The AI Supercycle

The Business Engineer's Toolbox

Back in 2022, I introduced my first analogy for what I believed would become the defining shape of the AI revolution.

As an analyst, a student of history, and someone deeply interested in structural realities, I see it as my responsibility to make a deliberate effort to contextualize, abstract, compress, and build mental models that help explain the world around us.

That is what The Business Engineer is about. For me, it is a lifelong quest.

So when ChatGPT was released, I felt it was essential to provide a framework, a mental model capable of making sense of the emerging AI era.

At the time, despite the relentless pace of progress in AI, it is easy to forget how many people believed everything would change within a single year. The expectations were immense. In that environment, I felt a better frame was needed.

That is where the AI Supercycle Thesis emerged.

And a word of caution: the term supercycle should not be interpreted as a purely economic concept. It goes far beyond economics. It describes the intersection of three powerful forces: geopolitics, cultural transformation, and economic change.

The economy is only one layer of the story. In many ways, it is the instrument through which deeper geopolitical and cultural shifts express themselves.

The AI Supercycle is ultimately an attempt to understand the thread connecting these forces and how, together, they shape the next era of human development.

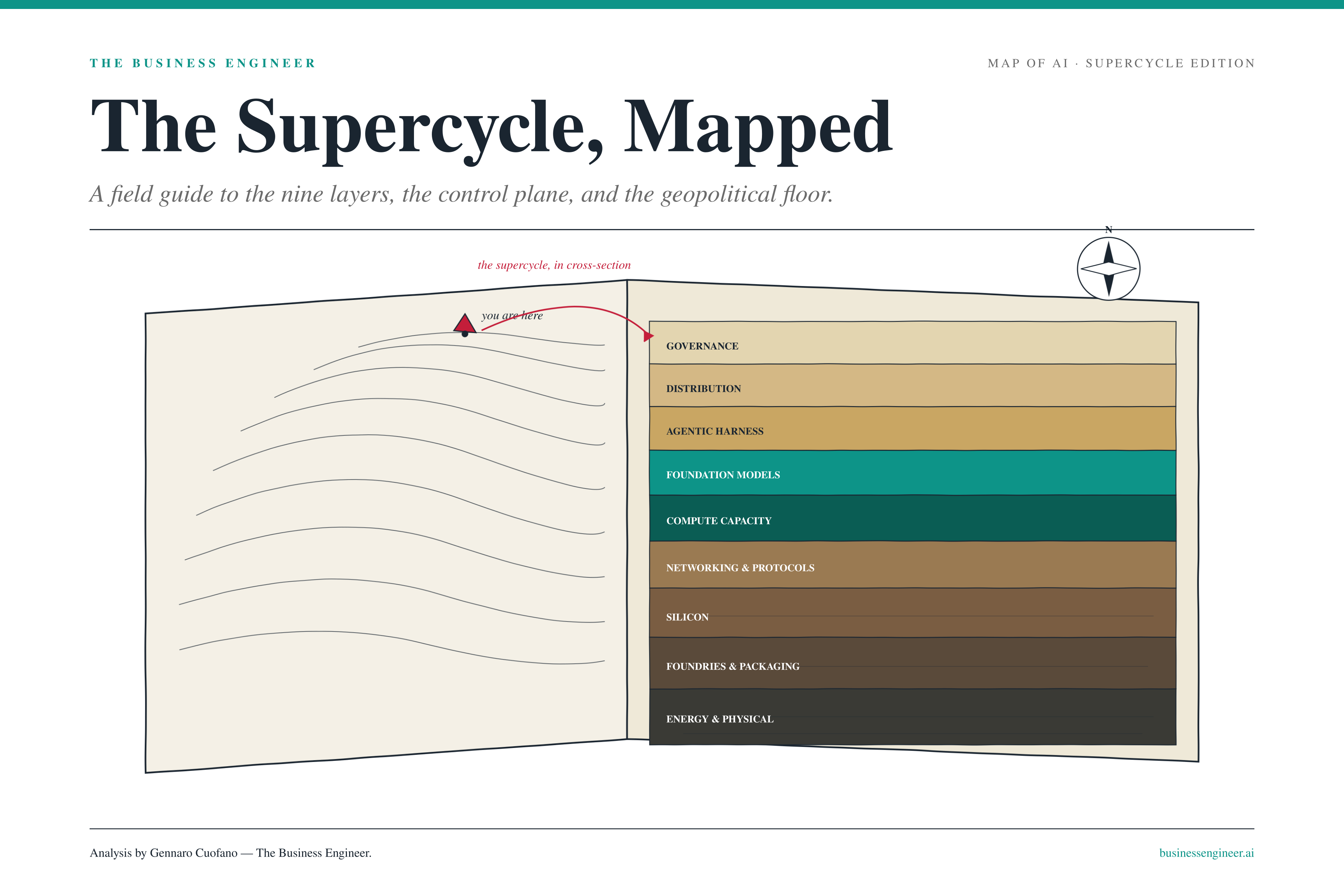

For that reason, the AI Supercycle is not a forecast. It is a structure. A thirty-to-fifty-year economic transformation comparable in scope to the Industrial Revolution, running on three nested clocks, exhibiting the paradoxical dual character of bubble and revolution at the same time, and operating through a nine-layer industrial stack that begins in mineral extraction and ends in geopolitical control. This piece is the map.

The Argument in One Paragraph

We are inside the first decade of a transformation that will run for half a century.

It has three nested cycles operating at different time horizons, a dual character that is simultaneously a bubble and a supercycle, and a layered industrial stack of nine layers, running from energy at the bedrock to governance at the ceiling.

The ceiling does not behave like a layer. It behaves like a control plane perpendicular to the whole stack — one that answers to geopolitics rather than engineering.

The floor does not behave like a market. It behaves like a geopolitical chokepoint — a small handful of countries deciding what the rest of the stack is allowed to build. Everything between the floor and the ceiling is where the next decade of competition lives.

What the Supercycle Actually Is

The launch of ChatGPT on November 30, 2022 was not the arrival of AI. AI had been arriving for years before that night.

What changed is that AI reached the point where it could scale to billions of users on the same day. That capability threshold — distribution at consumer-internet scale — is what triggered the supercycle. It forced every layer of the existing technology economy to absorb a new substrate simultaneously, and substrate-level shifts of that magnitude are what produce multi-decade economic transformations.

