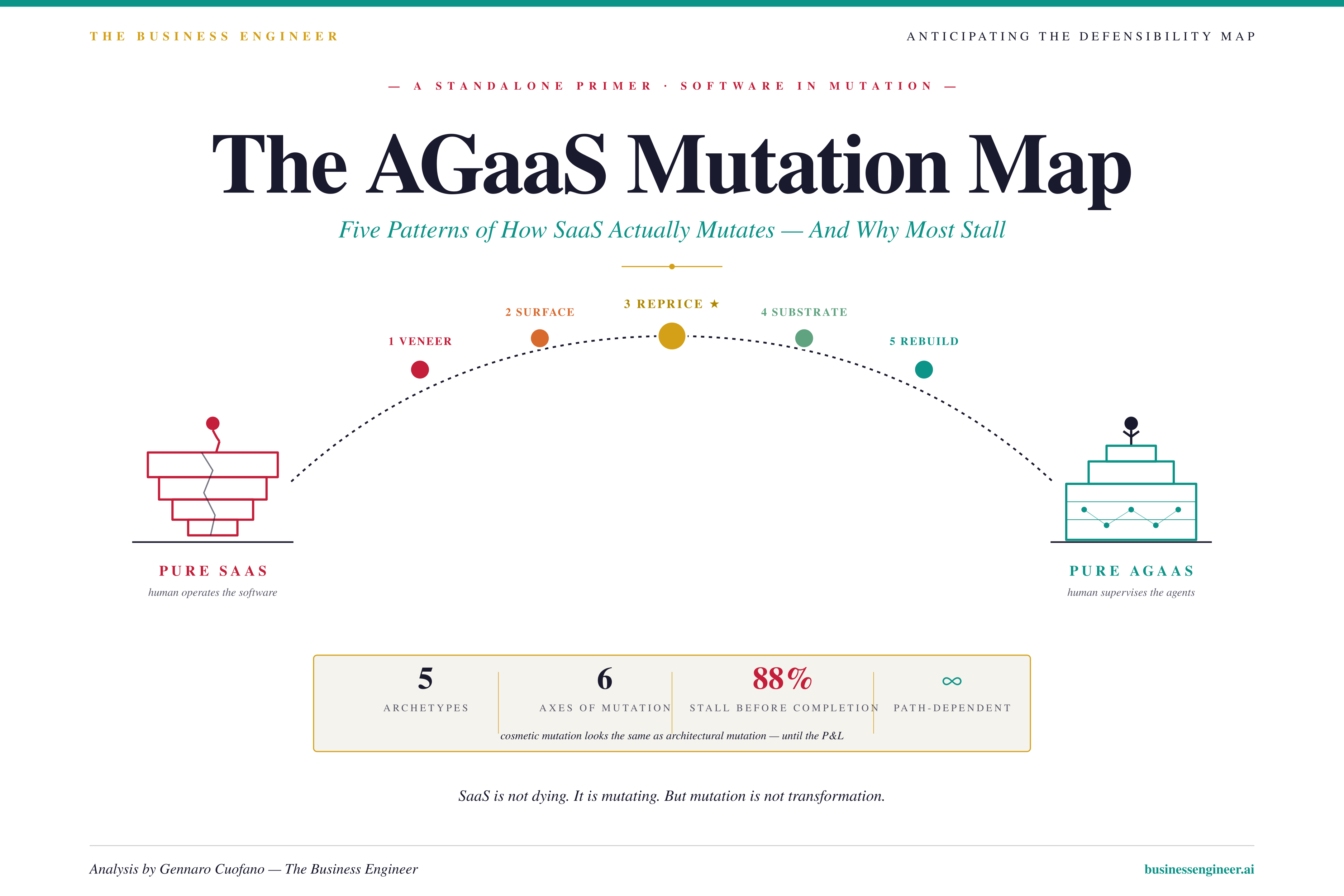

The SaaS to AGaaS Mutation

Back in March, I introduced you to the concept of AGaaS. Now it’s time to understand why every SaaS company is mutating into that.

What are the structural forces driving the change?

The dominant narrative in enterprise software in 2026 is that SaaS is dying.

This is not quite right.

SaaS is not dying. It is mutating.

But mutation is not transformation. A company can add “AI” to its name, ship a chatbot, expose an API, even introduce consumption pricing — and still be structurally the same company it was in 2022. The economics give it away. The org chart gives it away. The margin profile gives it away.

The interesting question is not whether a company is mutating — almost all of them are, in some direction, on some axis. The interesting question is how it is mutating, how completely, and whether the mutation will land.

