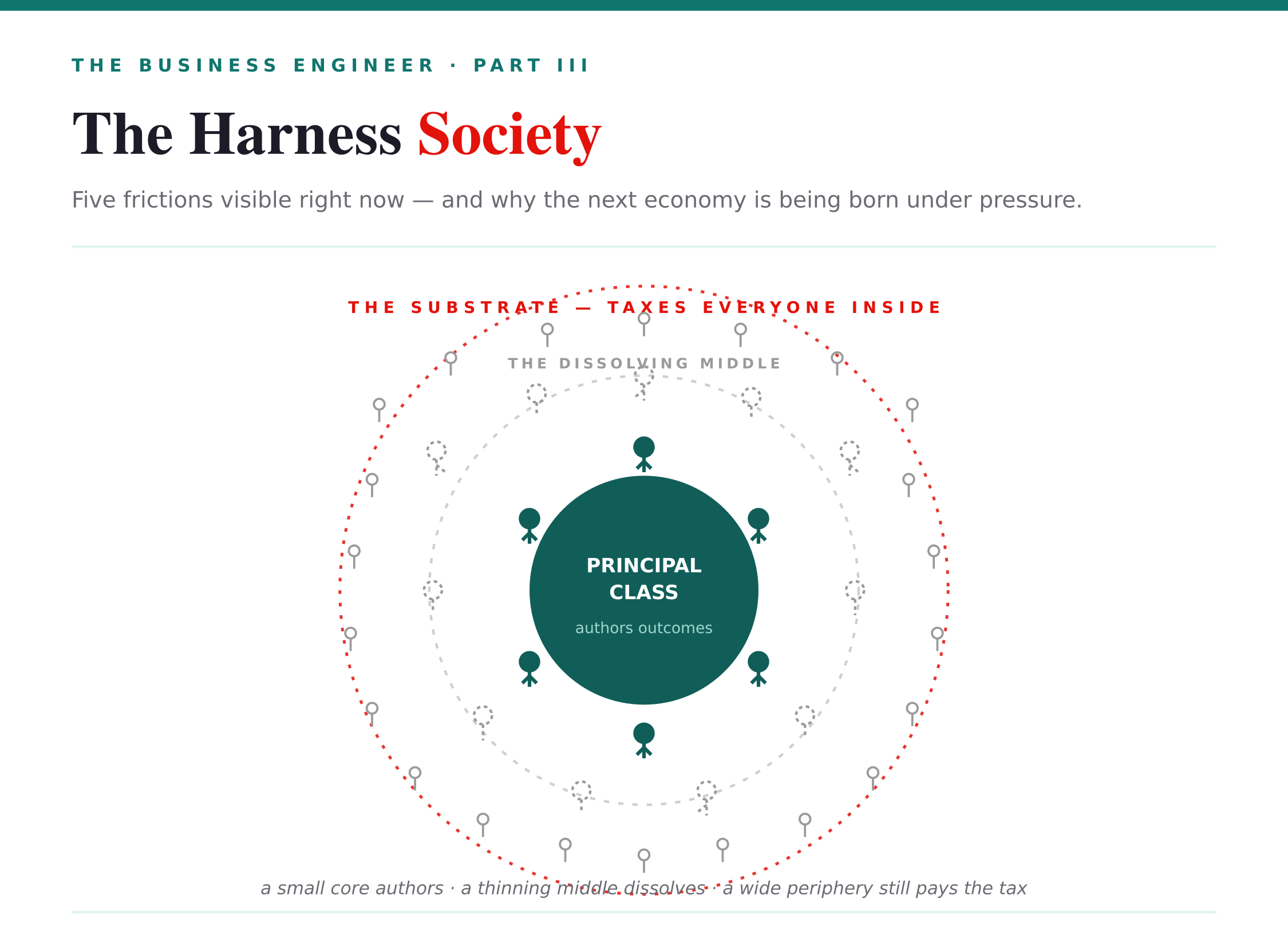

The Harness Society

I’ve written two pieces about what it looks like to live inside a harness of agents as one person — how I got there, and what the daily texture of it is. This one steps back from the desk.

Why I Ended Up in the Harness

A few days ago, I explained how, over the last eighteen months, the way I work has completely changed.

My Life in the Harness

I don’t work in a chat window anymore. I work in the Business Engineer’s harness.

Because the same forcing function that pulled me out of operating is now reorganizing everyone else, and the receipts are landing.

What follows is what I see. Not predictions — patterns. Five frictions, each one a force fighting another, each one already visible in the numbers. And one frame to hold above them all, because it changes how the rest reads:

You do not get to opt out of the harness society. It is cascading down to you whether you participate or not.

Start there.