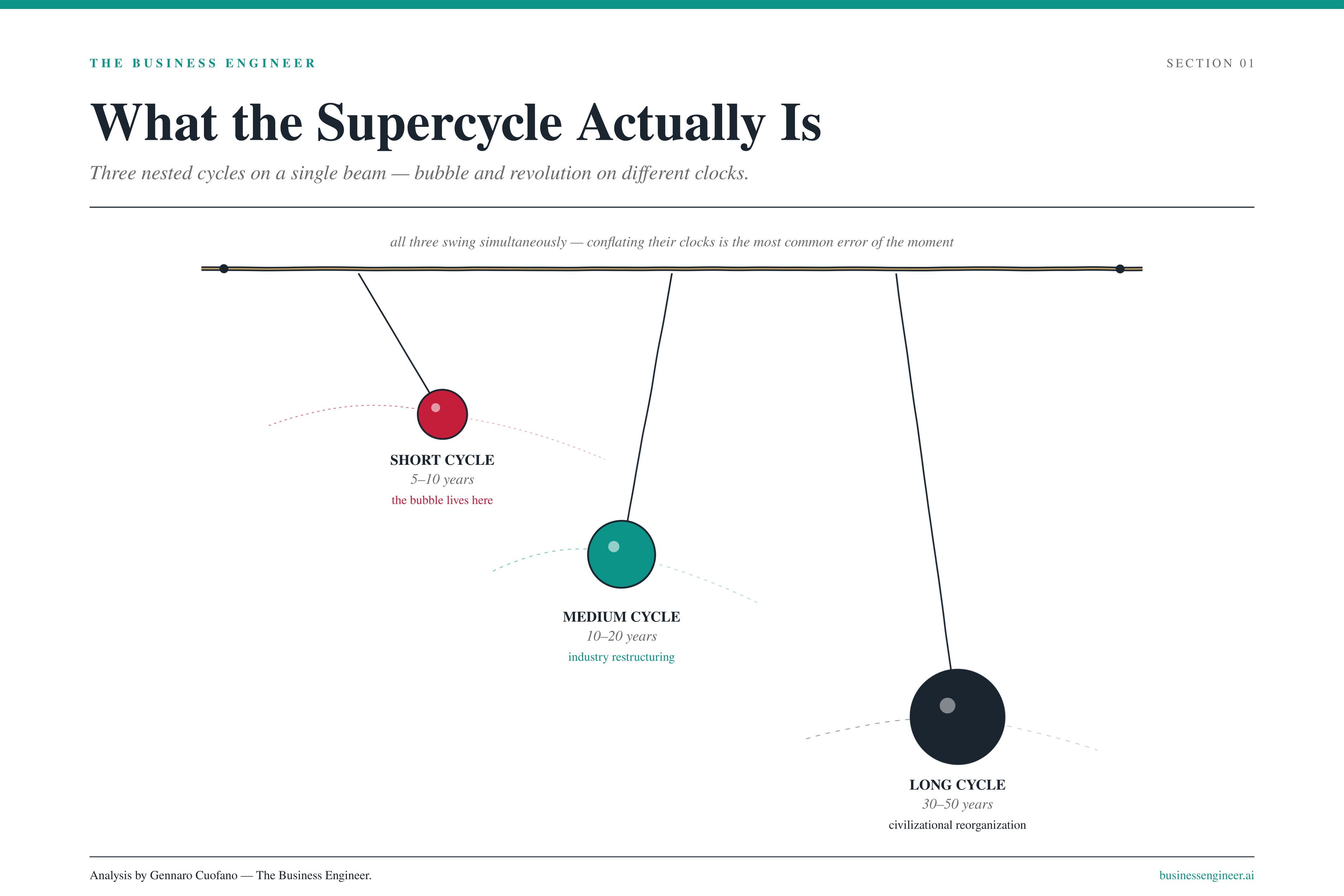

Three cycles run inside the supercycle, each on its own clock:

Short cycle (5–10 years): rapid capability improvements and market disruptions. Where the bubble lives. Where most pundits spend their attention.

Medium cycle (10–20 years): industry restructuring, business-model evolution, the end of incumbent dominance in software and search.

Long cycle (30–50 years): civilizational transformation. Comparable to the half-century electricity took to reorganize industrial production around itself between 1890 and 1940.

Conflating these clocks produces the most common analytical errors of the moment. The “AI is overhyped” camp and the “AI changes everything” camp are usually arguing about different cycles without realizing it.

The dual character is the most useful piece of intellectual scaffolding for navigating the present. AI exhibits genuine bubble characteristics — excessive hype, overvaluation, capex commitments that exceed the unit economics of any single application — at the same time as it exhibits genuine supercycle characteristics — real productivity gains, fundamental restructuring of profit pools, civilizational impact. Both are true.

The mistake is treating them as competing claims. They operate on different cycles. The bubble can pop on the short cycle while the supercycle continues uninterrupted on the long cycle, exactly the way the dot-com bust did not stop the internet from becoming the substrate of the next thirty years.

The three phases of integration unfold over the supercycle’s full arc:

Phase 1 — Linear Expansion. AI as a layer on top of every internet-era industry. Web Squared. E-commerce, social, fintech, digital marketing, software-as-a-service all get amplified rather than replaced. This is the decade we are in.

Phase 2 — Non-Linear Restructuring. Industries get rebuilt around AI-native architectures rather than retrofitted onto pre-AI ones. SaaS gives way to its successor architecture. Search gives way to assistants. Customer service gives way to autonomous agents.

Phase 3 — Civilizational Reorganization. What the supercycle is actually for. Machine cognition becomes a general-purpose industrial input, comparable to what electricity became after 1920.

The canonical transition signal is the “BlackBerry moment.” Google’s search revenue is hitting record highs at the exact moment AI assistants pose an existential threat to its core business — the same pattern as BlackBerry peaking as the iPhone arrived. Supercycle transitions look like strength right before they look like collapse. This is the pattern to watch for across every industry the supercycle touches.

