Beyond the NVIDIA's Tax

The Map of AI Series

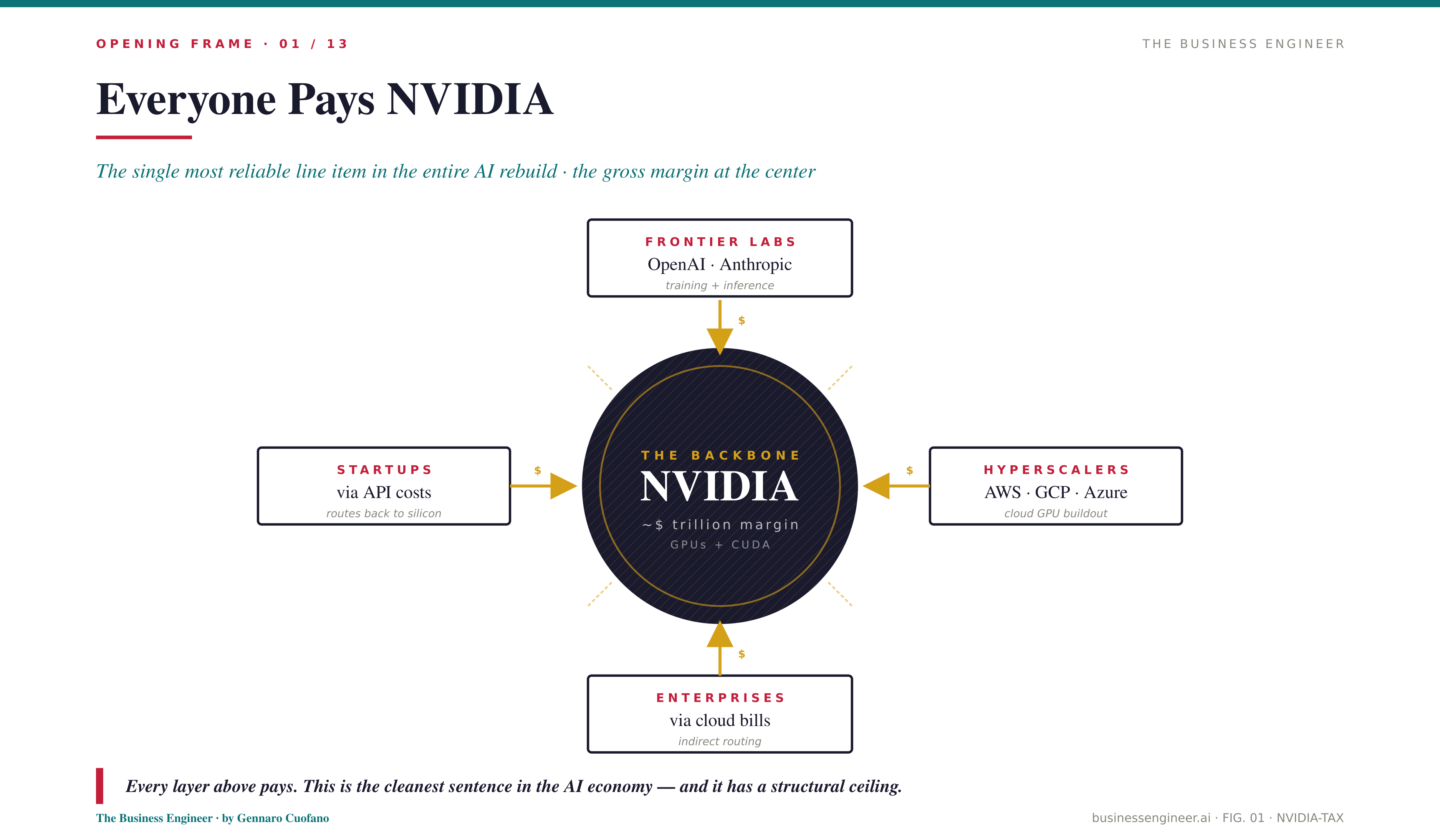

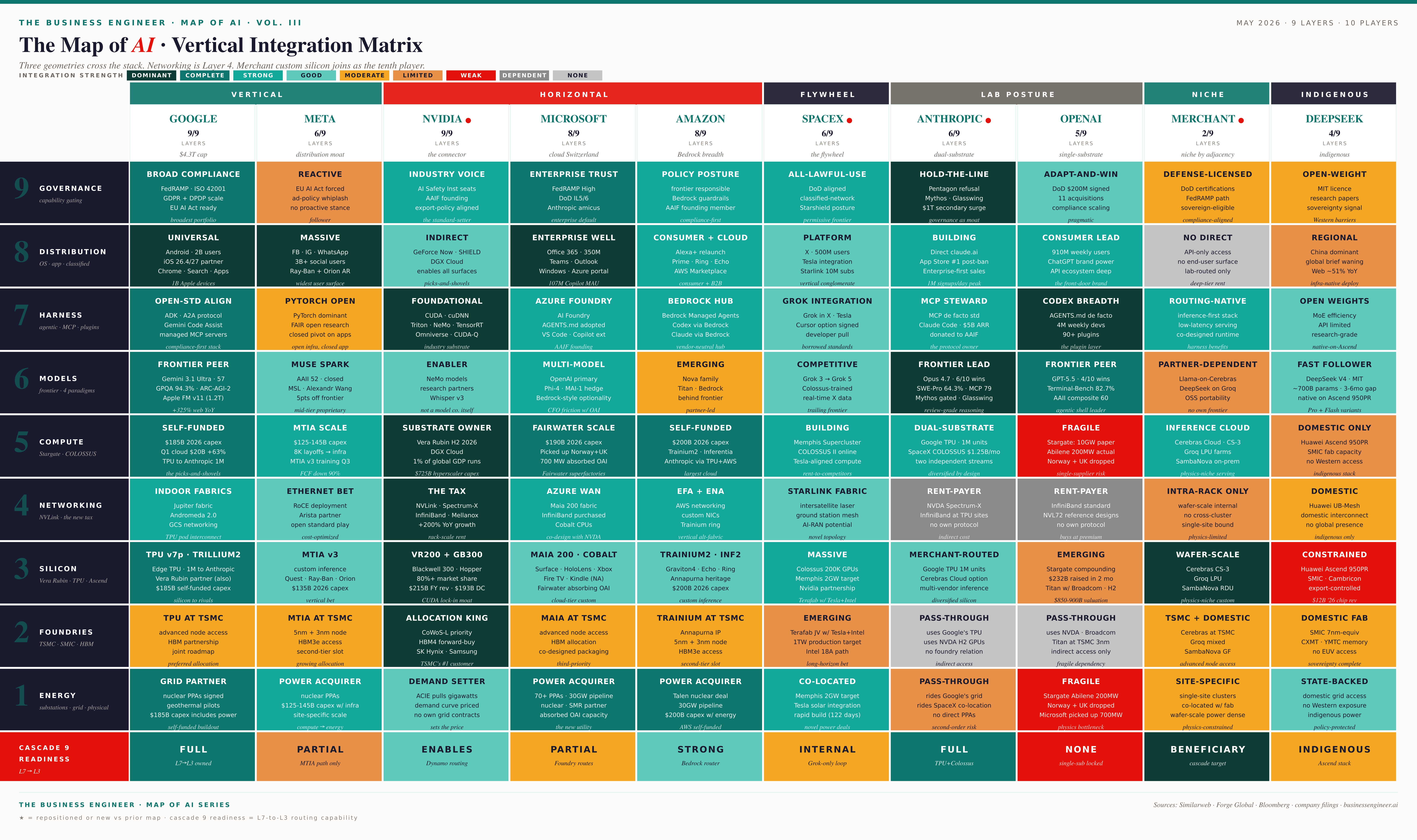

For three years, the cleanest sentence in the AI economy has been: everyone pays NVIDIA. Frontier Labs pays it. Hyperscalers pay it. Enterprises pay it through their cloud bills. Startups pay it through API costs that ultimately route to it. The single most reliable line item in the entire rebuild is the NVIDIA gross margin.

That is now changing. Not collapsing — changing.

Underneath the headline number that says NVIDIA’s revenue keeps climbing, the silicon layer of the stack is fracturing in three directions at once: hyperscalers are building their own chips for their own workloads, a generation of specialty silicon startups is attacking the parts of the workload the GPU was never optimal for, and a much smaller number of foundry and packaging providers are quietly emerging as the binding constraint that bounds all of it.

The most monopolistic layer of the AI stack is becoming the most differentiated.

This piece maps that fracture. Four layers as before: the abstraction (why the monopoly was structurally finite), the market map (who is building what), the playbook (three observable shifts in how silicon strategy is converging), and what comes next (where the leverage moves once the GPU’s generalism stops being the winning hand).

For Premium Members: