The AGaaS Exit Framework

The Defensibility Map Series

In the last week, I’ve given you all the pieces you need to understand the new software ecosystem emerging.

At its core, it comes down to a simple truth:

The agent is becoming the computer.

We’re moving beyond the phase where AI merely helps humans perform tasks. We’re entering a new phase where agentic architectures are merging with the computer itself.

The computer is no longer just a tool operated by a human.

It is becoming an orchestrated system of agents capable of executing tasks autonomously, coordinating workflows, making decisions, and extending far beyond what traditional software could ever do.

In this new paradigm, the human role shifts fundamentally.

We are no longer operating the terminal directly. We are designing, guiding, and orchestrating the architectures that enable these agents to act on our behalf.

That is why this moment matters.

This is not just another software cycle. It is a new computational framework that will redefine what a computer is for the next 30–50 years.

That’s where AGaaS comes into play.

Yet, as the previous analyses showed, being “agent-native” does not make the game easier. In fact, it may make it harder.

This is becoming an extremely competitive market, and over the next 18–24 months, many AI-native startups will disappear.

Not only because they will fail outright, but because they will be merged, acqui-hired, or, as I’d put it, compute-scoped.

In other words, absorbed into the larger infrastructure and platform wars where access to compute, distribution, and orchestration capacity becomes more important than the product itself.