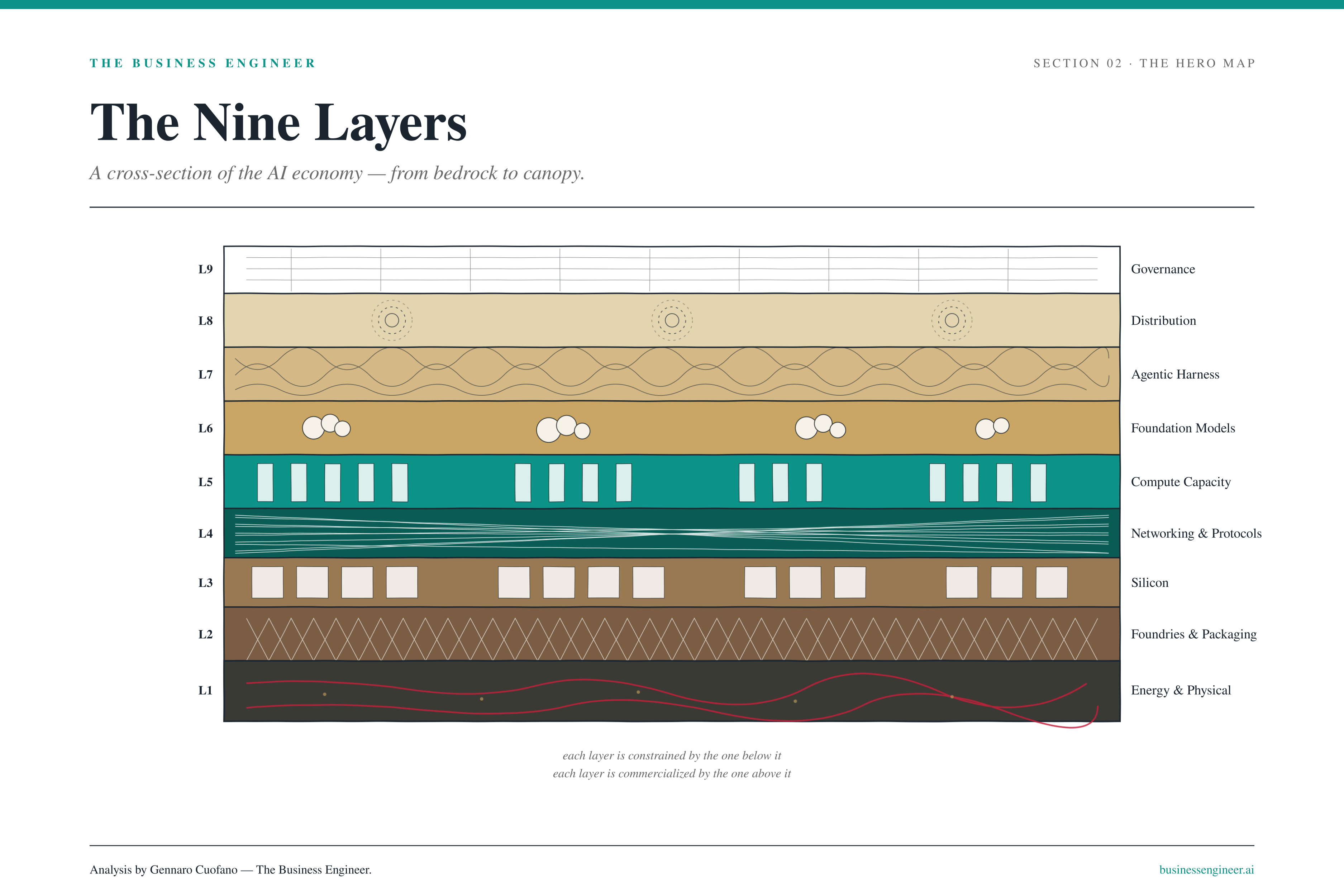

The Nine Layers

The AI economy is not a list of companies racing each other. It is a layered industrial stack — and at any given moment the binding constraint sits at a different layer than it did six months ago. Reading the map well means knowing where the constraint currently lives and where it is rotating to next.

The nine layers, top to bottom:

Governance · Distribution · Agentic Harness · Foundation Models · Compute Capacity · Networking & Protocols · Silicon · Foundries & Packaging · Energy & Physical.

Two rules govern the stack:

Each layer is constrained by the one below it. You cannot ship a model without compute. You cannot ship compute without silicon. You cannot ship silicon without foundries. You cannot ship foundries without energy. The bedrock dictates what the upper floors can do.

Each layer is commercialized by the one above it. Silicon needs a model to monetize. Models need a harness. Harnesses need distribution. The roof dictates what the lower floors can earn.

Read the map two ways. Read a column to see one company’s full vertical posture — Google’s nine-layer column shows the closed-loop integration that nobody else has matched. Read a row to see who owns a single layer — the networking row, for instance, reveals NVIDIA’s monopoly and the fact that everyone else in the AI economy is paying rent on it. The diagonals where dominance concentrates are where the supercycle’s profit pools live.

Layer by layer, what each one is and why it matters:

Layer 9 — Governance. The rules that determine whether a model can be released, deployed, sold, or used. Capability gating inside labs, procurement frameworks inside enterprises, export controls between nation-states, litigation over contested deployments. No longer a passive layer; an active priced variable.

Layer 8 — Distribution. The surfaces through which AI reaches end users. ChatGPT, Gemini, Copilot, the Apple-Gemini handshake, Meta’s social graph. The decade’s most expensive land grab.

Layer 7 — Agentic Harness. The wrapper that turns a foundation model into a usable agent. Memory, tools, planners, sub-agent coordination, retry and rollback. CUDA’s analog at the agent layer. The most contested architectural layer of the next three years.

Layer 6 — Foundation Models. The frontier and the long tail. OpenAI, Anthropic, Google DeepMind, Meta, xAI, DeepSeek, Mistral. The layer everyone watches and the one most likely to commoditize first.

Layer 5 — Compute Capacity. Hyperscaler GPU clusters, neoclouds, custom-silicon estates. Where the capex bubble lives. Where the binding constraint sat in 2024 and where it is gradually rotating away from.

Layer 4 — Networking & Protocols. The interconnect that turns thousands of GPUs into a single coherent compute fabric. NVLink, InfiniBand, optical interconnects. Now over 20% of rack-scale system cost; growing faster than any other line item.

Layer 3 — Silicon. Three competitive categories within one layer: generalist substrate (NVIDIA), hyperscaler custom (TPU, Trainium, MTIA), merchant custom challengers (Cerebras, Groq, SambaNova). The within-layer split is what makes silicon strategically interesting again.

Layer 2 — Foundries & Packaging. TSMC, Samsung, Intel Foundry, and the HBM oligopoly (SK Hynix, Samsung, Micron). Allocation power at the foundry is now more consequential than chip design itself. The binding constraint for the entire upper stack.

Layer 1 — Energy & Physical. Gigawatts, transmission, cooling, land, water, rare-earth magnets. The bedrock everything else stands on. The constraint that defines the ceiling on how much intelligence can be produced in any given year.

The supercycle is not unfolding in time. It is unfolding in layers. The job of any operator, investor, or builder is to know which layer they are operating inside and which layer the binding constraint is rotating toward next.