This piece names the patterns. Five archetypes. A vocabulary for reading the next 24 months of enterprise software.

For Exec Members, The Full BE Agent Harness Is Now Available!

The Portal collapses seven assets I have built separately over the past decade into one substrate.

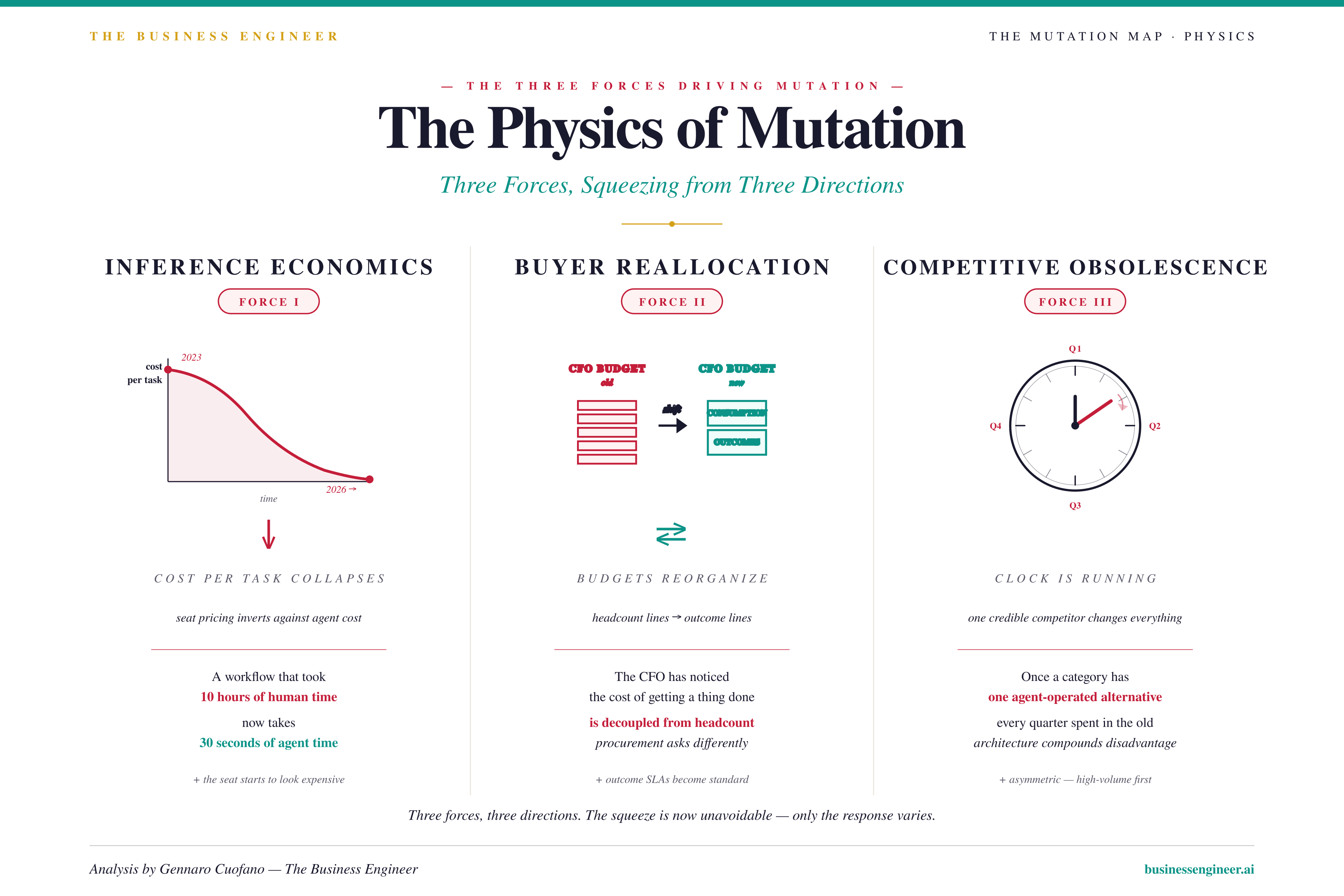

The Physics of Mutation

Mutations do not happen because companies want them. It happens because three forces are squeezing the SaaS architecture from three directions, and the squeeze is now unavoidable.

The first force is inference economics. As agent-led execution gets cheaper per task each year — orders of magnitude cheaper since the paradigm shift began — the unit economics of seat-priced software inverts. A seat that costs $50/month sat alongside a workflow that took 10 hours of human time; now the same workflow takes 30 seconds of agent time at a fraction of the cost. The seat looks expensive against the alternative.