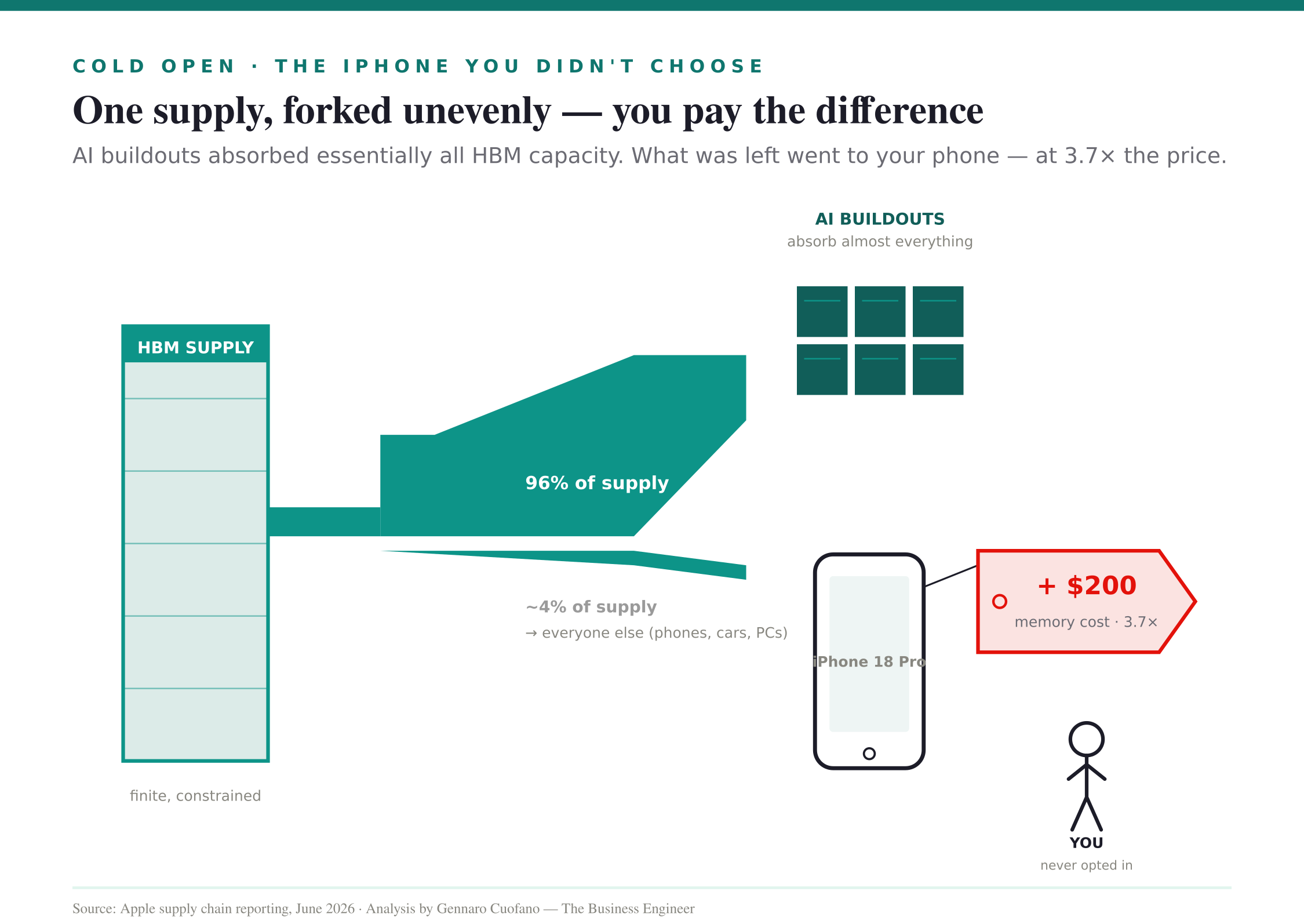

Cold open: the iPhone you didn’t choose

The iPhone 18 Pro is projected to cost about $200 more than its predecessor. The reason is mechanical: memory chip prices have risen roughly 3.7× in a year because AI buildouts have absorbed essentially all available HBM capacity. Apple is not an “AI company” in the frontier-lab sense. It still pays the AI tax — and passes it through to you.

That’s the entire piece in one consumer transaction. You didn’t sign up for the harness society. You’re paying for it anyway, because the inputs your phone needs are being absorbed by an economy you didn’t agree to join. And the iPhone is the easy case — the one where the cost is visible on a sticker.

The harder cases — power grids, talent markets, the political bandwidth absorbed by the AI story itself — work the same way. The harness society is not a destination one walks toward. It is a substrate the rest of the economy is already inside, and the people who never thought about it are paying their portion silently.

Five frictions follow. Each is a force fighting another. Each is already measurable.

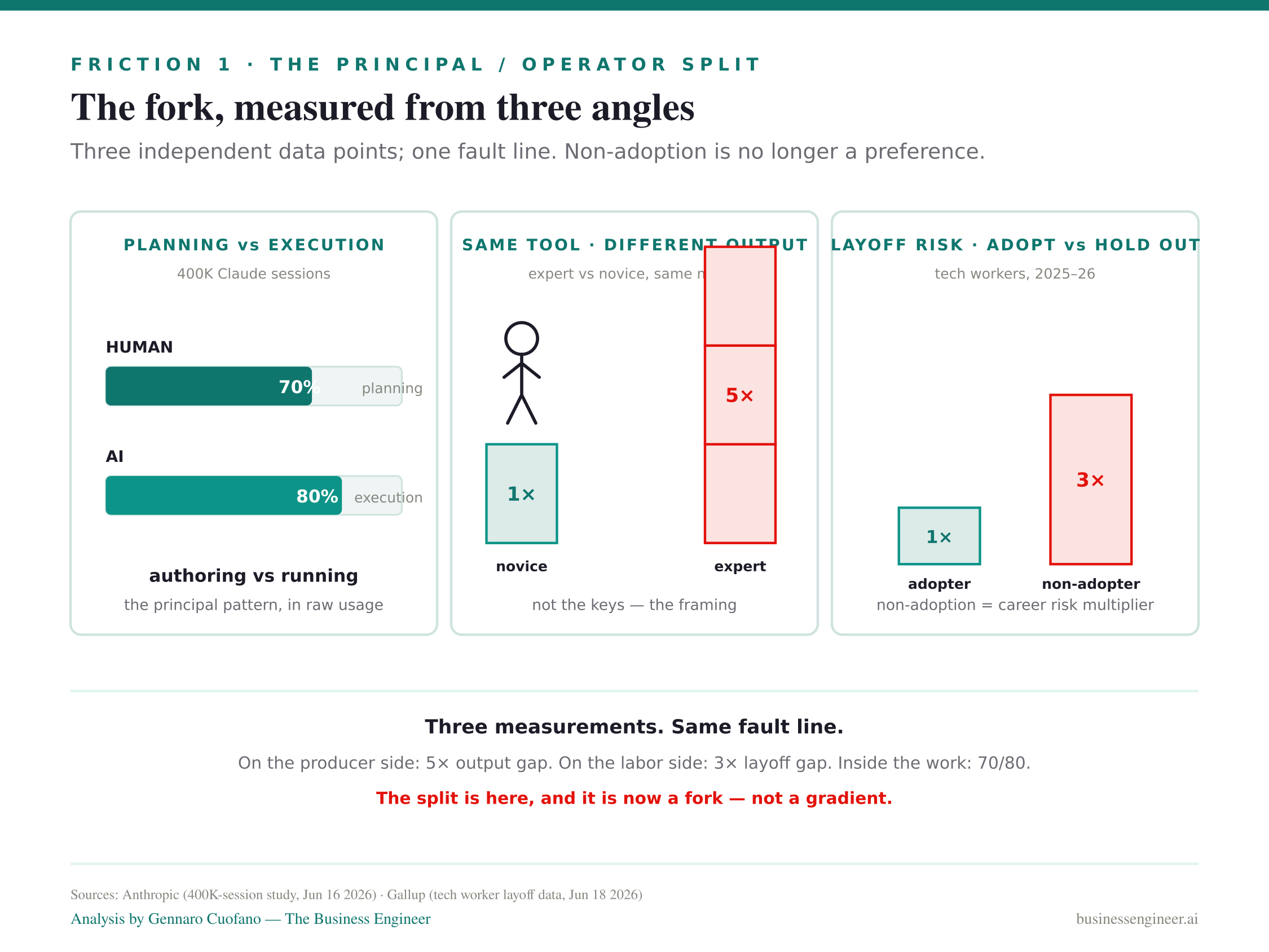

Friction 1 — The Principal / Operator split is here, with receipts

For two years the line “AI will divide workers into a small group who direct it and a large group who compete with it” has been theory. As of last week, it is measurement.

Anthropic published a study of 400,000 real Claude sessions, and the structure is unambiguous:

Humans make ~70% of the planning decisions. AI handles ~80% of the execution.

The same model produces 5× more output for an expert than a novice.

Domain expertise dominates over coding background — occupations cluster within seven points of one another regardless of technical fluency.

Debugging fell from 33% to 19% of session activity. Building rose 43%. Work is moving up the value stack in real time, inside the same tool.

That is not a trend; it is the Accountability Floor showing up as a usage pattern. The people who get 5× output are not pressing keys faster. They are better at the part the model cannot do — deciding what is worth doing and what “good” looks like before the agent runs. The 70/80 split is the principal at work: humans authoring, models executing.

Then Gallup, separately: tech workers who have not adopted AI face roughly 3× the layoff risk of those who have.

The split is now visible from both sides. On the producer side, a 5× output gap between expert and novice using the same tool. On the labor side, a 3× employment-risk gap between adopters and holdouts. That is not a gradient. It is a fork.

The structural read: non-adoption stopped being a preference and became a career risk multiplier. That is true even for capable, experienced workers — especially for them, because the ones being out-produced are usually the ones who used to be good at the layer the machine just took.