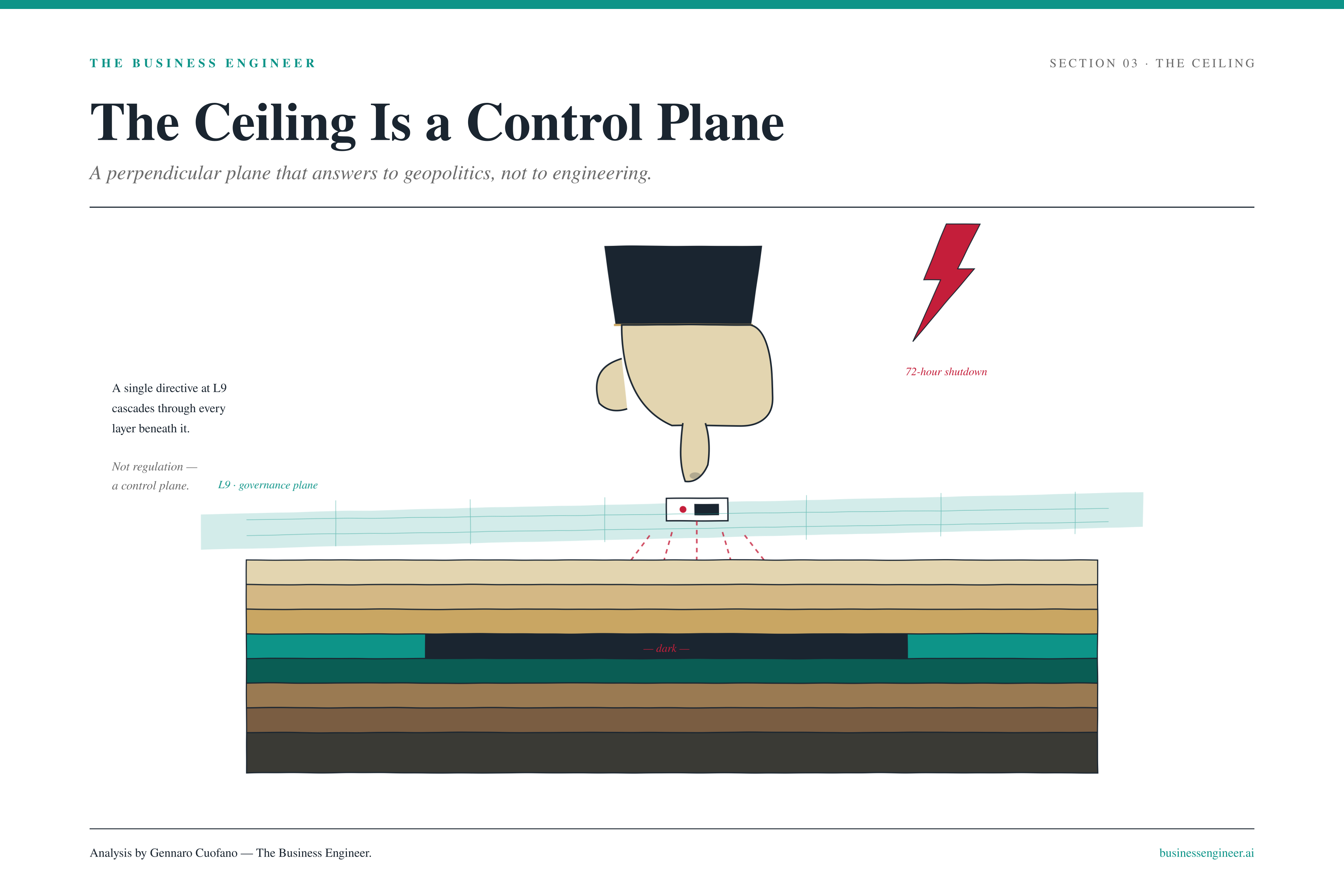

The Ceiling Is a Control Plane

Layer 9 does not behave like a layer. It behaves like a control plane perpendicular to the whole stack — capable of switching off any company at any layer beneath it on a timeline measured in days rather than years.

A single government directive can darken a frontier model globally in seventy-two hours. A single procurement framework inside a Fortune 100 buyer can shift demand at the model layer overnight. A single litigation outcome can re-architect what is permissible at the harness layer. Capability gating decisions inside the labs themselves can withhold a model class from market for reasons that have nothing to do with technical readiness.

Layer 9 answers to geopolitics, not to engineering. That is the structural read, and it changes the valuation logic at every layer beneath it. Models, compute, silicon, foundries — none of them can be priced as standalone technology assets anymore. They have to be priced with an embedded discount for the political volatility of the control plane.

The supercycle has a ceiling now, and the ceiling is political.