The second force is buyer reallocation. Enterprise buyers are quietly reorganizing their budgets — from headcount and license lines to outcome and consumption lines. The CFO has noticed that the cost of getting a thing done is now decoupled from the number of humans involved. Procurement is starting to ask for outcome SLAs and unit pricing where it never did before.

The third force is competitive obsolescence. Once one credible competitor in a category ships an agent-operated alternative — priced on completions, callable by other agents, architected around outcomes — the rest of the category has a clock running. Every quarter spent in the old architecture is a quarter of compounding disadvantage.

These three forces do not arrive symmetrically. They hit some categories first (high-volume, low-judgment workflows) and others later (high-judgment, regulated workflows). But they hit. And the response to the hit — the pattern of mutation — is where the typology begins.

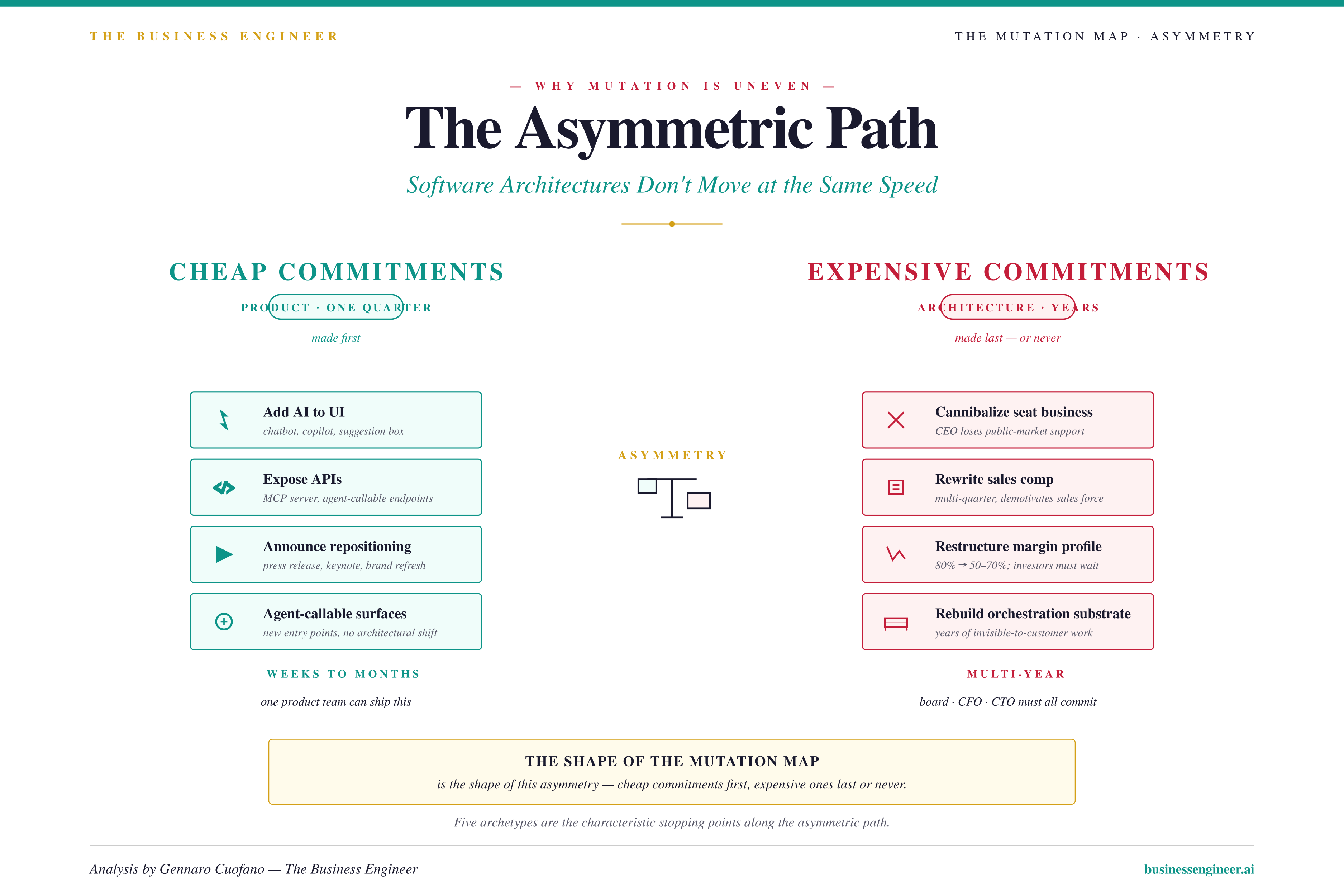

Why Mutation is Uneven

Software architectures are made of layers and commitments. Those layers do not all move at the same speed under pressure.

