The AI Memory Tax & the Bifurcation of AI Scaling Laws

The AI Map Series

For most of semiconductor history, memory was the unglamorous sibling of compute. Intel and later NVIDIA carried the branded, premium, era-defining narratives.

Memory was made in Korea and Japan, sold as a commodity, and lived through the most brutal cycles in tech — peak-to-trough revenue swings routinely above 50%, suppliers wiped out every decade, the survivors learning to bleed quietly through downturns and harvest aggressively through ups.

The industry consolidated from dozens of players in the 1990s to three by the 2010s, and even those three traded at low multiples because the market priced them as cyclical commodity producers rather than strategic assets.

Two things broke that frame.

The first was an obscure academic prediction. In 1995, computer architects Wulf and McKee published a paper titled “Hitting the Memory Wall,” arguing that processor speed was improving exponentially while memory access latency was barely moving, and eventually applications would stall waiting for data rather than computation. For thirty years the prediction was directionally right but commercially manageable — software architects partitioned around the wall, caches got bigger, problems got reshaped.

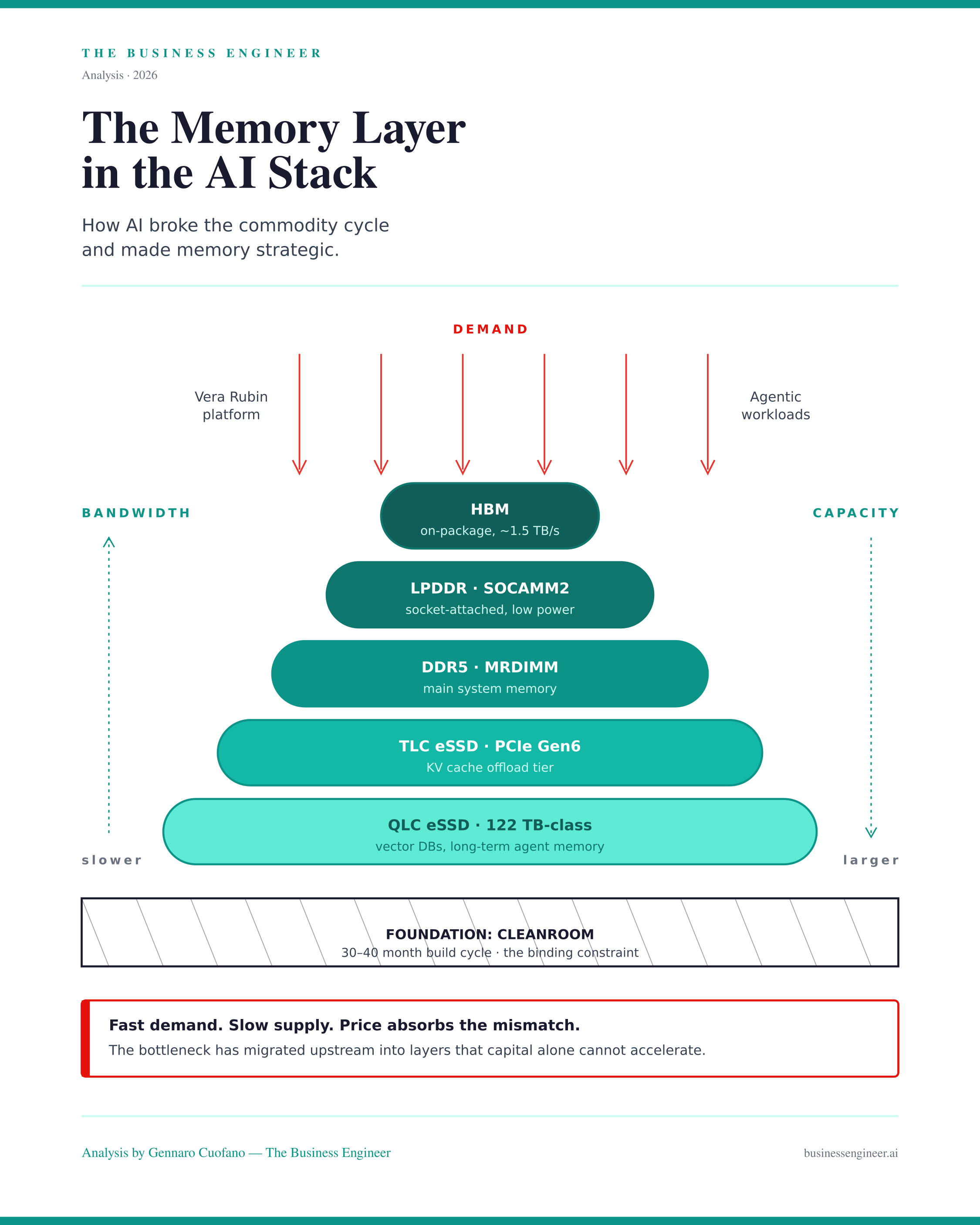

The second was an accident. In the early 2010s, AMD and SK hynix co-developed High Bandwidth Memory (HBM) for graphics cards — stacks of memory chips bonded directly onto the GPU package to feed pixel-pushing workloads. NVIDIA adopted it for high-performance computing. Then transformer attention mechanisms turned out to be one of the most memory-bandwidth-hungry computations ever deployed at scale, and HBM — designed to render video games — became the single most strategically important silicon product in the world.

The result is what we are seeing now: memory has stopped being a commodity, the cycle has stopped behaving like a cycle, and the three suppliers that survived the consolidation are printing record margins while still telling customers they cannot deliver enough product. This is not a peak. It is a regime change. What follows is why, what the actual products are, who owns what, and how the whole thing cascades back through the AI infrastructure map.

This is part of the Map of AI Series

Interactive Map Available Here!

For Exec Members, The Full BE Agent Harness Is Now Available!

The Portal collapses seven assets I have built separately over the past decade into one substrate.