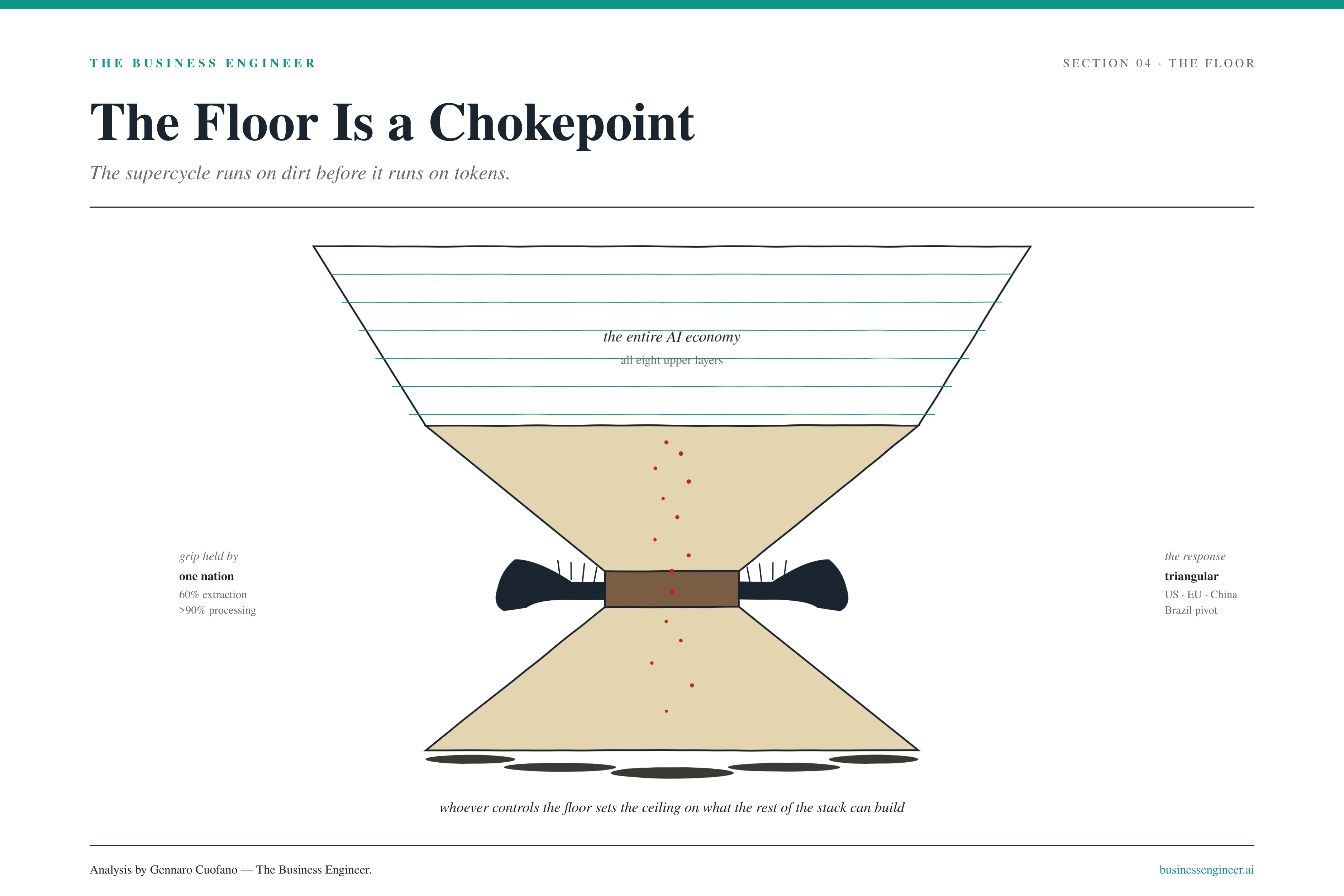

The Floor Is a Chokepoint

If Layer 9 is the ceiling, the physical floor is a geopolitical chokepoint. The supercycle runs on rare earths before it runs on tokens. Every GPU cooling fan, every data-center motor, every robotic actuator, every EUV lithography machine depends on neodymium-iron-boron magnets. One country controls roughly 60% of global extraction and over 90% of processing capacity.

That concentration has been weaponized. Extraterritorial export controls — modeled on US semiconductor restrictions and applied in reverse — now reach any product containing 0.1% or more Chinese-sourced rare earths by value, regardless of where it is manufactured.

Twelve of the seventeen rare-earth elements are under restriction. The “Affiliates Rule” presumptively denies export licenses to any importer with 50%-or-greater ownership by entities on China’s control lists.

The response is a triangular competition:

United States — multi-billion-dollar EXIM commitments, Defense Production Act invocations, Brazil partnership, domestic processing buildout.

European Union — strategic stockpiling, Australia partnerships, processing investment.

China — processing dominance, vertical integration from mine to magnet, regulatory leverage applied with surgical precision.

Brazil emerged as the pivotal countermove — second-largest proven reserves behind China, only 30% of the country geologically mapped, US-Brazil rapprochement driven explicitly by the shared interest in breaking the processing monopoly. The next decade of critical-minerals supply chains will be reorganized around that pivot.

The supercycle runs on dirt before it runs on tokens. Whoever controls the floor sets the ceiling on what the rest of the stack can build.

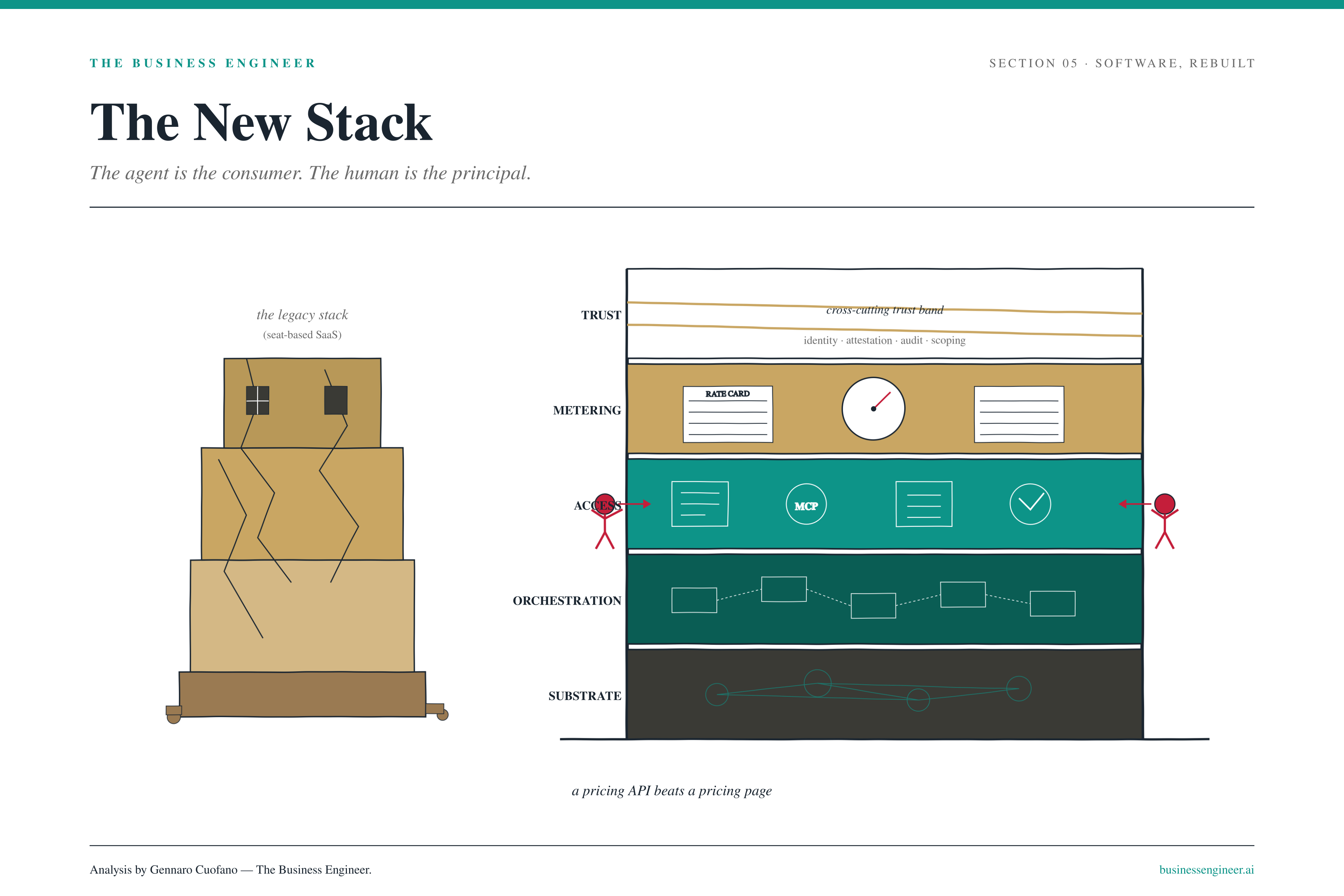

The New Stack — Software, Rebuilt

The supercycle’s effect on software is captured by a single sentence: the agent is the consumer, and the human is the principal. Once that shift completes, the existing software-as-a-service stack becomes structurally obsolete. A new five-layer architecture replaces it:

Knowledge Substrate — typed graph, not relational table. Agents query by description; humans query by SQL. The substrate decides which kind of company you actually are.