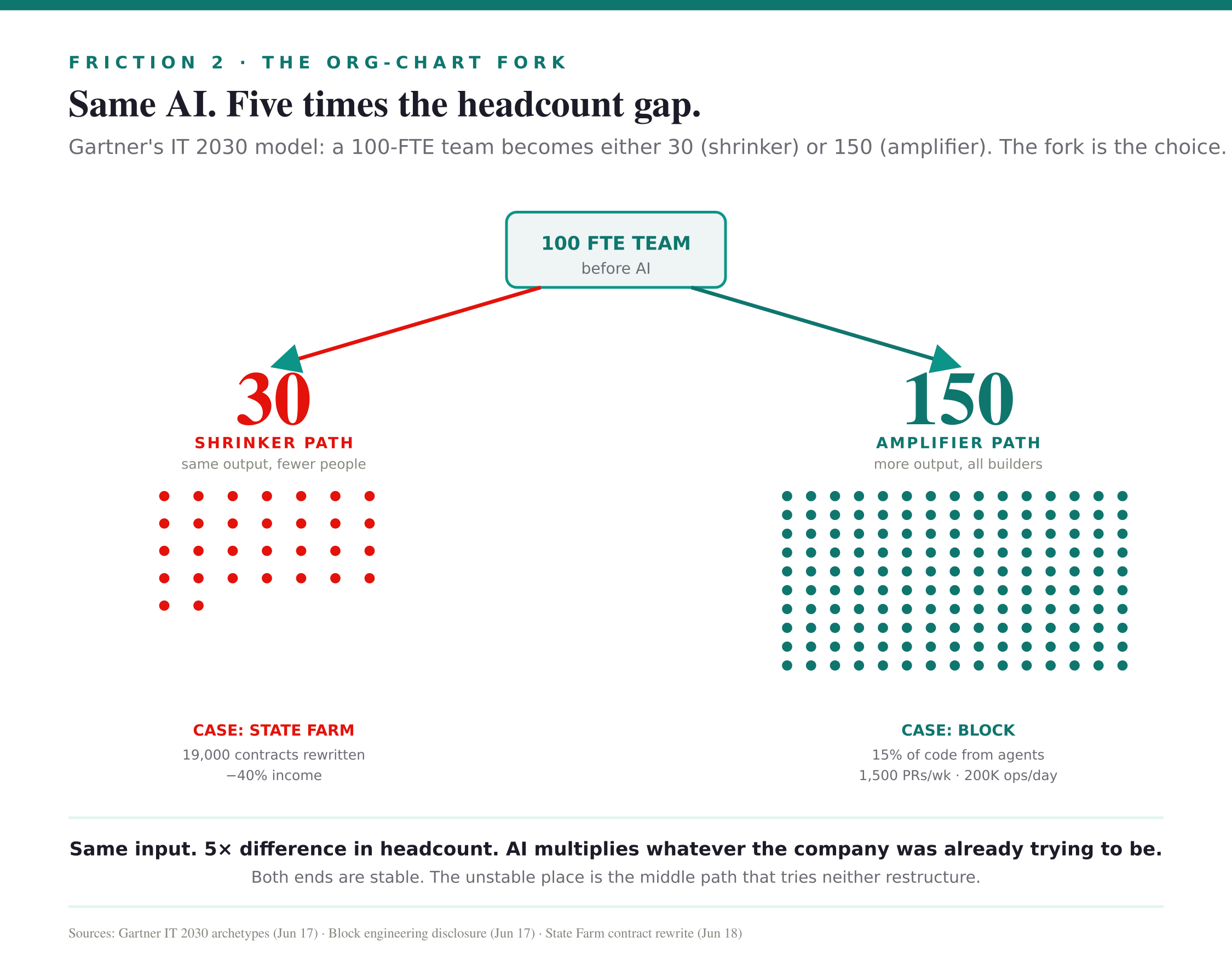

Friction 2 — The companies forking, with two extremes already visible

The same data set shows that AI does not push every company in the same direction. It pushes them in opposite directions depending on what they decide they are for.

Gartner’s IT 2030 model lays this out cleanly. A 100-FTE IT team, run through AI, becomes one of two things:

30 FTE producing the same output (the shrinker: same work, fewer people, lower cost), or

150 FTE, all builders, producing far more (the amplifier: same people, more output, redefined work).

Same technology. Two opposite org charts. The fork is not AI; the fork is what the company chose to do with the leverage.

Both ends are running, with names:

The amplifier case: Block (Square’s parent). Their internal “BuilderBot” agent produces ~15% of all production code shipped at the company. Roughly 1,500 pull requests merged per week. Around 200,000 agent operations per day. Tasks that took months take days. The system is triggered from a Slack message — a frame, set by a human, executes through a swarm. This is the harness, in production, at scale, with the headcount intact.

The shrinker case: State Farm. 19,000 agent contracts rewritten. Benefits cut. Retirement eliminated. Commissions tied to AI-tracked metrics. Income reductions of up to 40%. Meanwhile Progressive — running an AI-driven underwriting model — has overtaken State Farm as the #1 U.S. auto insurer. The shrinker pattern is not speculative; it is a finished restructuring with measurable consequences for the people it touched.

The pattern across both:

AI does not decide the org chart. It amplifies whatever the company was already trying to be.

Shrinkers shrink. Builders build. The technology is the multiplier; the choice is the company’s.

This is the structural reason most transitions will be painful. The political weight inside almost every organization is concentrated in middle management — and middle management is the layer most exposed to either path. The amplifier path turns middle managers into orchestrators of agent swarms (a new and difficult job). The shrinker path eliminates the role they currently occupy. Expect the fight inside organizations over which path to take to be more bitter than the one happening in public, because the people deciding the path are the people most affected by it.

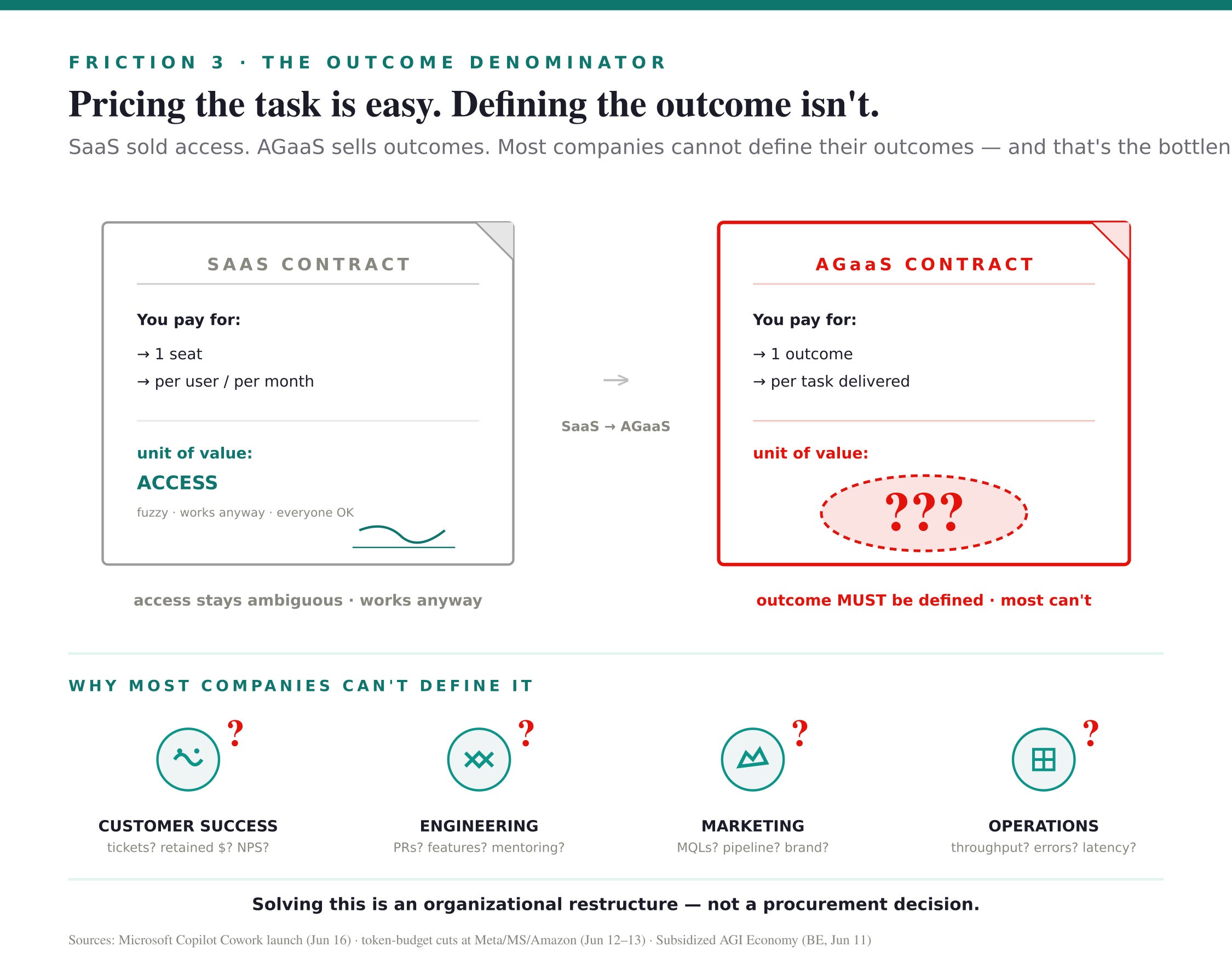

Friction 3 — The hardest problem isn’t pricing the task. It’s defining the outcome.

Per-seat software pricing held for nearly twenty years. That ended last week.

Microsoft launched Copilot Cowork at $0.01 per task — explicitly described as the first pricing-model change in nearly two decades. Nadella was direct: the unit being priced is no longer a user-month; it is a piece of work an agent completes. That is the SaaS → AGaaS transition I have been describing in the prior pieces, with a date stamp on it.

But the story most read out of this announcement misses what is actually hard about the transition. The token-cost stress is real — Meta, Microsoft, and Amazon all cut internal AI token budgets in the last fortnight; Uber burned its annual AI budget in four months; agentic AI consumes roughly 1,000× more tokens than chat for equivalent work; Microsoft canceled internal Claude Code licenses while expanding Copilot. Nadella himself called tokenmaxxing “addictive”. Those numbers will compress over the next 12–24 months as token deflation does its work.

The deeper problem won’t compress on its own. It is this: most companies cannot define what the outcome of a task actually is at the granularity an AGaaS contract requires.

Per-seat SaaS worked because the unit being purchased was access — a fuzzy, hard-to-measure good that everyone could agree on the price of without agreeing on the value. Per-task AGaaS does not have that luxury. The vendor charges per outcome delivered. The customer pays per outcome received. And both sides have to know what an outcome is. Most companies do not.

Consider the gap:

What is the outcome of a customer-success interaction? Resolved tickets, retained accounts, expanded contracts, satisfaction scores, all of them weighted somehow? Most orgs don’t have a definition.

What is the outcome of a software engineer’s day? Merged PRs, shipped features, reduced incidents, mentored juniors, refactored debt? Most orgs don’t have a definition.

What is the outcome of a marketing campaign? Impressions, MQLs, pipeline, attributable revenue, brand lift? Most orgs argue about it for years.

When the unit being priced is a seat, the outcome can stay ambiguous. When the unit being priced is a task, the ambiguity is the bottleneck. Companies cannot buy AGaaS at scale until they can articulate what their outcomes are, and articulating outcomes is an organizational restructure, not a procurement decision.

The revenue impact, where companies do solve this, is enormous. The Block case is what it looks like when a company restructures around outcomes: a Slack message becomes a frame, the frame becomes 1,500 PRs a week, the unit of value is the merged change, and it is measurable. The companies that build that scaffolding internally will see 5–10× output gains, possibly more. The companies that try to buy AGaaS without doing the restructure will spend money, fail to measure return, and conclude that AI “doesn’t work for us.” Both outcomes are happening simultaneously in the same market.

There is a clean structural symmetry worth naming here. The frontier labs are running the same problem in reverse. They are subsidizing power users at deeply negative margin to acquire workload signal at the frontier of difficulty — because they, too, cannot yet define what the outcome of an agentic task should be without watching real users grind real problems against it. The labs are buying outcome-definition data from power users at the same moment customer companies are trying to sell their own work as outcomes to vendors. Same denominator problem, opposite sides of the trade.

The outcome denominator is the load-bearing organizational problem of the next three years. Whoever solves it inside a company captures the AGaaS productivity multiplier. Whoever does not, doesn’t.