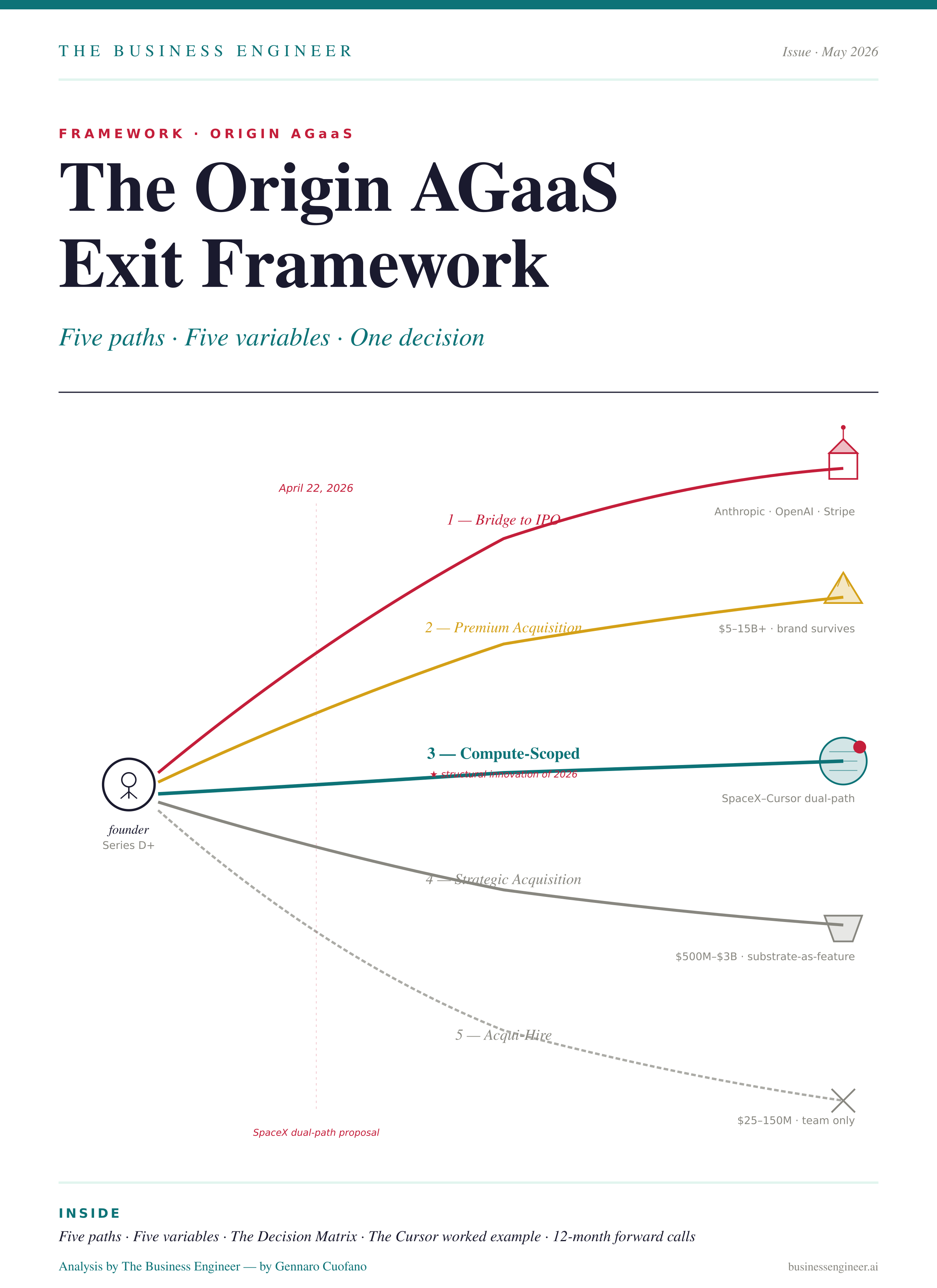

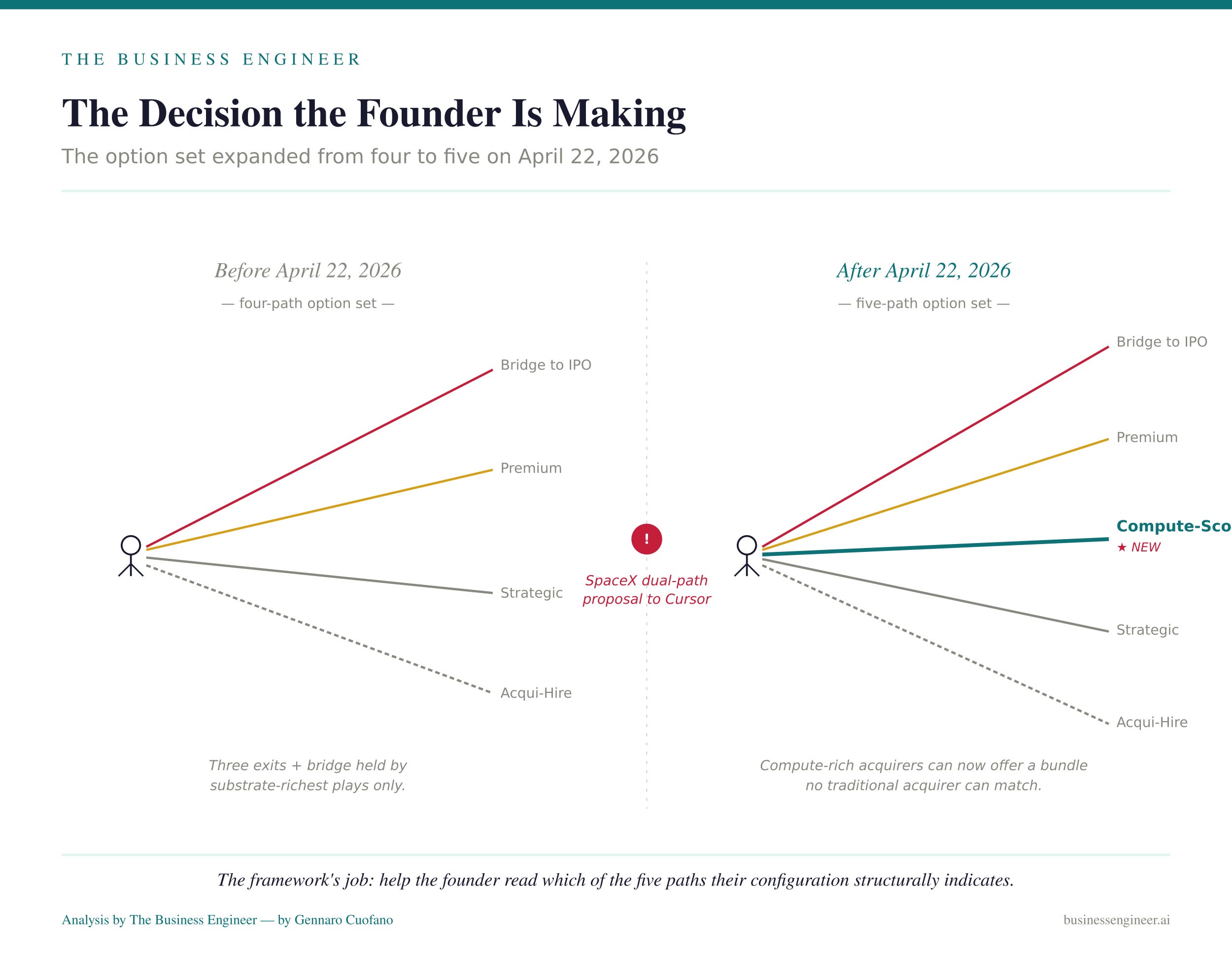

The AGaaS founder reaching Series D and beyond in 2026 faces a choice that the cohort’s first vintage did not face. For founders who reached this stage in 2023–2024, the option set was three: get acquired (acqui-hire, strategic, or premium price), stay independent and raise more venture, or shut down. For founders reaching it in 2026, the option set is five — and the fifth option is structurally new.

The April 22, 2026 SpaceX dual-path proposal to Anysphere (Cursor) is the moment that revealed the fifth option. SpaceX offered Cursor either a $60 billion outright acquisition or, alternatively, participation in a structured liquidity round that would let SpaceX participate in Cursor’s cap table without consolidating the asset.

Anysphere halted its in-progress $50 billion primary round to evaluate the proposal. The April 27, 2026 secondary market mark of $45.21 billion sits between the venture-priced and acquirer-priced reads — the cleanest available signal of how the market is currently pricing the choice.

What the SpaceX proposal made legible is that a compute-rich acquirer can offer a bundle no traditional acquirer and no venture round can match: compute commitment at scale, plus equity currency, plus structured liquidity — packaged either as full acquisition or as cap-table participation.

The bundle is not available from Andreessen Horowitz or Thrive Capital, because they cannot offer compute access. It is not available from Salesforce or Thomson Reuters, because they cannot bundle equity currency with compute. It is available only from acquirers whose primary asset is compute infrastructure at sovereign scale.

The five paths the framework names are:

Bridge to IPO — stay independent through structured tender offers; eventual IPO

Premium Acquisition — standalone-defensible exit with the brand surviving

Strategic Acquisition — substrate-as-feature, brand absorbed into a larger surface

Compute-Scoped Path — trade independence for sovereign-scale compute access plus structured liquidity

Acqui-Hire — team-only absorption, substrate doesn’t survive

What follows is the framework for choosing among them. The framework’s job is not to predict which path the market will produce. It is to help a founder facing the decision read which path their substrate position, compute trajectory, category geometry, brand position, and optionality preference structurally indicate.

In the end, this will give founders options.

The Portal collapses seven assets I have built separately over the past decade into one substrate.

The Five Paths — Definitions and Anchors

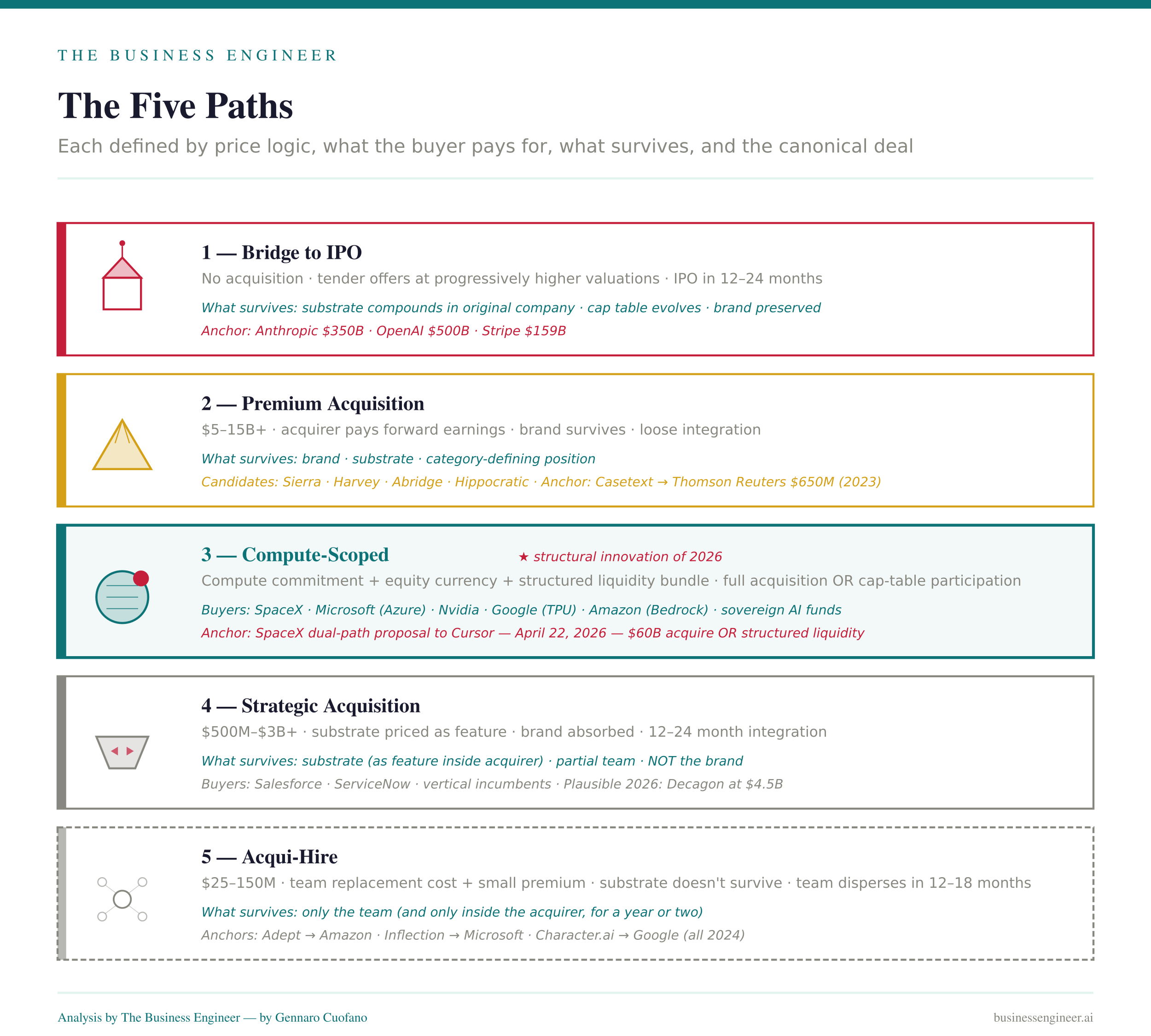

Each path is defined by four structural features: price logic, what the buyer is paying for, what survives the deal, and the canonical anchor deal that has now happened.

Path 1 — Bridge to IPO. No acquisition; periodic tender offers and primary rounds at progressively higher valuations; eventual IPO once public markets can correctly price AGaaS-native economics. The substrate stays compounding inside the original company; the cap table evolves; the brand is preserved; the IPO decision is deferred by 12–24 months. Buyers in the bridge are anchor allocators — sovereign wealth funds (GIC co-led Anthropic’s $10B Series G at $350B in February 2026), late-stage growth funds, crossover hedge funds. The anchor deals are Anthropic ($350B tender April 2026, IPO planned 2026), OpenAI ($500B secondary October 2025, listing steps underway), and Stripe ($159B tender February 2026). The bridge is not the SpaceX-style indefinite-private outcome; it is the SpaceX mechanism deployed as a bridge to public markets. Available only to substrate-richest plays in categories where the substrate compounding rate exceeds the rate at which any acquirer can price for it.

