The Foundry Is the New Federal Reserve of AI

Once every ninety days, a chairman walks up to a podium in Taipei and delivers the closest thing the AI industry has to a Federal Reserve meeting. He announces how much capital the industry will get, at what price, on what timeline, and — crucially — how it will be allocated across competing uses. He does this without ever using monetary policy vocabulary, because the vocabulary of his industry is nanometers, wafers, and yields rather than basis points and reserve requirements.

But the function is the same.

This Thursday, C.C. Wei delivered TSMC’s second quarter results:

Revenue of $40.2 billion, up 33.7% year-over-year

Fifth consecutive record quarterly profit

Full-year growth revised up to “slightly above 40%” — from the previous “above 30%”

An additional $100 billion commitment to Arizona, bringing US commitment to $265 billion

13 more fabs planned in Taiwan

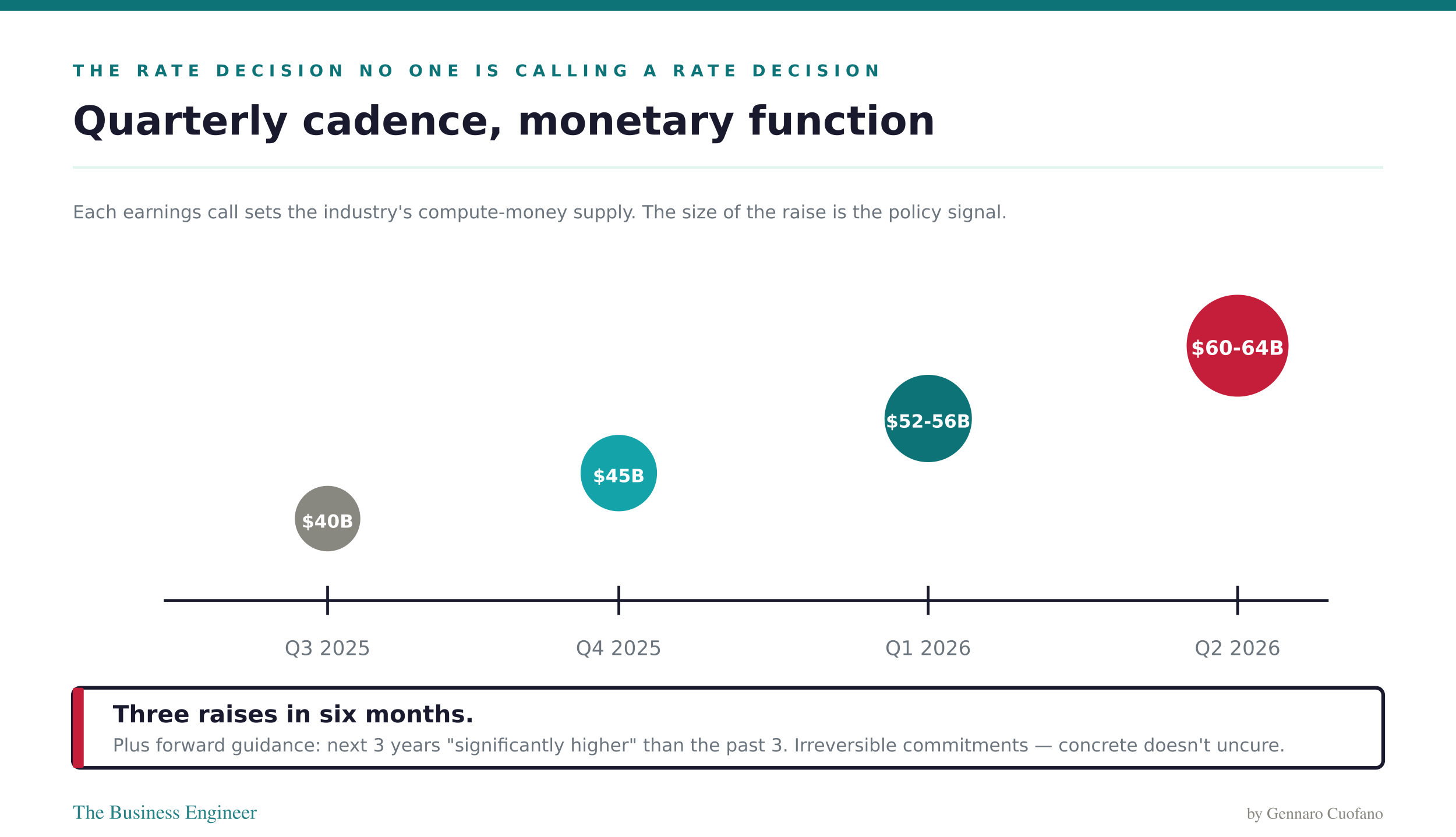

Capital spending raised for the third time this year, now $60–64 billion

Forward guidance that the next three years of investment will be significantly higher than the past three

TSMC’s stock fell 2%. Nvidia fell 2.4% alongside it. Arm fell 5.4%. Micron fell 5.6%. Marvell fell 8.7%.

The market read this as an overspending signal. That reading is wrong — and understanding why it’s wrong requires seeing TSMC as what it has actually become: the central bank of the AI industry.

The rate decision no one is calling a rate decision

When the Federal Reserve meets, it doesn’t just report the economy’s condition. It sets the price of money — which then transmits through banks, credit markets, business investment, employment, and eventually prices for everything else. The meeting is important not because of the reporting but because of the decision embedded inside it.

TSMC’s quarterly earnings do the same thing for AI compute. The numbers are the reporting. The capex line, the node roadmap, and the wafer allocation are the decision. And the decision has become so consequential that no other single event in the AI industry — not an Nvidia earnings call, not an OpenAI product launch, not a hyperscaler capex announcement — carries as much information about what the next three years of AI look like.

Consider what the market actually learned this week.

The wafer count barely moved. TSMC shipped 4,336 thousand wafer-equivalents in the quarter, versus 4,174 in the prior quarter — a 4% sequential increase. But revenue grew 12%. The eight-point gap is the average selling price of a wafer, which climbed from roughly NT$272,000 to NT$293,000 in a single quarter.

That’s not price extraction; TSMC explicitly refused to raise prices. It’s customers migrating up the technology ladder, and TSMC letting them do it at the margins the ladder produces.

Read as a central bank action, that’s the equivalent of the Fed shifting the composition of its balance sheet toward longer-duration securities without changing its overall stance. The base rate — the wafer count — is stable. The mix is where the policy lives.

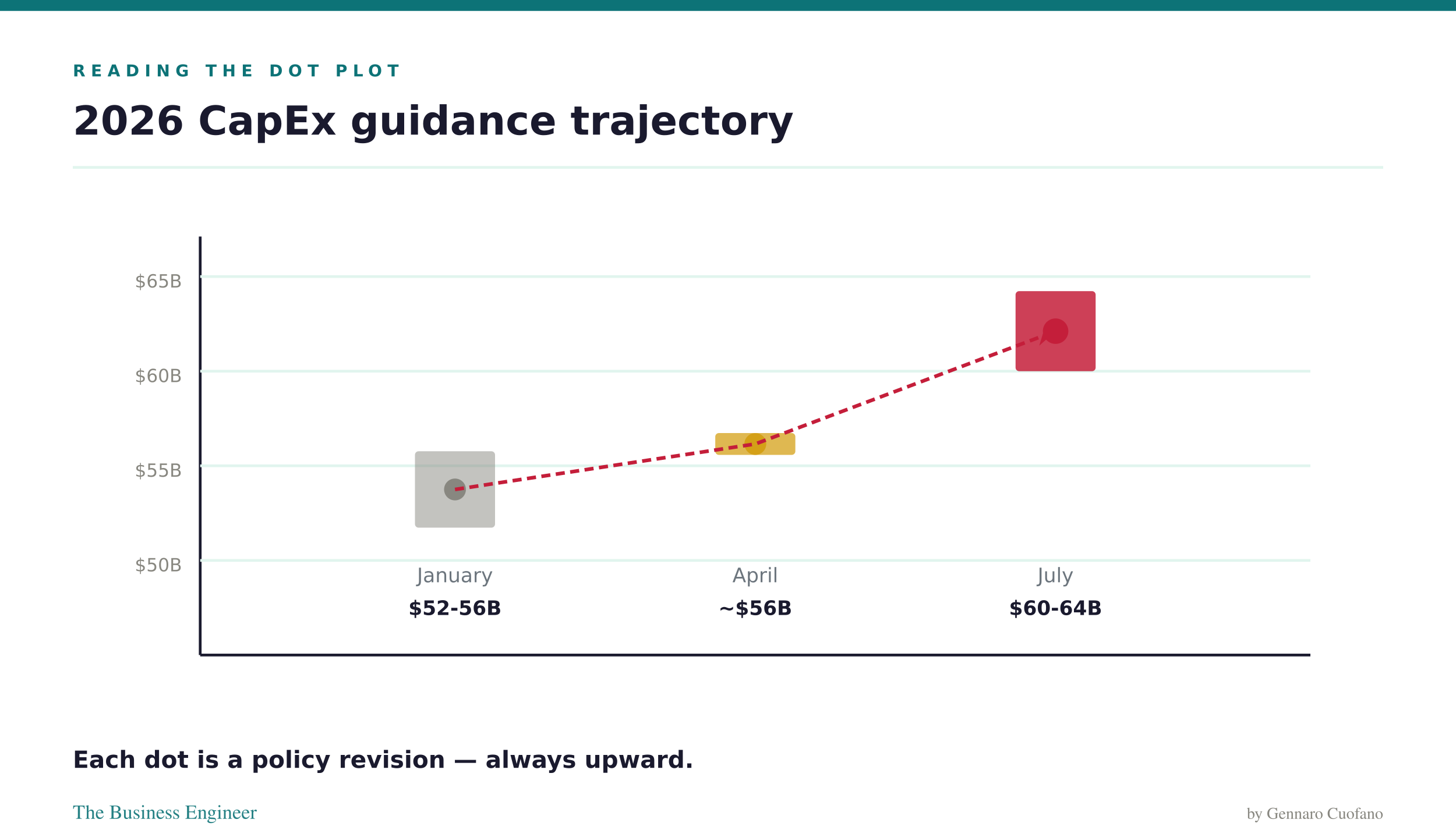

At the same time, TSMC’s capex path this year has moved three times:

January 2026: $52–56 billion

April 2026: closer to $56 billion

July 2026: $60–64 billion — plus $100 billion additional Arizona commitment, plus 13 Taiwan fabs

That is forward guidance in its purest form. And Wendell Huang, the CFO, went further in the Q&A: the next three years of investment will be “even more significantly higher” than the past three.

That is the equivalent of a central bank publishing not just a rate decision but a five-year path. And it’s being delivered by the only institution in the AI industry whose commitments cannot be reversed. Concrete doesn’t uncure. Fabs don’t relocate. Nodes don’t undevelop. Every dollar of TSMC’s capex is a physically irreversible bet on what AI demand will look like in 2028.

Reading the dot plot

What did the guidance actually say?