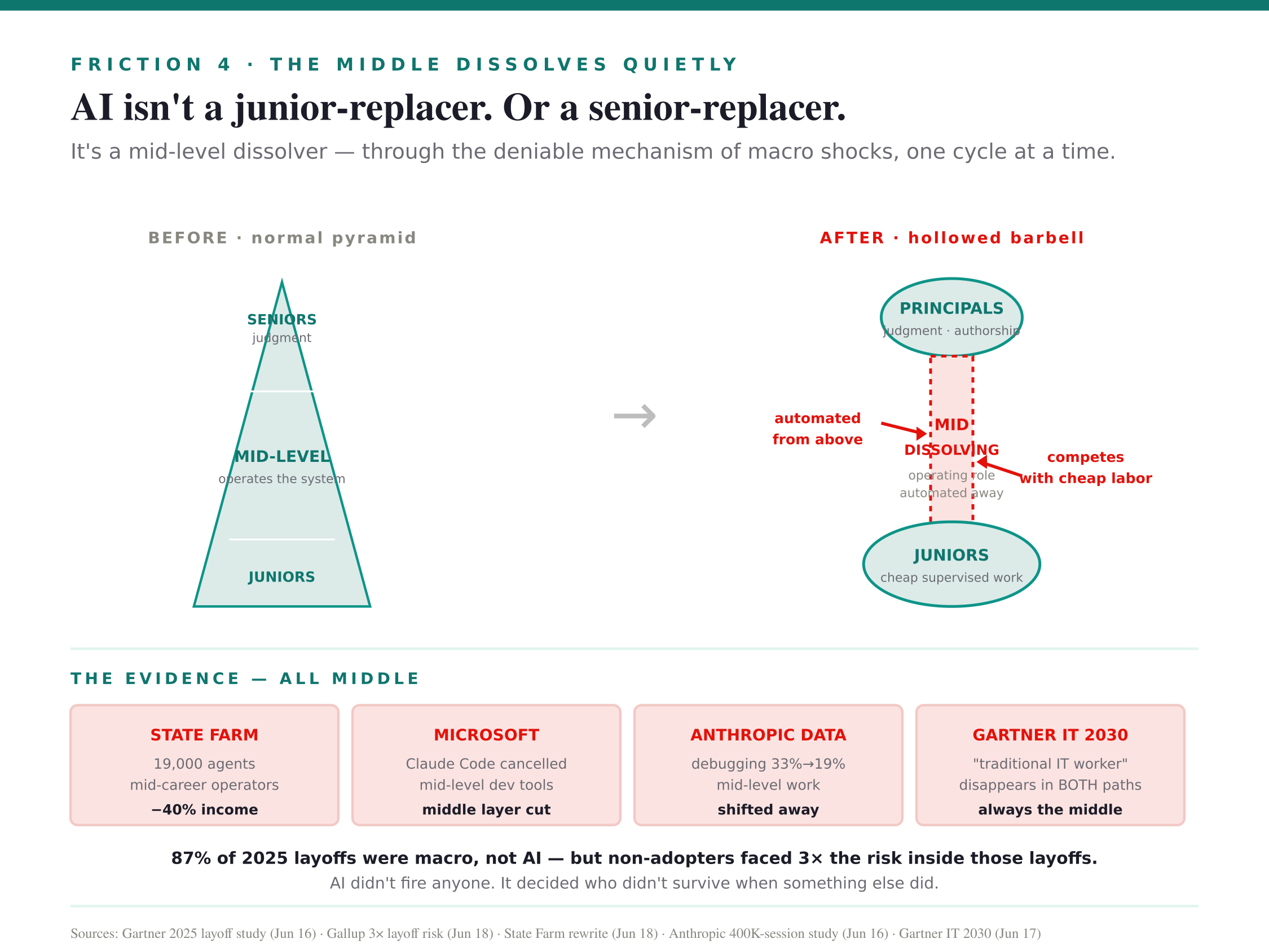

Friction 4 — The middle dissolves quietly

Here is the friction the political discourse keeps getting wrong.

Gartner, last week: of all 2025 layoffs studied, only 1% were AI-productivity-driven. Repositioning layoffs — companies pivoting to AI strategy — dropped from 17% to 7%. A full 87% of layoffs were macroeconomic, not AI at all.

Read in isolation, that is reassuring. Read against the Gallup 3× number, it inverts. AI is not doing the firing. It is deciding who survives the macro shock when one arrives. The displacement is not loud, broad, and AI-branded. It is quiet, selective, and macroeconomic-shaped — and consistently weighted against the people who did not restructure their work.

The harder question is: who is being filtered out, exactly? The data and the cases point at a non-obvious answer. It is not the juniors. It is not the seniors. It is the middle.

Look at where the displacement is actually landing:

State Farm’s 19,000 agent contracts — these are not entry-level workers. They are mid-career independent insurance agents, the operating layer between underwriting (top) and customer-facing service (bottom). The middle.

Microsoft’s Claude Code cancellations — these were mid-level developer tooling subscriptions. The cheap stuff at the bottom stayed; the high-end enterprise stayed; the middle got cut.

Anthropic’s session study — debugging (mid-level technical work) fell from 33% to 19% of activity; building (senior-level authoring) rose 43%. The activity mix shifted away from the middle.

Gartner’s IT 2030 archetypes — the role that disappears in both the shrinker and the amplifier paths is identical: “traditional IT worker doing manual tasks.” Mid-career operators of established systems. The middle.

The pattern is consistent across every data point: AI is not a junior-replacer or a senior-replacer. It is a mid-level dissolver. Juniors survive at the bottom because supervised execution is still cheaper than agentic supervision in most settings, and because juniors are the cheapest training pipeline a company has. Seniors survive at the top because their value is judgment, authorship, relationships, and accountability — exactly the bedrock the bedrock-piece pointed at. The middle is where competence-at-operating used to live, and operating is what just got automated.

This is more politically explosive than a broad displacement would be, for two reasons:

It is deniable. Every individual firing has a non-AI cause: budget cuts, restructuring, “performance.” No company is forced to say “we let her go because she did not restructure her work.” But statistically, that is largely what happened.

It compounds. Each downturn becomes an additional filter. The principal class gets reinforced at the top; the junior class survives at the bottom as the training pipeline; the middle gets winnowed. By the third macro shock, the workforce has been silently restructured into a barbell without anyone announcing the restructuring.

The harness society is not producing dramatic firings. It is hollowing out the middle of the labor market, one macro shock at a time, deniably.

And the political weight of the people being hollowed out is, in most countries, the political weight of the median voter.

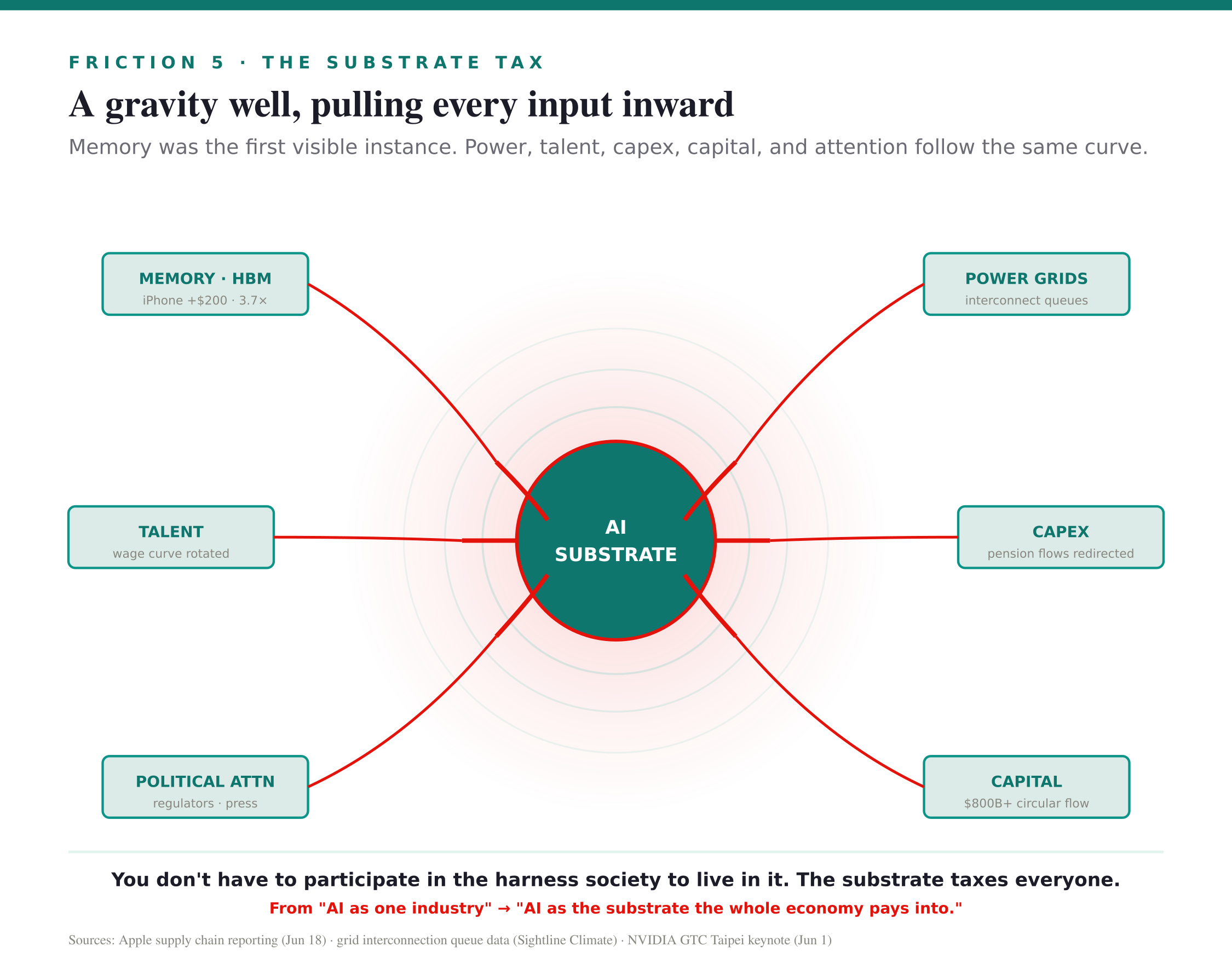

Friction 5 — The substrate tax

Back to the opener — but now widened beyond consumer electronics.

The iPhone case is the most legible instance of a pattern about to repeat across many goods and markets: AI buildouts are pulling key inputs out of every other industry that needs them, and the prices in those industries are reorganizing around that absorption.

Memory is the visible case. The next instances are already running:

Power grids. Data center buildouts are absorbing grid capacity that was assumed available to homes, factories, and existing commercial customers. New industrial projects are quietly losing interconnection slots to AI campuses willing to pay more and wait less. Power is being priced as if AI demand is the only demand that matters.

Talent. A few thousand people doing frontier ML are compressing technical wages across the entire economy. Companies that have nothing to do with AI compete with hyperscaler comp because their engineers can leave for it. The wage curve has rotated.

Capex absorption. Frontier-lab capex commitments are at a scale that crowds out other infrastructure investment. The pension funds and sovereigns financing the AI buildout are not financing other things at the same scale.

Political and regulatory bandwidth. Legislators, regulators, journalists, and academics now spend a disproportionate share of attention on AI — at the expense of every other policy question. The harness society is buying attention as an input the same way it buys memory.

This is the move from AI as one industry to AI as a substrate the whole economy now pays into. Substrates do not ask permission. They reshape the prices and the attention around them.

You do not have to participate in the harness society to live in it. The substrate taxes everyone — and the people who never opted in pay in goods, energy, wages, and attention.

This is the friction that closes the piece, because it is the one that converts the personal-scale “transition” of the prior pieces into a societal-scale reality. The principal class is being formed. The middle is being hollowed. The companies are forking. The pricing model is being rewritten. And the substrate is taxing everyone in the room — including the people who never read a piece like this one.

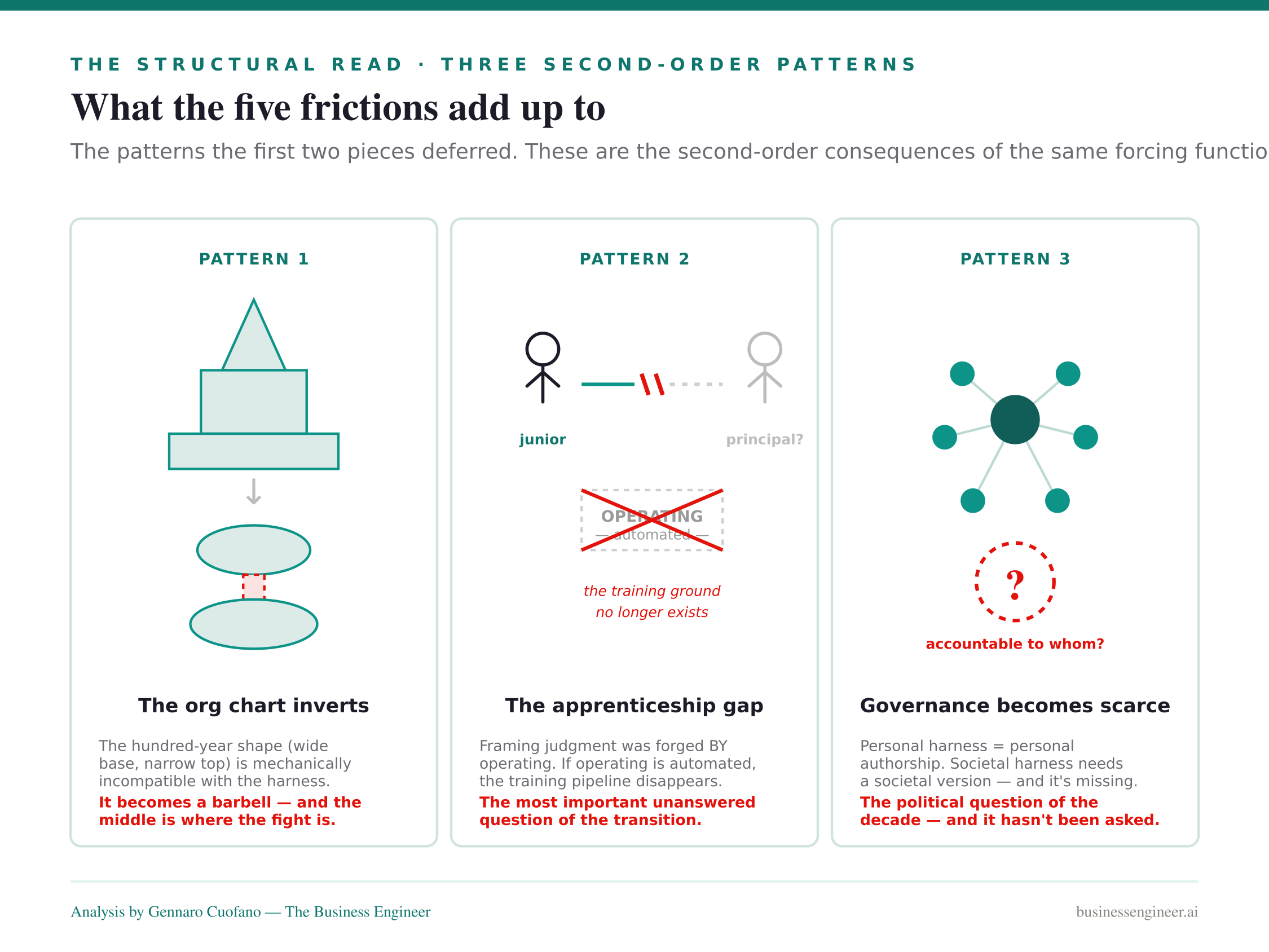

The structural read: three second-order patterns

Step back from the five frictions and three deeper patterns emerge — the second-order consequences the trilogy’s first two pieces deferred to here. Each is worth its own paragraph because each is a real, structural change to how the economy is organized.

The org chart inverts. The shape companies have used for the last hundred years — a wide base of operators, a layer of supervisors, a small top of decision-makers — is mechanically incompatible with the harness. The wide base is what gets automated. The supervisory middle is what gets dissolved. What is left is a small top of principals authoring outcomes and a thin pipeline of juniors apprenticing toward the top, with a swarm of agents in between doing the actual work that used to require the operating layer. Block is the shape running well. State Farm is the shape running badly. Most companies will spend the next five years trying to figure out which one they are, and the political fight over that decision will be the dominant internal story of the late 2020s. The companies that resolve it cleanly will become unrecognizable to their employees of three years prior. The companies that do not will fail in slow motion against competitors who did.

The apprenticeship pipeline breaks, and nobody is fixing it. Framing judgment was historically forged by operating. You became a principal by spending years as an operator, learning what the work actually is, accumulating the pattern recognition that lets you eventually direct it from above. If operating is being automated, the training ground for the next generation of principals quietly disappears. This is the genuine fragility in the harness thesis, and the data does not address it. Block’s BuilderBot is producing 15% of code, but where do the engineers who can direct a BuilderBot in 2030 come from, if there is nothing for them to operate in 2026? The answer right now is “from the existing pool of seniors, until that pool retires.” That is a transitional state with a hard expiration date. This is the most important unanswered question in the entire transition, and the people closest to the harness (myself included) have not yet articulated what replaces the operating-as-training-ground pipeline. Until someone does, the principal class is finite, ageing, and not being replenished.