Some commitments are cheap to change. Adding an AI feature to the UI is a product decision; it takes a quarter and a few engineers. Exposing an API is a product decision too — slightly more work, but bounded. Adding a new agent-callable surface is a product decision.

Some commitments are expensive to change. Cannibalizing the seat business is a board decision that breaks the sales comp model, alarms public-market investors, and risks revenue in the quarter the change is announced. Restructuring the margin profile is a CFO decision that changes how the business is valued. Rebuilding the orchestration substrate is a CTO decision that takes years.

This asymmetry produces the entire shape of the mutation map. Companies make the cheap commitments first — and many never make the expensive ones. The result is a population of companies that have moved on the visible axes (UI, API, marketing) and stayed still on the hidden ones (pricing, margin, architecture).

The five archetypes are the characteristic stopping points along this asymmetric path.

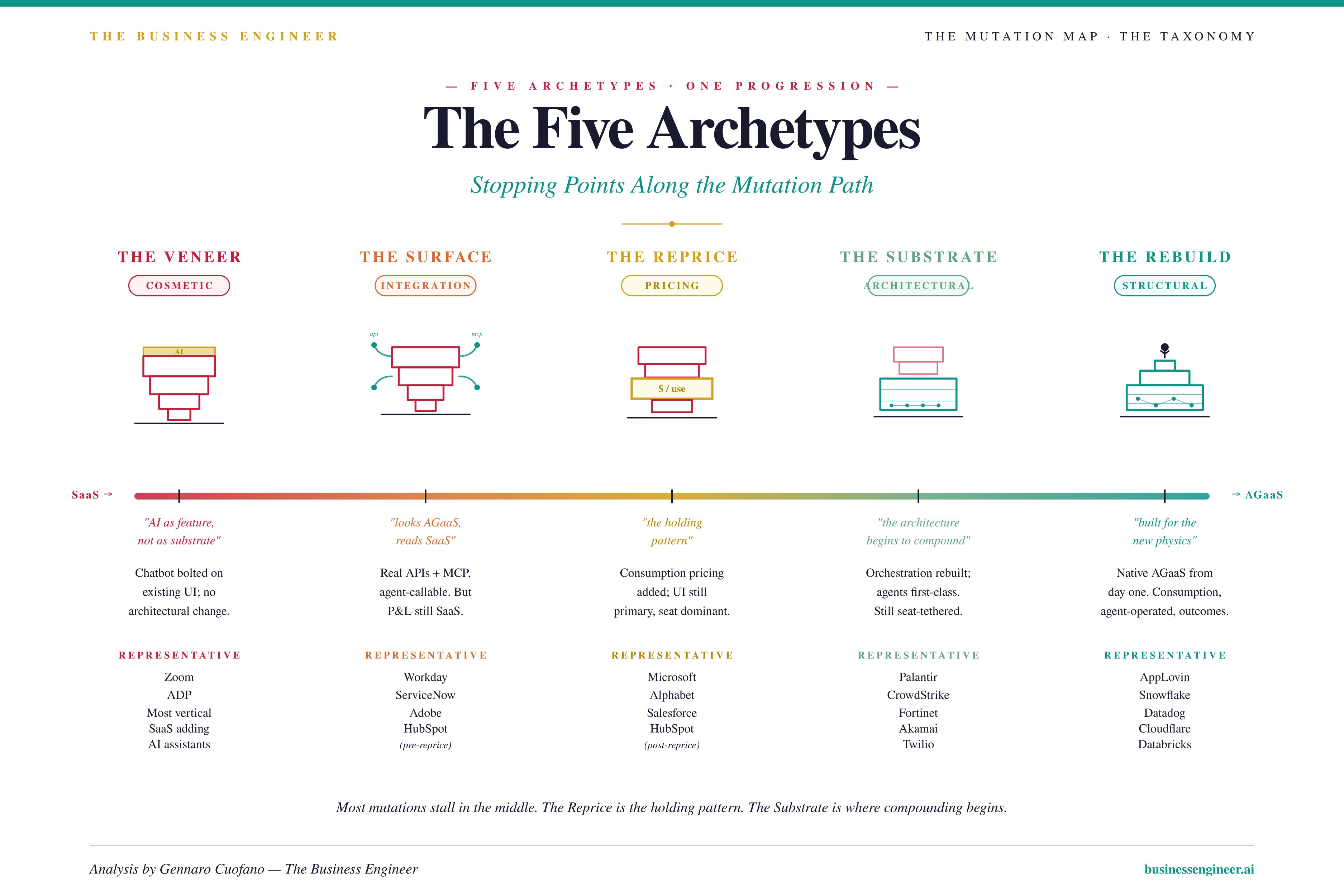

The Five Archetypes

THE VENEER

The cosmetic mutation. A chatbot bolted onto an existing UI. AI features in the changelog. Sometimes a press release announcing “the AI transformation of [legacy product].” None of it touches architecture, pricing, operator model, or margin.

The Veneer is the cheapest mutation. It is also the most common — and the most temporary. The cost curve eats it from underneath: as agent-led execution gets cheaper per task each year, a product whose only AI is a polite assistant on top of seat-priced workflows starts to look like a phone with an extra ringtone.

The Veneer is what a company ships when it wants to be seen mutating without committing to the mutation. It buys time. It does not buy defensibility.

Representative: most vertical SaaS adding AI assistants in 2025–26. Zoom. ADP.

THE SURFACE

The integration mutation. Real APIs. MCP endpoints. Agent-callable surfaces. The product becomes legible to the agent ecosystem — discoverable, addressable, callable.

But everything underneath stays SaaS:

The agent can call you, but you still bill per seat.

The agent can read your data, but the human still operates the workflow.

The agent can trigger an action, but the action is priced on the old curve.

This is the “looks AGaaS, reads SaaS” zone. To the outside ecosystem, the company is participating in the new paradigm. To the P&L, nothing has changed.

The Surface is genuine progress on two axes — value layer and access surface — but it leaves the harder axes untouched. It is a real commitment to interoperability. It is not yet a commitment to the new economics.

Representative: Workday. ServiceNow. Adobe. HubSpot before its repricing move.

THE REPRICE