Path 2 — Premium Acquisition. Standalone-defensible exit at $5–15B+ with the original brand surviving. The acquirer pays forward earnings on a substrate-rich category leader; integration is intentionally loose; the original product line operates semi-autonomously. Buyers are hyperscalers (rarely, on category-defining substrate) and major incumbents (when the target completes their category strategy). Candidates in 2026 are Sierra ($15.8B post-money May 2026, $150M ARR, 40% of Fortune 50, structurally one funding event away from the bridge band), Harvey ($11B March 2026, 1300+ legal organizations across 60 countries, 25k+ custom agents running on the platform), Abridge (regulated clinical substrate), and Hippocratic (regulated healthcare substrate). The canonical historical anchor is the Casetext → Thomson Reuters deal at $650M in 2023, though the price bracket has shifted upward as the substrate has compounded.

Path 3 — Strategic Acquisition. Substrate-as-feature exit at $500M–$3B+, with the brand absorbed into the acquirer’s larger surface. The acquirer pays what the substrate would cost to build internally plus a premium minus the risk discount. The substrate survives; the brand does not; integration is twelve to twenty-four months; the team usually stays partially intact. Buyers are incumbents racing through their Mutating-zone migration — Salesforce, ServiceNow, Workday, Adobe, Atlassian, the major CX platforms, vertical incumbents (Thomson Reuters in legal, healthcare incumbents in clinical workflow, financial services incumbents in regulated voice). The canonical anchor is Casetext → Thomson Reuters ($650M, 2023); the 2025–2026 strategic-band deals follow the same pattern with vertical-specific variants. Decagon at $4.5B is a plausible 2026 target.

Path 4 — Compute-Scoped Path. The structural innovation of 2026. A compute-rich acquirer offers a bundle no traditional acquirer or venture round can match: sovereign-scale compute commitment, equity currency, and structured liquidity — packaged either as full acquisition or as cap-table participation. The seller trades some degree of independence for compute access they could not otherwise afford and could not buy at any venture-round price. Buyers are the small number of entities with sovereign-scale compute and balance-sheet capacity: SpaceX (revealed as a buyer through the Cursor proposal), Microsoft (via Azure commitments to OpenAI-shaped deals), Nvidia (via preferential compute access and equity), Google (via TPU commitments), Amazon (via Bedrock commitments), and sovereign AI funds (Saudi PIF, UAE MGX, possibly Norwegian and Singaporean equivalents through partnered structures). The canonical anchor is the April 22, 2026 SpaceX dual-path proposal to Cursor — $60B acquisition or structured liquidity participation. Whichever path Cursor takes will define the structural memory of how the compute-scoped option resolves.

Path 5 — Acqui-Hire. Team-only absorption at $25–150M. The buyer pays team replacement cost plus a small premium to clear founders’ liquidation preferences. The substrate does not survive; the team disperses within twelve to eighteen months; the brand dissolves. Buyers are primarily foundation model providers internalizing wrapper capability (Anthropic, OpenAI, Google DeepMind) and hyperscalers absorbing capability into their platform layer (Amazon for Bedrock AgentCore, Microsoft for Copilot Studio). The canonical anchors are Adept → Amazon (mid-2024), Inflection → Microsoft (early 2024), and Character.ai → Google (mid-2024) — all license-plus-team structures rather than full acquisitions.