Governance becomes the scarce resource. Personal harnesses are governed by personal authorship — the bedrock the first two pieces ended on. Societal harnesses need a societal version of the same thing, and it is genuinely missing. Who is allowed to be the principal of a swarm that can author at scale? Who is accountable when a swarm authors something that goes wrong — the operator, the lab, the regulator, the customer? Whose will and whose liability govern an agent that ran for fifty steps without supervision? These are political questions, not technical ones, and they are the ones that determine what the harness society actually feels like to live in. The labs and the hyperscalers will not answer them; they will optimize around whatever answer the rest of the system produces, the same way every other industry has done. The answer needs to come from somewhere else, and right now it is not coming from anywhere. That is the political vacuum the next decade fills. Whoever fills it — legislators, courts, professional associations, customer cartels, a new institution that does not yet exist — defines the terms of the harness society more than any line of code will.

The structural read

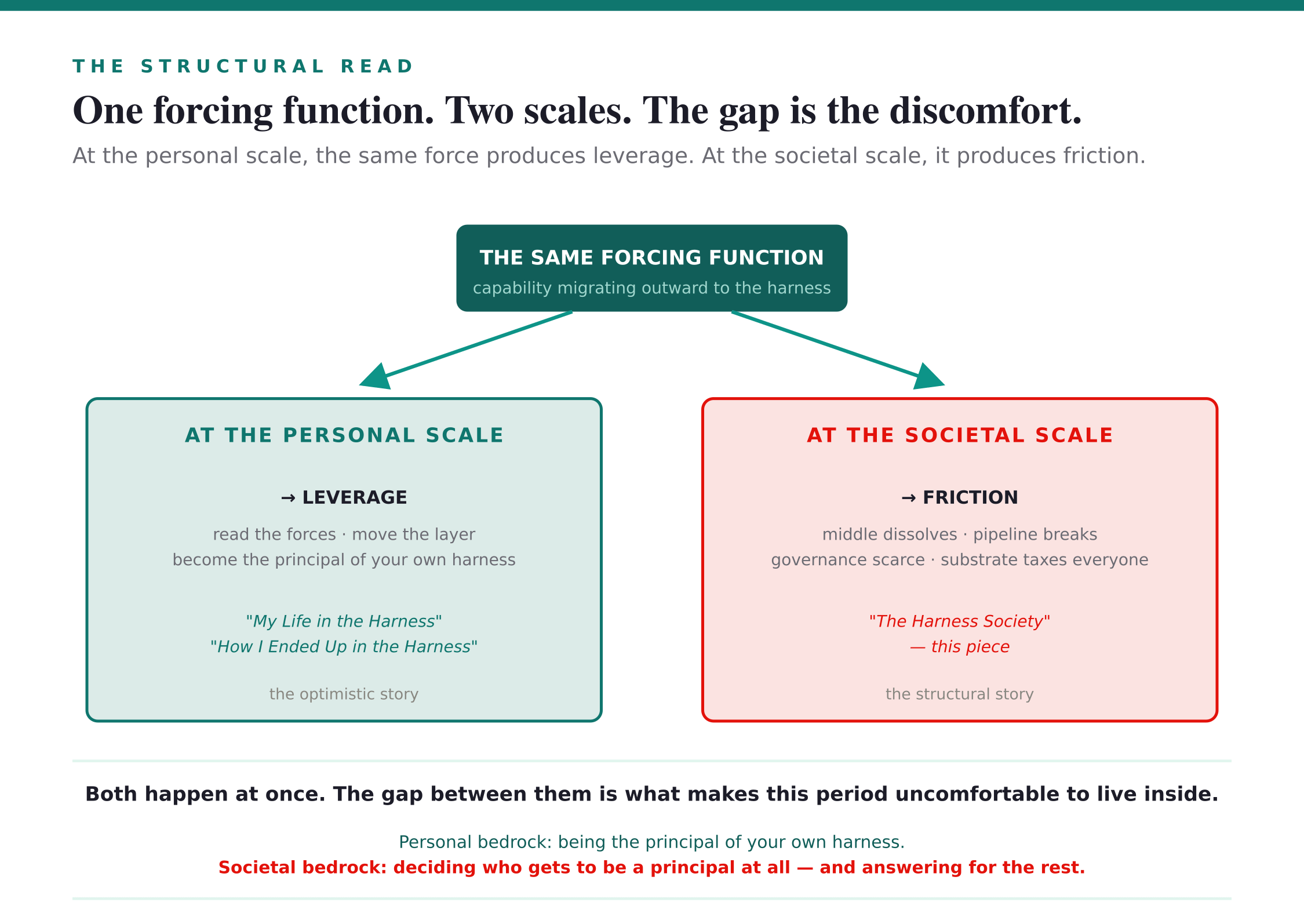

The harness society is not coming. It is here, and it is being born under pressure.

The personal version of the transition — the one I wrote about in the first two pieces — is real and available to people who can see the forces and move. It is the optimistic story, and the data supports it. Block-style amplifier orgs, Anthropic’s 70/30 planning split, Nadella’s human-capital framing, the AGaaS pricing transition where outcomes are well-defined — these are all the harness society going well.

But the same data set contains the structural story. State Farm’s 19,000 contracts. Gartner’s 1% / 87%. Gallup’s 3× — concentrated on the middle. Apple’s supply tax, generalized. The middle dissolves. The pipeline breaks. The substrate taxes the opt-outs. The new pricing model arrives bottlenecked on a problem most companies cannot solve. The political conversation has not begun.

These are not competing narratives. They are the same forcing function — capability migrating outward from the model to the harness around it — playing out at two scales simultaneously. At the scale of one person who can read the forces, it produces leverage. At the scale of a society that mostly cannot, it produces friction. Both are happening at once, and the gap between them is what makes this period feel uncomfortable to live inside.

The trilogy’s first two pieces ended on the bedrock — authorship, the position the churn cannot reach. That answer holds at the personal scale, and it holds here too, restated upward:

At the personal scale, the bedrock is being the principal of your own harness.

At the societal scale, the bedrock is deciding who gets to be a principal at all — and answering for the rest.

The first is a choice anyone reading this can make. The second is the political question of the next decade, and it has not been asked yet.

The harness society is here. The question is who runs it, and on what terms.