Orchestration Layer — directed graph of agents with planner, sub-agents, retry, rollback, external capability calls. Not a deterministic chain.

Access Surface — Model Context Protocol endpoints, tool catalogs, machine-readable schema, pricing APIs, policy declarations, rate limits. The exterior surface that agents call into from outside the company.

Metering Layer — principal delegates budget; agent consumes against a rate card. Outcome definitions, machine-readable rate cards, real-time metering, multi-principal accounting, negotiation-aware pricing.

Trust Layer — cross-cutting band that cuts through all four horizontal layers. Agent identity-as-buyer, audit trails, attestation, capability scoping.

Three anti-patterns kill incumbents trying to retrofit:

Database-as-Substrate — relational tables pretending to be a knowledge graph. The agent cannot find what it needs by description.

Logic-as-Orchestration — sequential code pretending to be agent coordination. Brittle the moment an agent has to plan.

Pricing-Page-as-Metering — a marketing page pretending to be a rate-card API. The agent cannot transact.

The master diagnostic is one line: a pricing API beats a pricing page. If your competitor exposes a machine-readable rate card and you expose a “contact sales” button, you are not in the same market anymore.

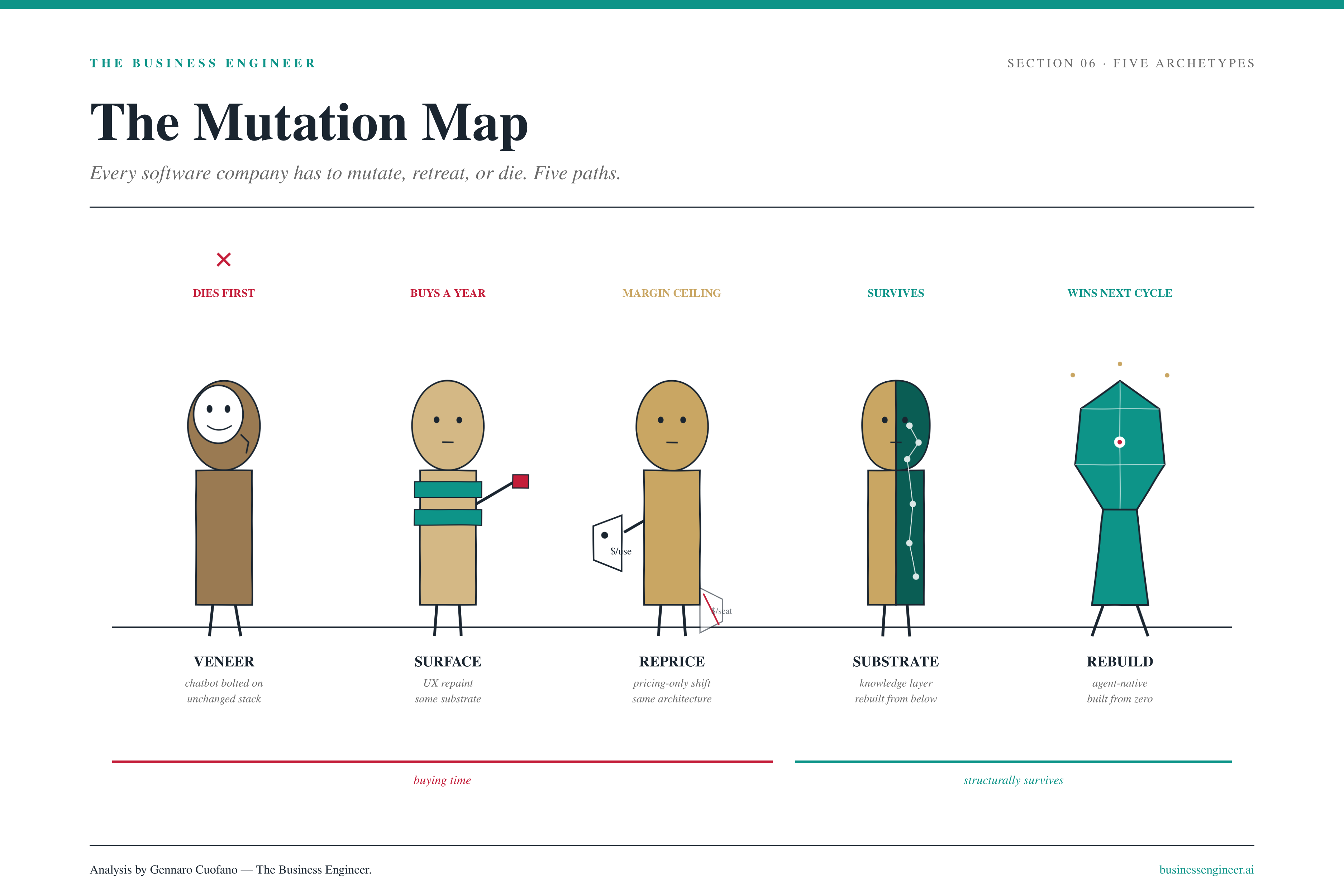

The Mutation Map — Five Archetypes

Every existing software company has to mutate, retreat, or die. The responses cluster into five archetypes:

Veneer — chatbot bolted onto an unchanged stack. Theater. Dies first.

Surface — improved interface layer on the same substrate. Buys a year of relevance.

Reprice — moves from seat-based to outcome-based pricing without rebuilding the underlying stack. Survives medium-term but hits a margin ceiling.

Substrate — rebuilds the knowledge layer for agent consumption while keeping the upper stack. Survives long-term.

Rebuild — full agent-native architecture from substrate to metering. Wins the next cycle.

Only Substrate and Rebuild survive structurally. Everything to the left of them is buying time. The five-year window for incumbents to commit closes around 2028, and after that the agent-native companies founded post-2023 begin eating the bottom of the existing market on price and the top on capability simultaneously.