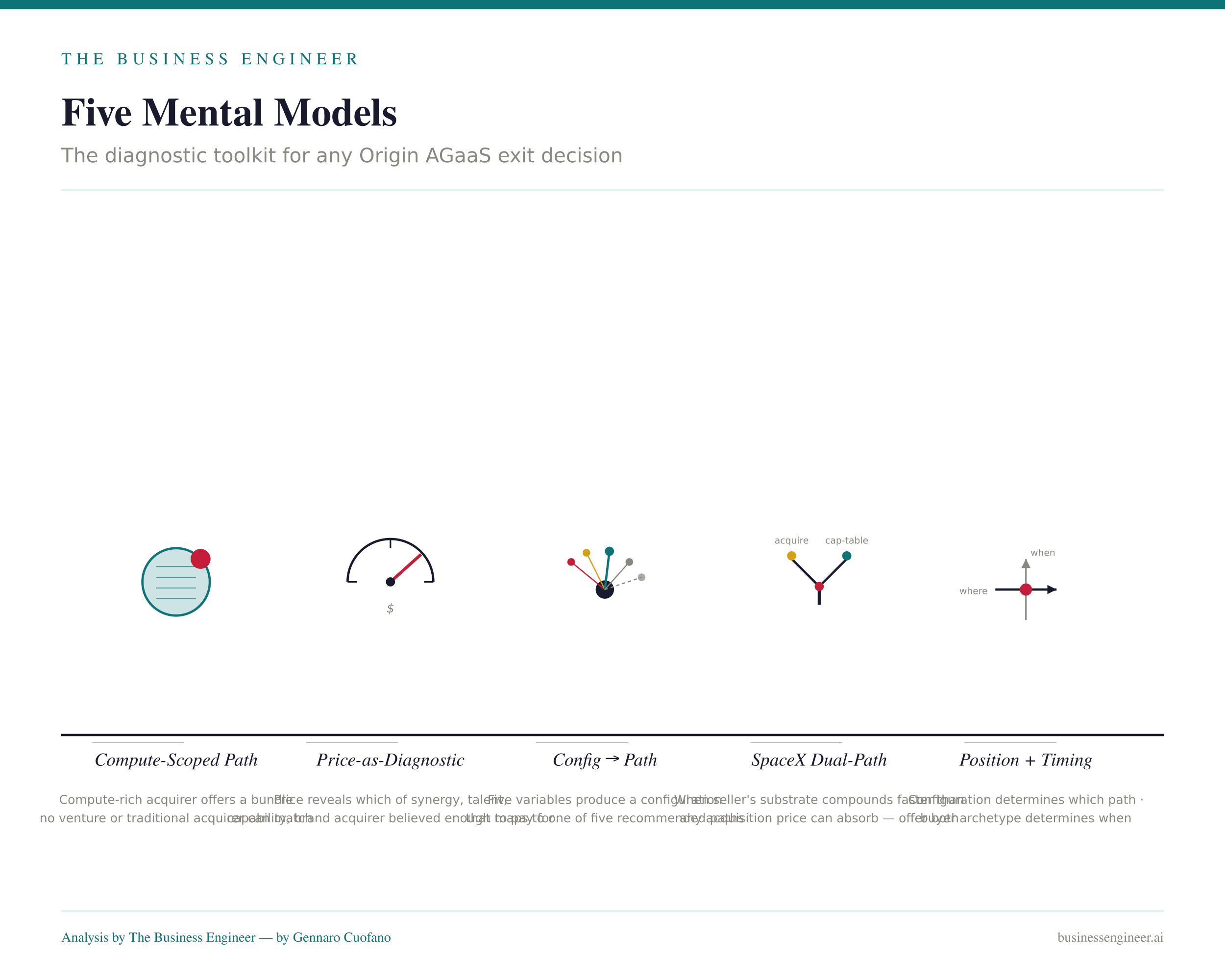

The Five Variables — How to Score the Decision

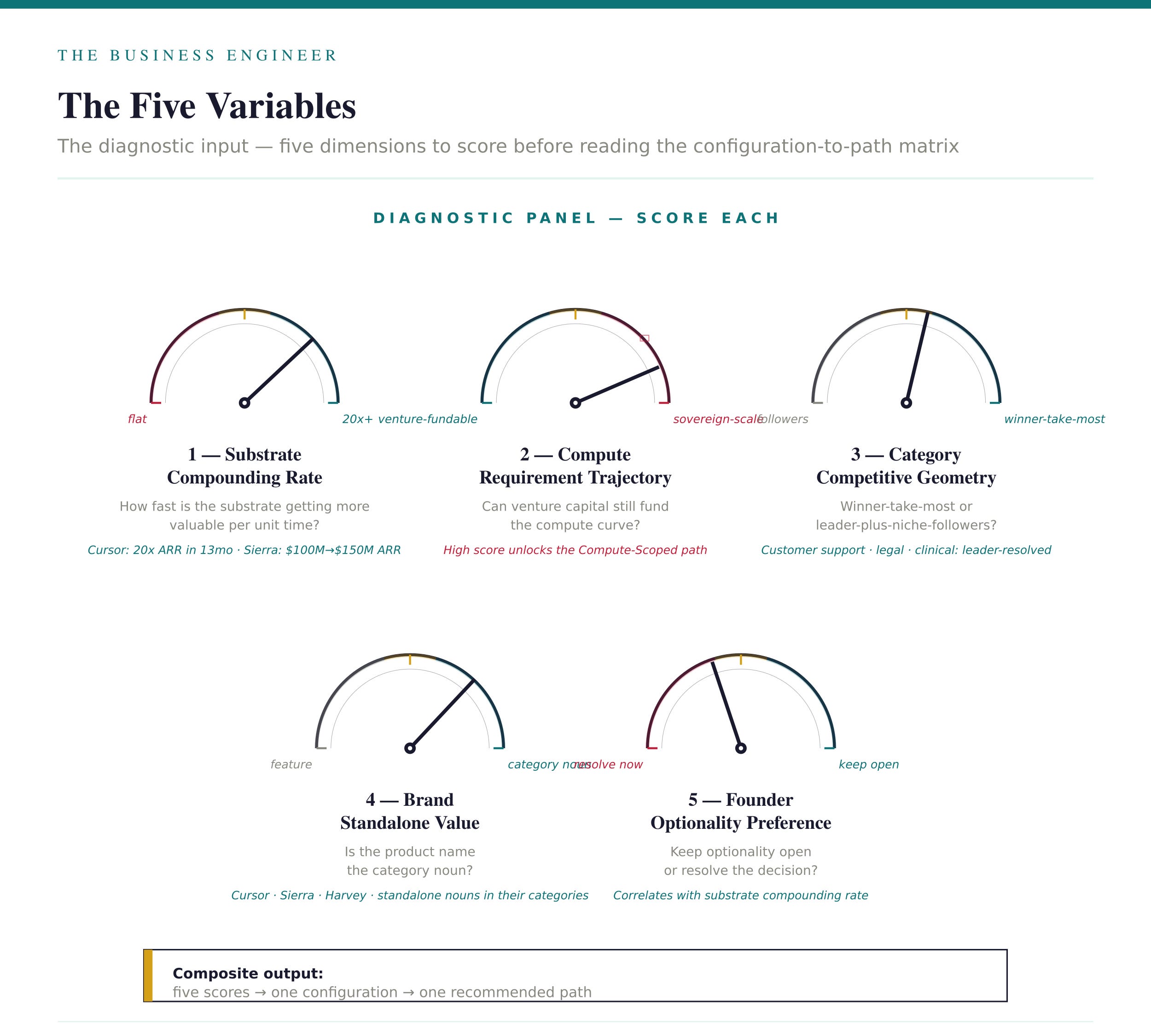

The framework’s diagnostic input is a score on five structural variables. The configuration of scores determines which path is structurally correct.

Variable 1 — Substrate Compounding Rate. How fast is the substrate getting more valuable per unit time? Cursor’s revenue went from $100M ARR in January 2025 to $2B ARR in February 2026 — a 20x ramp in thirteen months. Sierra went from $100M ARR in late 2025 to $150M+ in early 2026 with 40% of Fortune 50 deployment. Harvey reached 1300+ organizations and 25,000+ custom agents inside three years. The score is measurable: revenue compounding rate, customer-base compounding rate, substrate-asset compounding rate (outcome data accumulated, verification infrastructure deployed, embedded surface positions established). High scores favor the Bridge path. Mid scores favor Premium. Low scores favor Strategic. Near-zero scores indicate Acqui-Hire as the likely default.

Variable 2 — Compute Requirement Trajectory. How much compute will the company need to keep the substrate compounding, and can venture capital fund it? An Origin play whose substrate is compounding through proprietary model training (Cursor’s Composer, Sierra’s “constellation of models” approach running 15+ models in parallel) has a compute requirement curve that grows superlinearly with revenue. A play whose substrate is compounding through proprietary data accumulation without proprietary model training (Harvey’s legal substrate sitting on top of third-party foundation models, Abridge’s clinical substrate similarly) has a compute requirement that grows roughly linearly. The score is the ratio of compute requirement growth to venture-fundable capital growth. When the ratio is materially above 1.0 — when compute is growing faster than venture can fund — the Compute-Scoped path becomes structurally available and structurally attractive. Below 1.0, the Bridge path remains viable.

Variable 3 — Category Competitive Geometry. Is this a winner-take-most category or a category-leader-plus-niche-followers structure? Customer support agents have shown a category-leader pattern with Sierra emerging as the dominant Fortune 50 play; Decagon, Forethought, and others are settling into niche-follower positions. Legal AI shows the same pattern with Harvey dominant and vertical-specific plays in niche positions. Coding agents are still in winner-take-most contestation, with Cursor leading but Cognition, GitHub Copilot, Claude Code, and Cursor’s own Composer model all in real competition. Healthcare clinical documentation is showing winner-take-most dynamics with Abridge ahead. The score is structural: winner-take-most categories favor Bridge or Compute-Scoped (the category leader needs to keep compounding faster than competitors); category-leader-plus-niche-followers favors Premium for the leader and Strategic for the followers.

Variable 4 — Brand Standalone Value. Does the brand carry consumer-recognition value standalone, or does it carry value only as a feature inside a larger product? Cursor has standalone brand value among developers (it is the noun developers use, not a feature of someone else’s product). Sierra has standalone brand value among enterprise CX buyers. Harvey has standalone brand value among legal buyers. Most strategic-band targets do not have standalone brand value — they are valuable as substrate, but their brand is not a load-bearing asset. The score is observable: when the product name has become the category noun in the relevant buyer’s vocabulary, brand standalone value is high. When the product is described as “the agent layer for X” rather than by its own name, brand standalone value is low. High scores favor Bridge or Premium. Low scores favor Strategic or Acqui-Hire.

Variable 5 — Founder Optionality Preference. Does the founder want to keep optionality open or resolve the decision? Bridge maximizes optionality (the founder retains the IPO decision); Premium resolves the decision but preserves operational autonomy; Strategic resolves the decision and surrenders autonomy; Compute-Scoped is a hybrid (partial decision resolution, partial optionality preservation); Acqui-Hire resolves the decision completely. The score is the founder’s own — but it is structurally correlated with the company’s substrate compounding rate. Founders whose substrate is compounding fastest typically want to keep optionality open; founders whose substrate has plateaued typically want resolution.