The pricing mutation. Consumption tiers appear. Action-based billing emerges. Hybrid pricing structures (base + outcome) get introduced in enterprise contracts. Sometimes the change is real — Agentforce’s $2/action model is genuine consumption — and sometimes it is a re-bundled add-on.

This is the largest cluster in the universe. It is also the most ambiguous zone: a company in this state has committed publicly to the new paradigm but has not yet committed architecturally.

The UI is still primary.

The seat business still dominates revenue.

The board still uses seat-based ARR as the headline metric.

The new pricing is real, but small.

The Reprice is where most large enterprise software companies sit. The cluster is large because the move is rational: pricing change signals intent to the market, but does not require the painful structural commitments yet.

The Reprice is the holding pattern. It is where companies wait to see whether they can complete the mutation — or whether they will be acquired before they have to.

Representative: Microsoft. Alphabet. Salesforce. HubSpot (post-reprice).

THE SUBSTRATE

The architectural mutation. The orchestration layer gets rebuilt. Agents are first-class operators, not features. The data substrate is restructured for machine consumption. Outcomes start to be measurable and billable.

This is the zone where the mutation begins to compound. The architecture matches the marketing. The financial profile starts to shift — gross profit per customer grows, retention metrics behave differently than the seat business did, and a new kind of revenue line begins to appear in their earning calls.

But Substrate-state companies are often still tethered: they have a legacy seat business protecting near-term revenue, and the substrate is being built alongside it rather than replacing it. The mutation is real but not complete.

The Substrate companies are the ones to watch. They are the population from which the next paradigm’s incumbents will be drawn. The seat business may continue to throw off cash for years; the substrate is where the next decade’s compounding happens.

Representative: Palantir. CrowdStrike. Fortinet. Akamai. Twilio.

THE REBUILD

The structural mutation. Native AGaaS. Consumption-priced from day one. Agent-operated by design. Built for the new physics, not retrofitted into it.

These companies didn’t mutate. They were born after the shift — or built before the shift on the right substrate, by accident or insight. They are not “AI companies” in the marketing sense; they are companies whose entire architecture happens to match what the post-2026 frontier demands.

The Rebuild population is small. It is also disproportionately concentrated in the infrastructure and data layers — where consumption pricing and machine-callable access were the default long before “AGaaS” was a word. Application-layer Rebuilds are rare and tend to be newer companies built explicitly for the new paradigm.