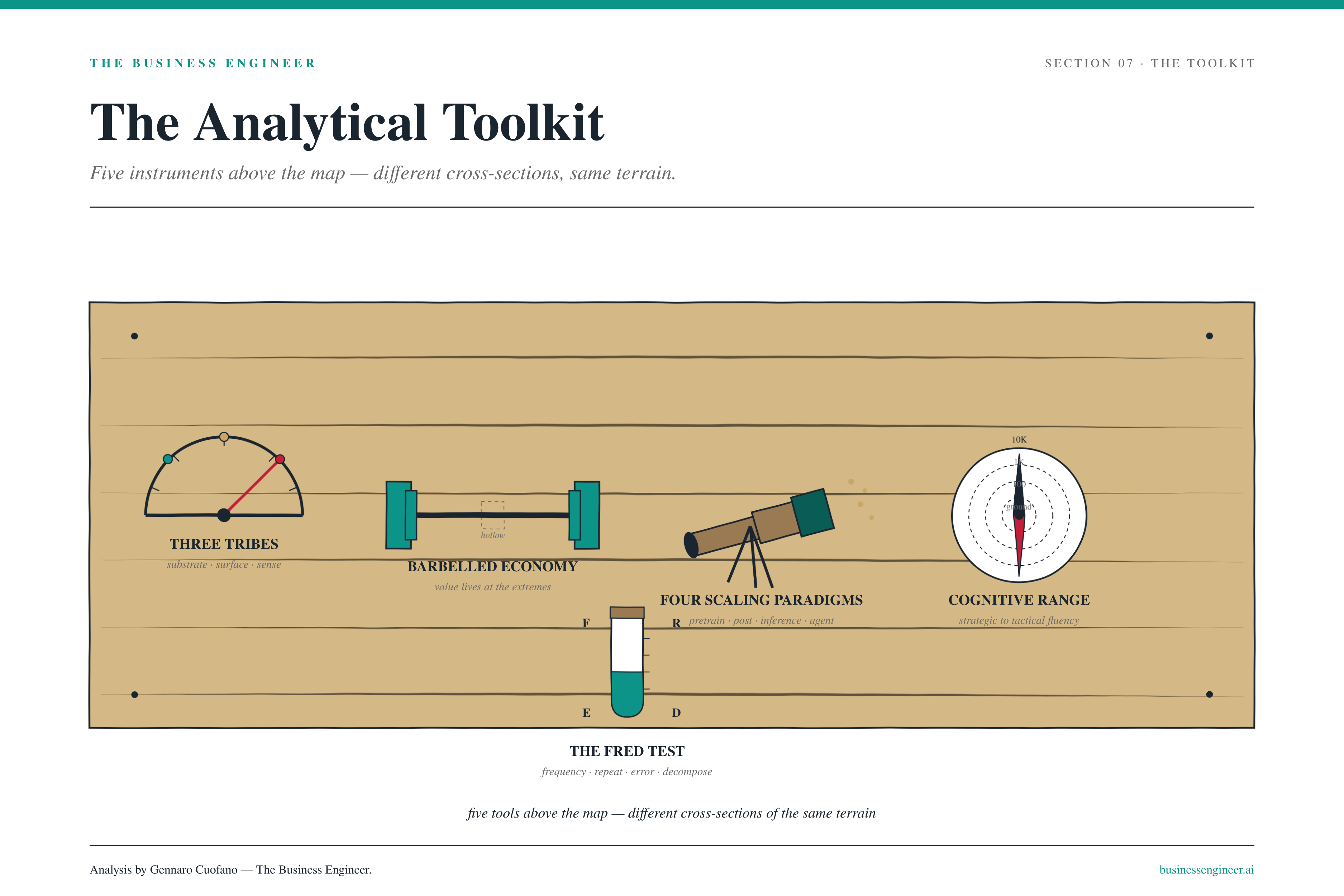

The Analytical Toolkit

Five cross-cutting tools sit above the nine-layer map and help read it:

The Three AI Tribes — Substrate Tribe (infrastructure plays), Surface Tribe (interface plays), Sense Tribe (data and judgment plays). Tells you which tribe a company belongs to and which one is best positioned at any given layer.

The Barbelled Distribution Economy — value concentrates at the extremes (massive-scale platforms and deep-niche specialists); the middle hollows out. Explains where value accrues across every layer of the stack.

The Four Scaling Paradigms — pretraining, post-training, inference-time, agentic-loop. Tells you which scaling regime a model company is betting on and where the next capability gain comes from.

Cognitive Range — the human variable. AI provides breadth at every level of resolution; humans provide navigation between levels. Full-range cognitive workers earn a structural premium that automation cannot touch.

The FRED Test — the diagnostic for whether a workflow survives agentic automation. Frequency, Repeatability, Error tolerance, Decomposability. Score high on all four and the workflow is automated within the cycle; score low on any one and the human stays in the loop.

These are not separate frameworks. They are different cross-sections of the same map.