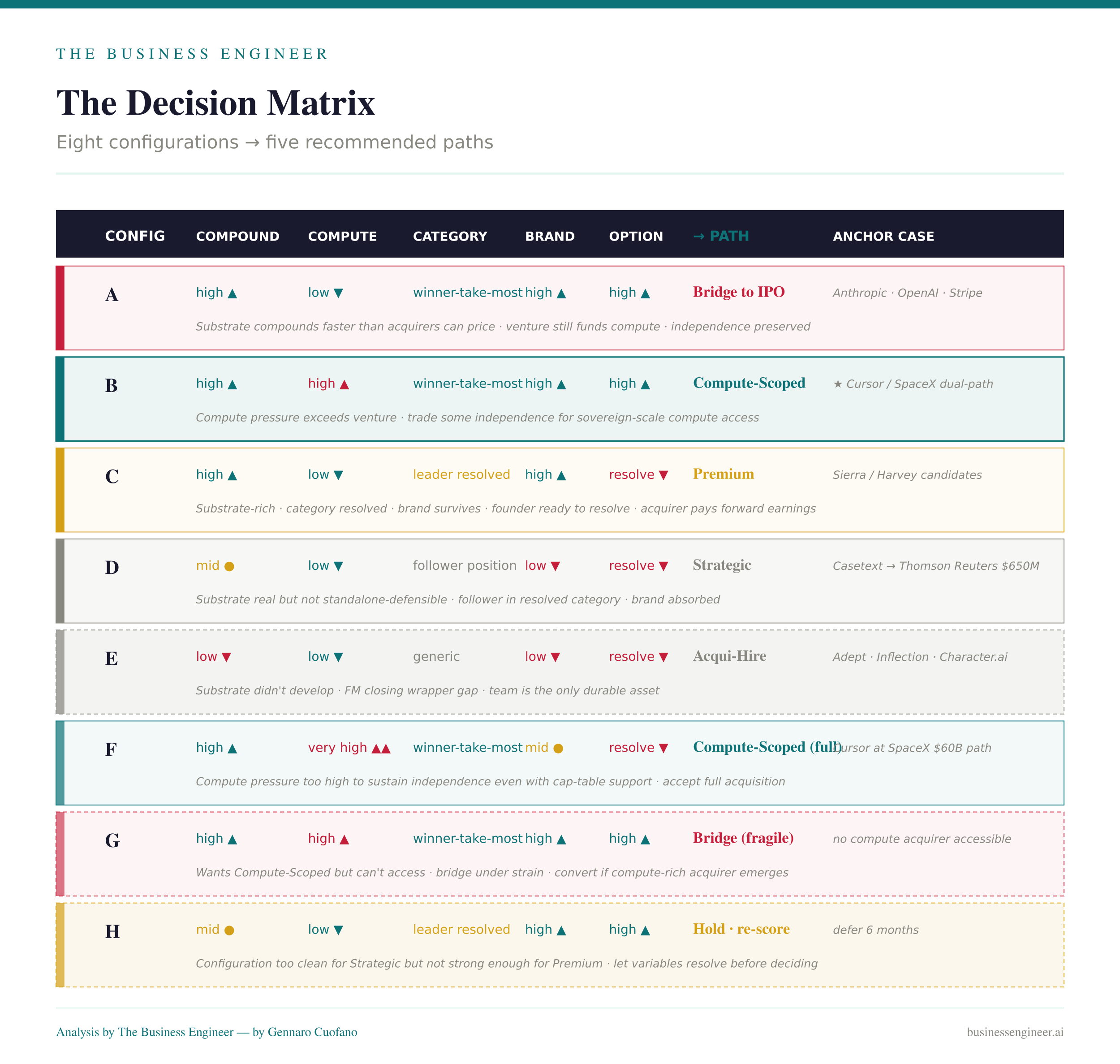

The Decision Matrix — Configuration to Path

The five variables produce a configuration. The configuration maps to a recommended path. The matrix below states the mapping for the eight most common configurations Origin AGaaS founders actually face in May 2026.

Configuration A — High compounding, low compute pressure, winner-take-most, high brand, high optionality. Recommended path: Bridge to IPO. Substrate is compounding faster than acquirers can price; compute is fundable through venture; the category dynamics reward staying in the race; the brand is a standalone asset; the founder wants to preserve the IPO option. Anchor case: Anthropic, OpenAI, Stripe. Counter-indication: if compute pressure rises sharply mid-bridge, the path may need to convert to Compute-Scoped.

Configuration B — High compounding, high compute pressure, winner-take-most, high brand, high optionality. Recommended path: Compute-Scoped. The substrate justifies independence, but the compute requirement curve has exceeded what venture can fund. Trading some independence for sovereign-scale compute is structurally correct because the alternative is losing the compounding race to a compute-better-funded competitor. Anchor case: Cursor’s decision in response to SpaceX. Counter-indication: if compute pressure normalizes (e.g., via efficiency gains in foundation models or via proprietary model wins like Cursor’s Composer), the path may revert to Bridge.

Configuration C — High compounding, low compute pressure, category-leader-plus-followers, high brand, low optionality. Recommended path: Premium Acquisition. Substrate is compounding, but the category has resolved enough that the leader’s price has stabilized; the founder is ready to resolve the decision; the brand value supports premium pricing. Anchor case: candidates are Sierra (if it chooses acquisition over bridge), Harvey (if Thomson Reuters or another major incumbent can reach the price). Counter-indication: if compute pressure rises, Compute-Scoped may become more attractive than Premium.

Configuration D — Mid compounding, low compute pressure, category-follower position, low brand, low optionality. Recommended path: Strategic Acquisition. Substrate is real but not standalone-defensible; the company is in a follower position in a resolved category; the brand will not survive standalone; the founder wants to resolve. Anchor case: most 2025–2026 strategic-band deals. Counter-indication: if substrate compounding accelerates, the path may upgrade to Premium.

Configuration E — Low compounding, low compute pressure, generic category, low brand, low optionality. Recommended path: Acqui-Hire. Substrate did not develop; foundation model capability is closing the wrapper gap; the team is the only durable asset. Anchor case: the long tail of 2024–2025 wrapper plays absorbed by FM providers and hyperscalers. Counter-indication: none — this is the default Casualty quadrant outcome.

Configuration F — High compounding, very high compute pressure, winner-take-most, mid brand, low optionality. Recommended path: Compute-Scoped via full acquisition. Compute pressure has reached a point where independence is structurally unsustainable; the seller accepts full acquisition by a compute-rich acquirer because the alternative is losing the race. This is the configuration where SpaceX’s $60B path wins over the structured-liquidity path. Anchor case: the path Cursor will choose if it accepts SpaceX’s acquisition rather than cap-table participation.

Configuration G — High compounding, high compute pressure, winner-take-most, high brand, high optionality, but no compute-rich acquirer interested. Recommended path: Bridge to IPO under compute strain. The founder wants the bridge, but cannot access the Compute-Scoped option because no compute-rich acquirer is offering. The bridge becomes harder to sustain; tender pricing may stall; the IPO timing may compress. This is a fragile configuration. Counter-indication: if a compute-rich acquirer enters, path converts to Compute-Scoped.

Configuration H — Mid compounding, low compute pressure, category-leader position, high brand, high optionality. Recommended path: Hold and re-score in six months. The configuration is too clean for Strategic but not strong enough for Premium or Bridge. The founder should defer the decision and let the compounding rate, compute trajectory, or category geometry resolve into a clearer configuration. Acting on this configuration prematurely is the most common error in the 2025–2026 cohort.

