The AI Capex Map & The State of AI Hyperscalers

The May 2026 Edition

In the last week of April 2026, Microsoft, Amazon, Alphabet, and Meta reported their first-quarter results within forty-eight hours of one another.

The Big Four lifted their 2026 capex guides in unison. Apple reported the day after, decreasing capex year-over-year — and announcing a structural break from its decade-old “net cash neutral” policy.

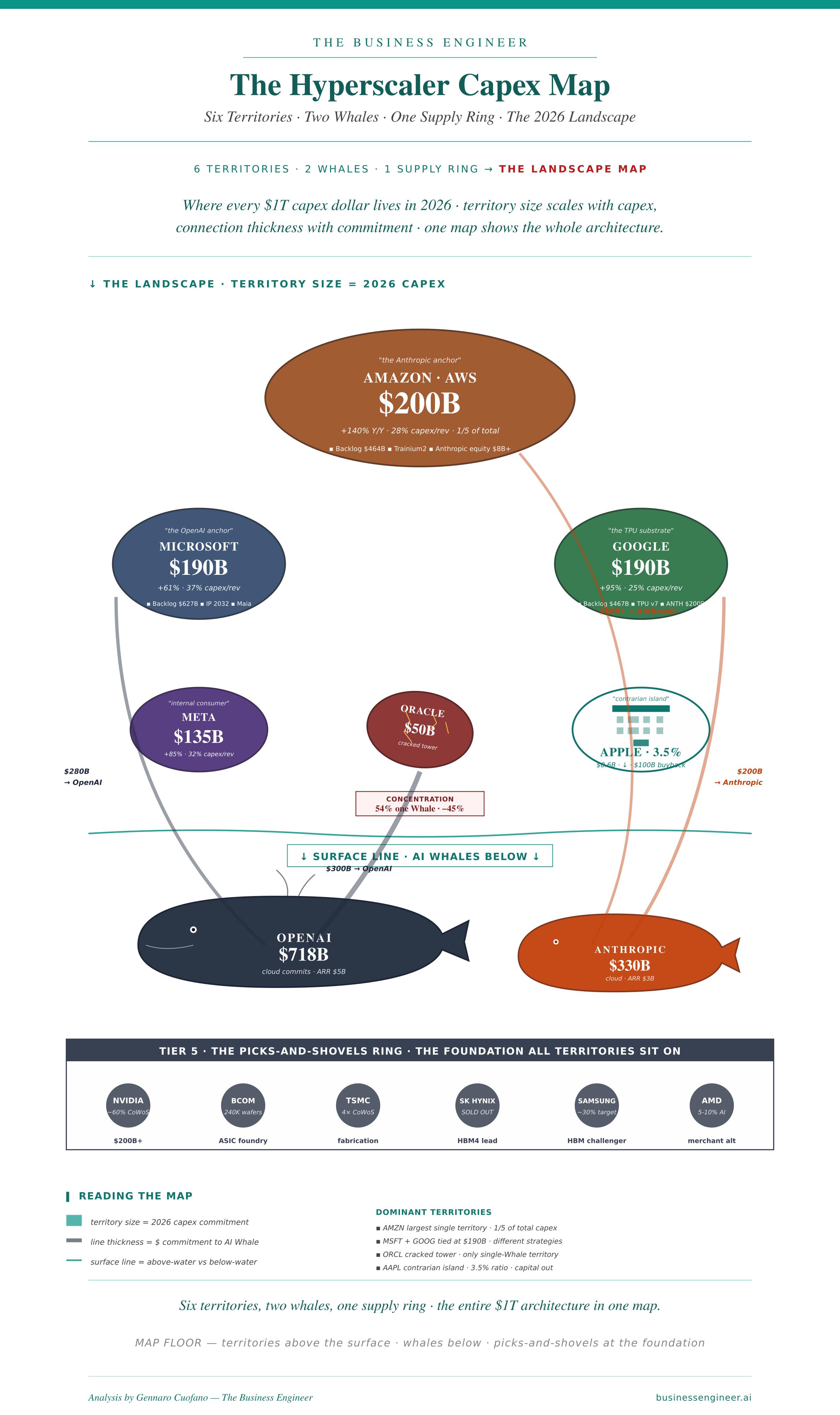

The Financial Times then compiled the totals: $725 billion combined for the Big Four in 2026, up 77% from $410B in 2025 — the largest single-year concentrated infrastructure cycle in the history of technology.

Q1 alone saw the Big Four spend $130 billion combined — 3.7× the $35 billion they spent in Q1 2023.

A week later, on May 5, 2026, The Information disclosed the dollar figure on Anthropic’s Google Cloud commitment: $200 billion over five years for 5 GW of capacity.

Taken together with prior disclosures, the picture was clarified: the four largest U.S. cloud providers now hold roughly $2.1 trillion in revenue backlog, and half of that — $1.05 trillion — comes from two cash-burning AI startups,

OpenAI and Anthropic. The $1T capex cycle is being underwritten by a $1T concentrated demand commitment from two counterparties whose combined free cash flow is deeply negative.

The total cycle: $725B Big Four + $50B Oracle + $13B Apple + $60B Neoclouds + $80B China + $60B Sovereigns + $48B Other = ~$1.04 trillion in 2026 compute capex, the first trillion-dollar year of compute capex in human history. We’ll do the bottom-up math in Section 10.

This is not a continuation of the cloud capex cycle. This is a different cycle, with different physics.

The May 2026 Map of AI argued that the seven-layer AI stack is now governed from the bottom — energy, silicon, compute capacity. That is the architecture.

The Map of AI

Seven weeks since the March 13 map. The five-race frame held. What changed is the velocity inside the frame — and in the last fourteen days, the velocity broke into a new register.

This piece is about the financing. How the money flows, where it cracks, what it buys, who can absorb it, and what happens when revenue can’t catch up.

Five cascades, fifteen players, ten structural truths — plus two structural shifts that landed in the final week of April that change the read on the whole cycle, plus the bottom-up landing-zone math for 2026, plus the AI Whales concentration that explains why this is fragile in a way the headline numbers obscure.

The thesis: the capex race is no longer a corporate spending cycle. It is a sovereign-scale financing problem dressed in tech-company clothing — and the financial architecture is starting to invert.

You can also find the interactive map below.

For Exec Members, The Full BE Agent Harness Is Now Available!

The Portal collapses seven assets I have built separately over the past decade into one substrate.