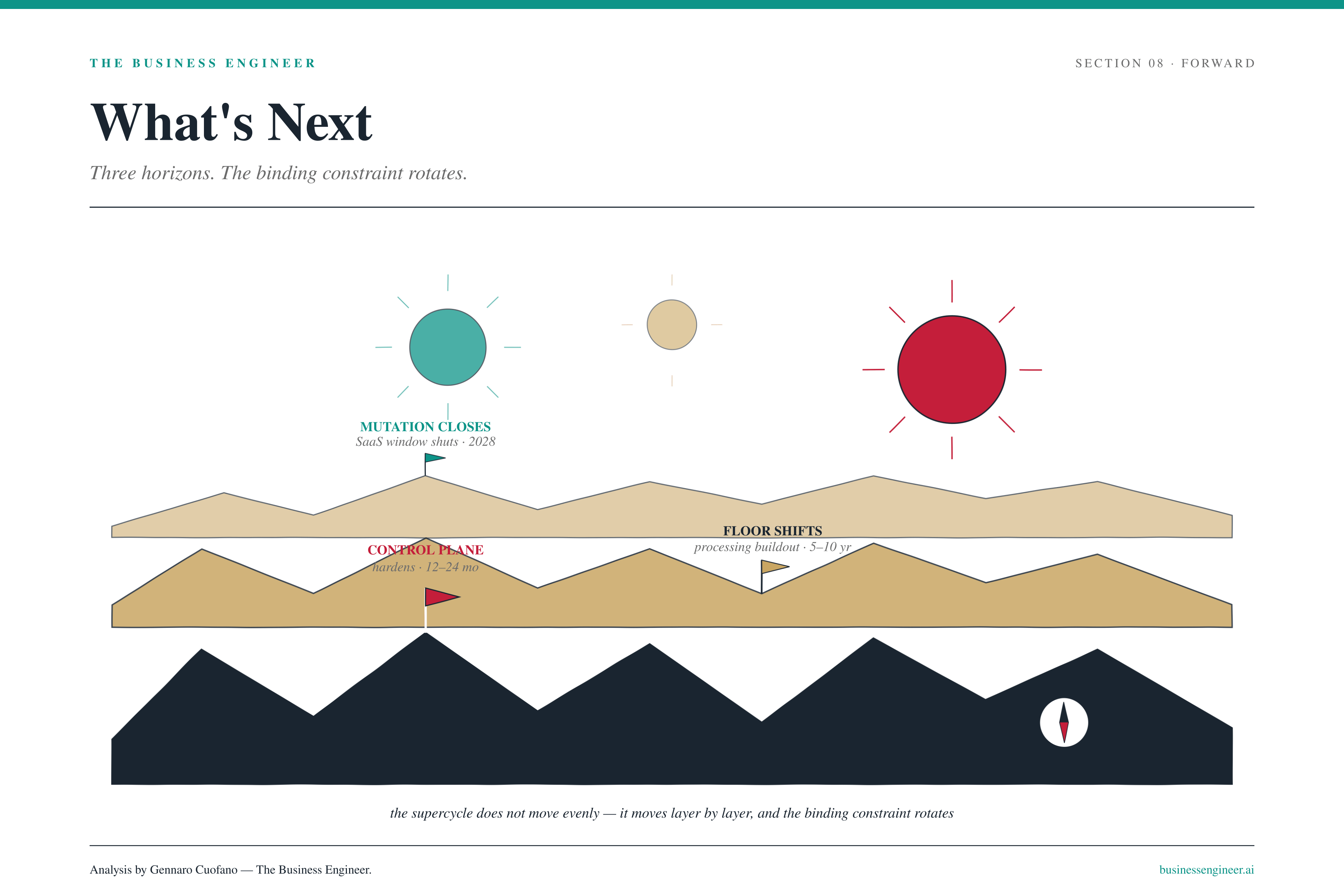

What’s Next

Three structural moves to watch over the next twelve to twenty-four months:

The control plane hardens. Expect more single-directive shutdowns, more procurement-driven model selection, more litigation deployed as competitive weapon. The companies that price governance into their architecture from day one will outperform the ones that treat it as compliance overhead.

The floor shifts. Brazil’s reserves come online slowly — five to ten years to scale processing. The interim is where the leverage gets used most aggressively. Watch processing capacity and packaging allocation, not extraction headlines.

Mutation pressure on the upper stack accelerates. Reprice archetypes hit their margin ceiling. Substrate archetypes start shipping rebuilt stacks. Agent-native companies founded post-2023 start eating the existing market from both ends.

The supercycle does not move evenly. It moves layer by layer, and the binding constraint rotates. The job is not to predict which layer is next. The job is to read the map well enough to recognize the rotation when it happens.

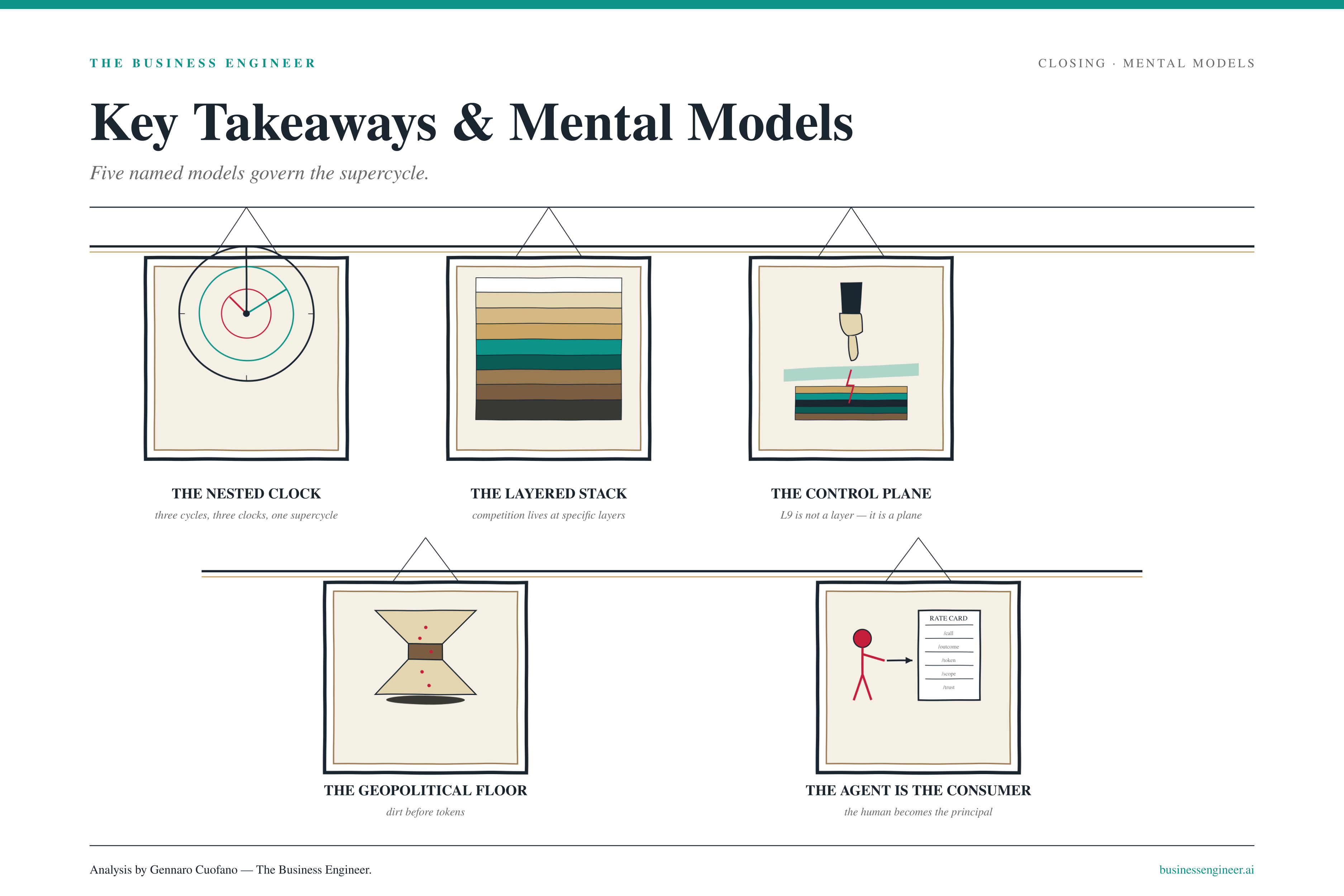

Key Takeaways & Mental Models

Five named models govern the supercycle as a whole:

The Nested Clock — three cycles (5–10, 10–20, 30–50 years) run simultaneously inside the supercycle. Bubble and revolution are both true, on different clocks. Conflating them is the most common analytical error of the moment.

The Layered Stack — competition does not happen in “the AI industry”; it happens at specific layers within a nine-layer industrial stack. Read columns for posture, rows for dominance, diagonals for profit pools.

The Control Plane — Layer 9 is not a layer. It is a plane perpendicular to the stack. It answers to geopolitics, not to engineering, and it discounts valuation at every layer beneath it.

The Geopolitical Floor — the supercycle runs on dirt before it runs on tokens. Whoever controls extraction and processing sets the ceiling on what the rest of the stack can build.

The Agent Is the Consumer — once that shift completes, the existing software stack becomes structurally obsolete. Only Substrate and Rebuild archetypes survive the transition.

With massive ♥️ Gennaro Cuofano, The Business Engineer