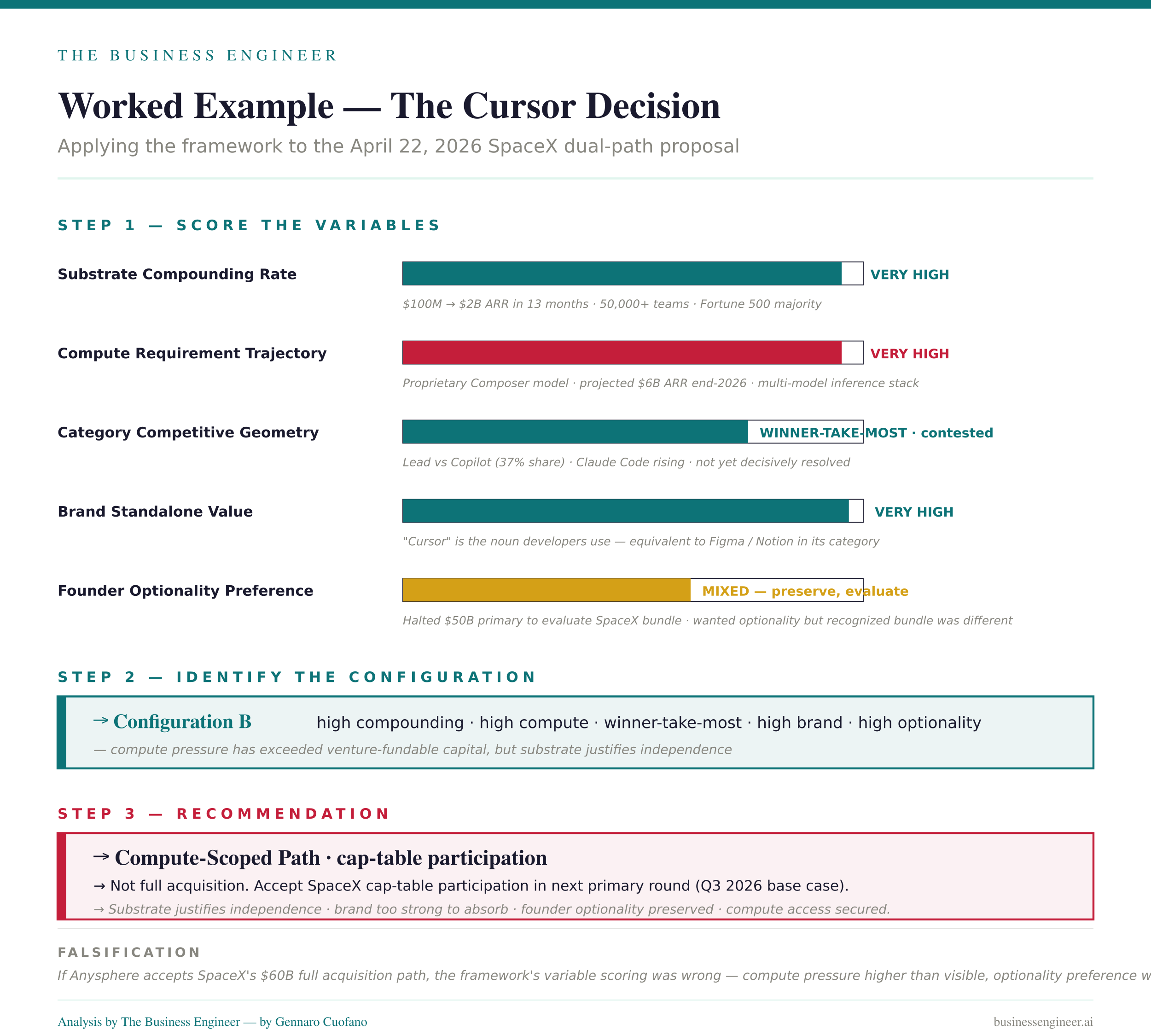

Worked Example — The Cursor Decision

The clearest application of the framework right now is the Cursor decision in response to SpaceX’s April 22, 2026 dual-path proposal.

Variable scores (May 2026):

Substrate Compounding Rate: very high — 20x revenue growth in 13 months ($100M → $2B ARR), 50,000+ teams, majority of Fortune 500, positive gross margins on enterprise sales

Compute Requirement Trajectory: very high — proprietary Composer model launched November 2025, projected $6B ARR by end-2026 implies further model investment, supplementary inference stack across Composer/Claude/GPT/Kimi

Category Competitive Geometry: winner-take-most, contested — GitHub Copilot at 37% market share with 4.7M paid subscribers and 90% Fortune 100 adoption, Claude Code rising to 57% developer awareness, Cursor in lead but not yet decisive

Brand Standalone Value: very high — Cursor is the noun developers use for AI-native coding environment, equivalent to “Figma” or “Notion” status in its category

Founder Optionality Preference: mixed — founders halted the $50B primary round to evaluate SpaceX, suggesting they wanted to preserve optionality but recognized the SpaceX bundle was structurally different from the venture round

Framework reading: the configuration matches Configuration B (high compounding, high compute pressure, winner-take-most, high brand, high optionality). The recommended path is Compute-Scoped via cap-table participation rather than full acquisition. The structural reasoning: substrate justifies independence; compute pressure has exceeded what venture can fund (which is why the $50B primary was halted); the category has not yet resolved so independence remains structurally valuable; the brand is too strong to absorb into SpaceX or any other acquirer’s product line; the founder optionality preference is preserved by cap-table participation rather than full acquisition.

Falsification: if Anysphere accepts SpaceX’s $60B full acquisition path, the framework’s recommendation was wrong. The structural reading would then be either (a) compute pressure was higher than visible from outside, (b) the founder optionality preference was weaker than indicated, or (c) the category competitive geometry was more resolved than the framework scored.

Forward expectation: the base case as of May 2026 is that Anysphere takes the structured liquidity path, with SpaceX participating in a next primary round (probably Q3 2026) at a valuation between $60B and $100B. This would validate the framework’s recommendation and establish the Compute-Scoped path as a stable fifth option in the Origin AGaaS exit market.

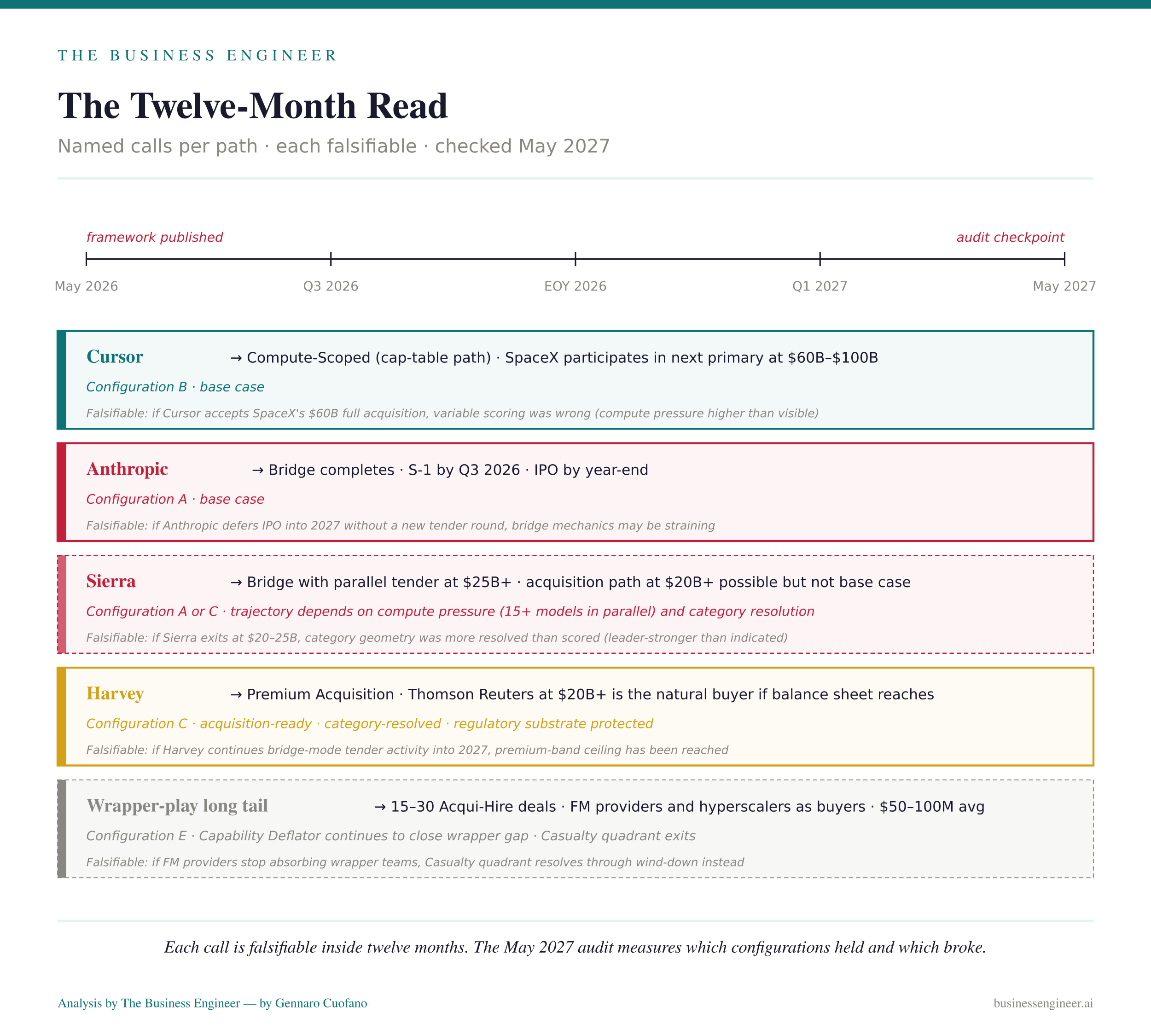

The Twelve-Month Read — Which Plays Will Choose Which Path

Three specific named calls based on the framework, with the structural reasoning compressed:

Cursor → Compute-Scoped (cap-table path). Configuration B; SpaceX bundle is structurally superior to either pure acquisition or pure venture round. Falsifiable: if Cursor accepts SpaceX’s $60B full acquisition, framework’s variable scoring was wrong.

Anthropic → Bridge completes; IPO by year-end 2026. Configuration A; substrate compounding rate justifies bridge continuation but planned 2026 IPO suggests bridge is near termination. S-1 filing by Q3 2026 expected. Falsifiable: if Anthropic defers IPO into 2027 without a new tender round, bridge mechanics may be straining.

Sierra → Bridge with parallel tender at $25B+. Configuration A or C — depends on whether compute pressure is rising (Sierra runs 15+ models in parallel, which suggests rising compute) and whether category has resolved (40% of Fortune 50 suggests resolution toward Sierra). Base case is Bridge with tender at $25B+; acquisition path is possible if Salesforce or a hyperscaler reaches $20B+ in the next twelve months. Falsifiable: if Sierra accepts acquisition at $20–25B, framework’s category geometry scoring was wrong (Sierra was more leader-resolved than indicated).

Harvey → Premium Acquisition by Thomson Reuters at $20B+. Configuration C; substrate is acquisition-ready, category has resolved with Harvey dominant, brand value is high but is partially absorbed by acquirer’s existing brand strength in legal. Thomson Reuters is the natural buyer but balance sheet may not reach. Falsifiable: if Harvey continues bridge-mode tender activity into 2027, framework’s compounding rate was scored too high (Harvey has reached premium-band ceiling).

The wrapper-play long tail → Acqui-Hire. Configuration E; foundation model capability continues to close wrapper gap; 15–30 acqui-hire deals expected over the next twelve months. Falsifiable: if FM providers stop absorbing wrapper teams (because foundation model capability has internalized the wrapper layer entirely), framework’s acqui-hire band predictions break and Casualty quadrant resolves through wind-down rather than acqui-hire.

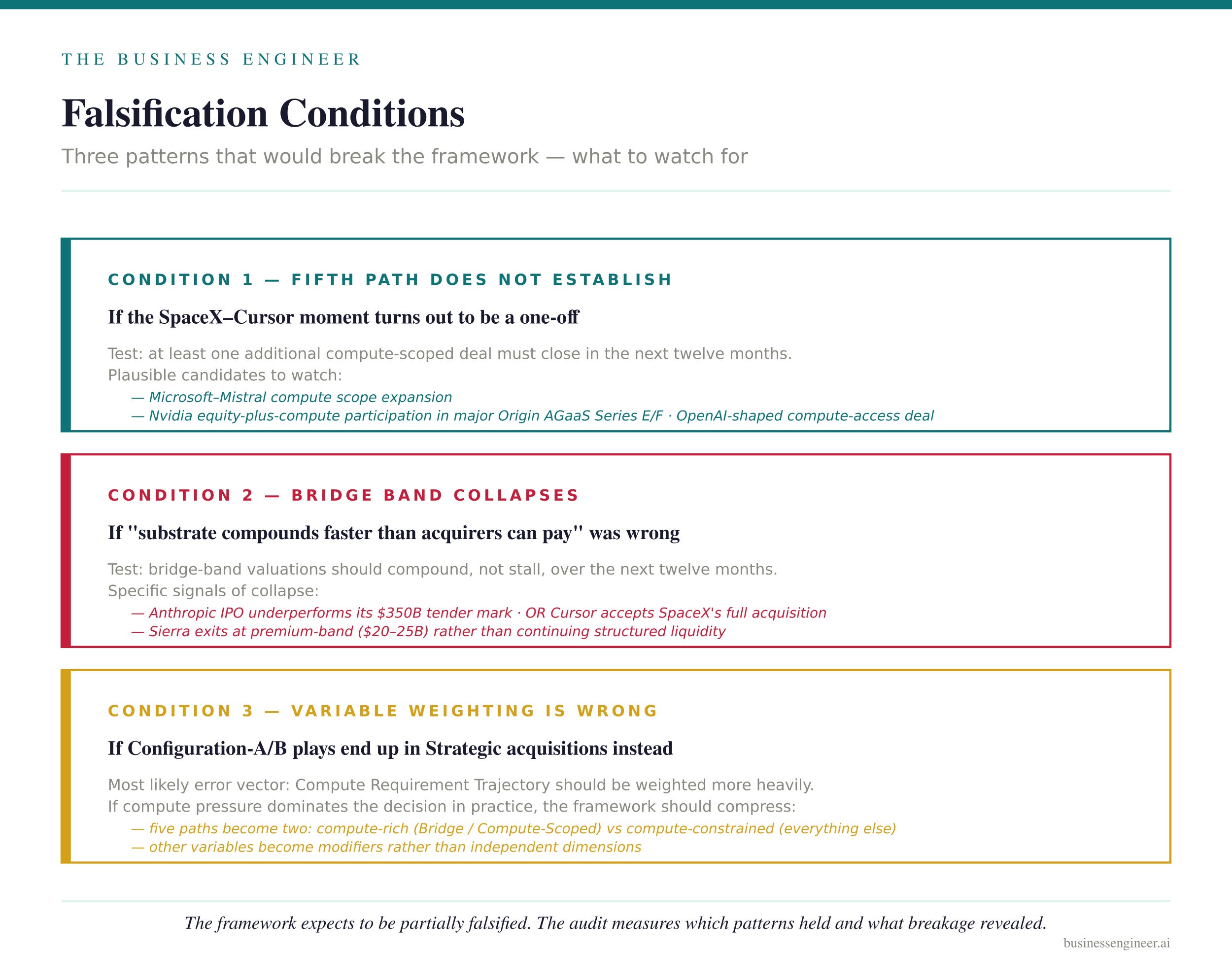

Falsification Conditions

The framework is falsifiable. Three patterns that would break it:

If the Compute-Scoped path does not establish as a stable fifth option — meaning the SpaceX-Cursor moment turns out to be a one-off rather than the named instance of a recurring pattern — the framework’s central claim is wrong. The test: at least one additional compute-scoped deal must close in the next twelve months. Plausible candidates: Microsoft–Mistral compute scope expansion, Nvidia equity-plus-compute participation in a major Origin AGaaS Series E or F, an OpenAI-shaped deal where compute access is the primary asset traded.