Key Takeaways & Mental Models

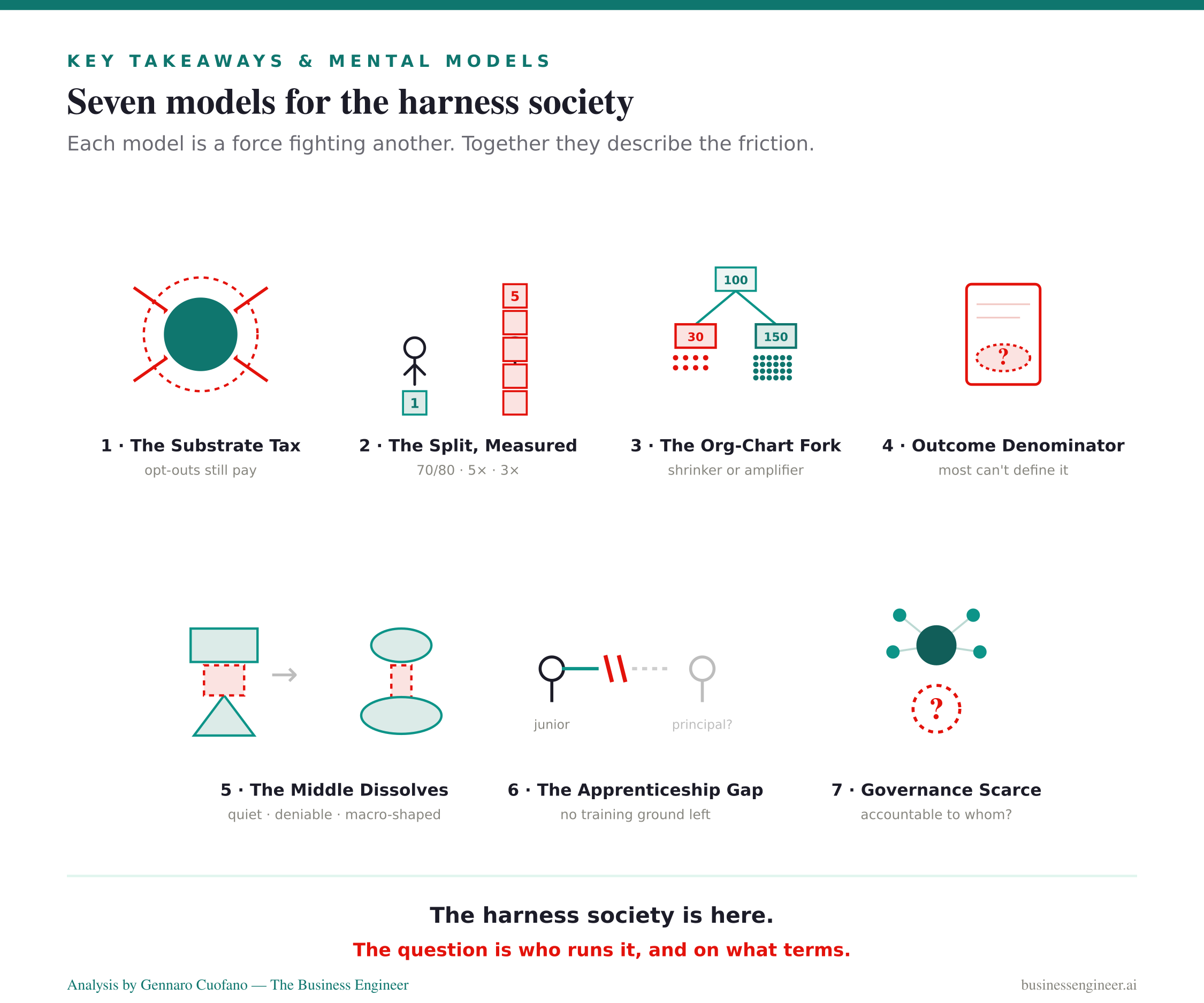

The Substrate Tax — AI is no longer one industry among many; it is a substrate the rest of the economy pays into whether or not it participates. Memory chips are the visible instance. Power grids, talent markets, capex, and political bandwidth are the next.

The Principal / Operator Split, Measured — Anthropic’s 70/80 planning-vs-execution split, the 5× expert-vs-novice output gap, and Gallup’s 3× layoff risk for non-adopters are the same fault line measured from three angles. The split is here, with receipts.

The Org-Chart Fork — Same AI, opposite results: 100 FTE → 30 FTE or 150 FTE. Shrinkers shrink. Amplifiers build. The technology multiplies whatever the company was already trying to be.

The Outcome Denominator — The hard part of the AGaaS transition is not pricing the task; it is defining the outcome. Most companies cannot articulate their outcomes at the granularity an agent contract requires. Solving this is an organizational restructure, not a procurement decision — and it is the load-bearing problem of the next three years.

The Middle Dissolves Quietly — AI is not firing juniors and not firing seniors. It is hollowing out the mid-level operating layer through the deniable mechanism of macro shocks, one cycle at a time. The political weight of that layer is the political weight of the median voter.

The Apprenticeship Gap — Framing judgment was forged by operating. If operating is automated, the training pipeline for the next generation of principals quietly disappears. Nobody is fixing this, and it is the most important unanswered question in the transition.

Governance as the Scarce Good — Personal harnesses run on personal authorship. Societal harnesses need a societal version of authorship: who is allowed to be the principal of a swarm, and who answers when one goes wrong. That is the political question of the decade, and it has not been asked.

Recap: In This Issue!

The Harness Society Is Not Optional

The central thesis is simple:

You do not get to opt out of the harness society.

Even people who never use AI directly are already paying for it through higher prices, constrained infrastructure, distorted labor markets, and redirected capital flows. AI is becoming a substrate, not an industry.

The Principal–Operator Split Has Become Measurable

For years, the idea that AI would separate people into those who direct intelligence and those who compete with it was largely theoretical.

Now the data is showing it:

Humans make ~70% of planning decisions.

AI performs ~80% of execution.

Experts generate 5× more output than novices using the same tools.

Non-adopters face roughly 3× higher layoff risk.

The emerging divide is not technical skill.

It is the ability to frame, direct, and evaluate work.

Companies Are Forking Into Two Models

AI is not producing one organizational outcome.

It is creating two.

The Amplifier

Similar headcount

Dramatically higher output

Humans orchestrate agent swarms

Example: Block

The Shrinker

Lower headcount

Cost-focused restructuring

AI used primarily for efficiency

Example: State Farm

The technology is neutral.

The strategic choice belongs to leadership.

The Outcome Economy Is Replacing the Seat Economy

The shift from SaaS to AGaaS changes the unit of value.

The old question:

How many users need access?

The new question:

What outcome is being delivered?

Most organizations cannot answer that question with precision.

This becomes the biggest bottleneck in AI adoption.

The companies that can clearly define outcomes unlock massive leverage.

The companies that cannot remain trapped in experimentation.

AI Is Quietly Hollowing Out the Middle

The most politically important insight:

AI is not primarily replacing juniors.

AI is not primarily replacing seniors.

AI is dissolving the middle.

The operating layer that historically sat between execution and leadership is becoming increasingly automated.

The result is a barbell structure:

Principals at the top

Apprentices at the bottom

A shrinking middle

This happens gradually, often hidden inside macroeconomic restructuring rather than explicit AI layoffs.

The Apprenticeship Crisis Has No Answer Yet

One of the deepest unresolved questions:

How do future principals emerge if operating work disappears?

Historically:

Operator → Experience → Judgment → Principal

If AI automates the operating layer, the traditional training ground for judgment disappears.

The industry has not yet solved this problem.

This may become the defining talent challenge of the next decade.

The AI Tax Is Becoming a Substrate Tax

AI is beginning to absorb scarce resources across the economy:

Memory chips

Electricity

Technical talent

Infrastructure capital

Political attention

This is what happens when a technology stops being a sector and becomes infrastructure.

Everyone pays the tax, including those who never participate directly.

Governance Becomes the Scarce Resource

The biggest unanswered question is no longer technical.

It is political.

Who gets to direct increasingly autonomous systems?

Who is accountable when they fail?

Who determines the rules under which agentic systems operate?

The next decade is likely to be defined less by breakthroughs in AI capability and more by the struggle to define legitimate authority over those capabilities.

The Core Insight

The first two Harness essays were about the transformation of the individual.

This piece expands the lens to society.

The underlying force remains the same:

Capability is migrating from the model into the harness around it.

At the individual level, that migration creates leverage.

At the organizational level, it creates restructuring.

At the societal level, it creates friction.

The harness society is not a future scenario. It is the operating environment that is already emerging around us.

With massive ♥️ Gennaro Cuofano, The Business Engineer