If the bridge band collapses — Anthropic IPO underperforms, Cursor accepts SpaceX’s full acquisition, Sierra exits at premium-band — the framework’s structural claim that “substrate compounds faster than acquirers can pay” was wrong. The test is empirical: bridge-band valuations should compound, not stall, over the next twelve months.

If multiple Configuration-A and Configuration-B plays end up in Strategic Acquisition (substrate-as-feature) outcomes instead of the recommended paths, the framework’s variable weighting is wrong. The most likely error vector is that Compute Requirement Trajectory should be weighted more heavily; if compute pressure dominates the decision in practice, the framework should compress the five paths into two: compute-rich (Bridge or Compute-Scoped) versus compute-constrained (everything else).

The framework expects to be partially falsified. The audit twelve months from now will measure which configurations held and which broke, and what the breakage revealed about the underlying structural physics of substrate, compute, and category.

Key Takeaways & Mental Models

The Compute-Scoped Path Is the Structural Innovation of 2026. Before April 22, 2026, Origin AGaaS founders faced four exit paths. After April 22, they face five. The fifth path exists because compute-rich acquirers can offer a bundle (sovereign-scale compute + equity currency + structured liquidity) that no traditional acquirer or venture round can match. Mechanism: when compute pressure exceeds venture-fundable capital, the founder trades some independence for compute access at scale.

The Price Is the Substrate Diagnostic. Each price band encodes a specific structural read by the buyer about what is durable in the target. Acqui-hire prices the team; strategic prices the substrate-as-feature; premium prices the standalone business; compute-scoped prices the compounding curve under compute access; bridge prices the compounding curve in independence. Mechanism: price encodes the buyer’s structural belief about what survives the deal close and what compounds after it.

The Five-Variable Configuration Maps to a Recommended Path. Substrate compounding rate, compute requirement trajectory, category competitive geometry, brand standalone value, and founder optionality preference together determine the structurally correct path. The framework’s diagnostic output is the configuration-to-path mapping, not a market prediction. Mechanism: structural variables produce structural fates; the founder’s choice is whether to align with the structural recommendation or actively diverge from it.

The SpaceX Dual-Path Moment. SpaceX’s April 22, 2026 proposal to Cursor — $60B acquisition or structured liquidity participation — is the framework moment that revealed the fifth option. SpaceX did not just offer to buy Cursor; SpaceX offered Cursor a structurally new exit architecture, made the architecture itself legible, and forced every other compute-rich entity to consider whether they should offer something similar. Mechanism: when the seller’s substrate compounds faster than any acquisition price can absorb, the acquirer’s best option is to bundle compute access with cap-table participation rather than consolidate the asset.

Configuration Determines Path, Buyer Determines Timing. The framework predicts which path each Origin AGaaS play should choose based on its variable configuration. The specific timing of the deal depends on which buyer archetype reaches first — and which compute-rich acquirer decides to use the SpaceX dual-path template in the next twelve months. Mechanism: structural position determines structural fate; market access and buyer initiative determine the specific outcome inside each fate.

Recap: In This Issue!

The AGaaS founder reaching Series D and beyond in 2026 now faces a new exit architecture.

The old menu was:

acquisition

stay independent

shut down

The new menu has a fifth path: compute-scoping.

This exists because compute-rich acquirers can offer something traditional investors cannot: capital plus compute plus liquidity.

The Agent Becomes the Computer

The deeper shift is not just that AI helps humans use software.

It is that agents are becoming the operating layer of the computer itself.

The computer is evolving from a human-operated tool into an orchestrated system of autonomous agents.

Humans move from operators to architects, supervisors, and orchestrators.

Why AGaaS Becomes Strategically Harder

Being agent-native does not make the market easier.

It makes the market more competitive.

Many AI-native startups will disappear over the next 18–24 months through:

acquisitions

acqui-hires

strategic absorption

compute-scoped deals

outright failure

The New Force: Compute-Scoping

Compute-scoping means trading some independence for access to sovereign-scale compute.

This is structurally different from a normal acquisition or venture round.

The buyer is not just offering capital.

It is offering:

compute capacity

equity currency

structured liquidity

platform leverage

The SpaceX-Cursor Moment

SpaceX’s dual-path proposal to Anysphere/Cursor made the fifth option visible.

The offer reportedly included:

a full acquisition path

or a structured liquidity path with SpaceX entering the cap table

This showed that compute-rich buyers can create hybrid deal structures traditional VCs cannot match.

Why Traditional Capital Cannot Match It

Venture funds can provide money, but not sovereign-scale compute.

Traditional acquirers can provide distribution, but not necessarily compute.

Compute-rich buyers can bundle:

infrastructure access

capital

liquidity

strategic protection

That bundle becomes decisive when the company’s growth depends on compute availability.

The Five Founder Paths

Bridge to IPO

stay independent through tenders and late-stage rounds

preserve the brand and compounding substrate

Premium Acquisition

sell at a high price while preserving product identity

best for category leaders with durable substrate

Strategic Acquisition

become a feature inside a larger platform

substrate survives, brand usually does not

Compute-Scoped Path

trade some independence for compute access and structured liquidity

new path for compute-intensive AGaaS winners

Acqui-Hire

team-only absorption

substrate does not survive

Price Reveals Structural Value

Each exit band prices a different asset:

acqui-hire prices the team

strategic acquisition prices substrate-as-feature

premium acquisition prices the standalone business

compute-scoped deal prices the growth curve plus compute dependency

bridge to IPO prices independent compounding

The Five Decision Variables

Founders should score the company across five variables:

Substrate compounding rate

how fast the company becomes more valuable with each deployment

Compute requirement trajectory

whether compute needs are outgrowing venture-fundable capital

Category competitive geometry

whether the market is winner-take-most or leader-plus-followers

Brand standalone value

whether the product name has become the category noun

Founder optionality preference

whether the founder wants independence, resolution, or a hybrid

When Bridge to IPO Makes Sense

Best fit when:

substrate is compounding quickly

compute pressure is manageable

brand is strong

the category remains large enough for independence

founders want to preserve optionality

When Premium Acquisition Makes Sense

Best fit when:

the company is a category leader

substrate is durable

brand has standalone value

the founder is ready to resolve

the acquirer can pay for the full strategic value

When Strategic Acquisition Makes Sense

Best fit when:

substrate is real but not independently dominant

the company is a category follower

brand value is limited

the acquirer can absorb the product into a larger platform

When Compute-Scoped Makes Sense

Best fit when:

substrate is compounding fast

compute needs are rising faster than venture can fund

the category is winner-take-most

brand value remains strong

independence is still valuable but compute access is becoming existential

When Acqui-Hire Becomes the Default

Best fit when:

substrate did not develop

the company is mostly a wrapper

foundation models are closing the capability gap

the team is more valuable than the product

Cursor as the Framework Case

Cursor fits the compute-scoped profile because it combines:

rapid revenue growth

strong standalone brand

contested winner-take-most category dynamics

rising proprietary model and inference needs

strategic need for compute access

The strongest path is not necessarily full acquisition.

It may be structured liquidity plus compute access.

The Exit Market Is Bifurcating

Weak wrapper plays move toward acqui-hire or shutdown.

Mid-tier substrate plays move toward strategic acquisition.

Durable category leaders move toward premium acquisition or IPO bridge.

Compute-intensive leaders may move into compute-scoped structures.

The Next 12 Months Are Diagnostic

The key test is whether compute-scoped deals become a recurring pattern.

If more compute-rich buyers copy the SpaceX template, compute-scoping becomes a stable fifth path.

If not, the Cursor proposal remains an exceptional case.

Final Compression

AGaaS founders are no longer choosing only between independence and acquisition.

They are choosing among different ways to price substrate, compute dependence, brand value, and optionality.

The new question is not simply:

Should we sell or stay independent?

It is:

Can we keep compounding without sovereign-scale compute access?

With massive ♥️ Gennaro Cuofano, The Business Engineer