Representative: AppLovin. Snowflake. Datadog. Cloudflare. MongoDB. Databricks.

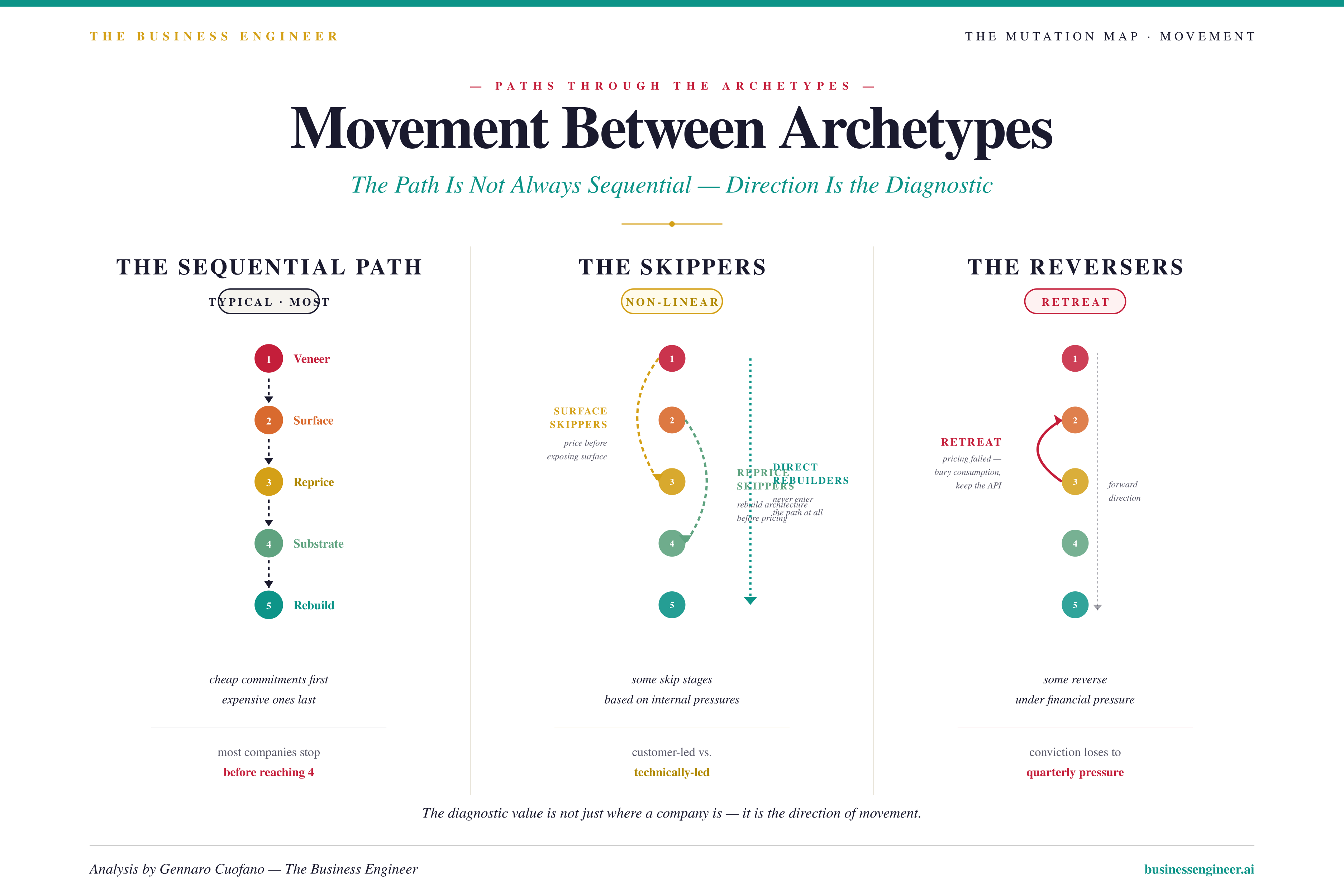

Movement Between Archetypes

The archetypes are stopping points on a continuum, not stable steady-states. Companies move between them — sometimes by design, sometimes by quarter-by-quarter pressure.

The typical path is sequential: Veneer → Surface → Reprice → Substrate → Rebuild. Companies start by adding cosmetic AI, then expose surfaces, then reprice, then rebuild architecture. Most stop before the end.

But not every company moves sequentially. Some skip:

Surface skippers go straight from Veneer to Reprice — they price differently before they expose surfaces. Common in enterprise sales-led companies whose customers demand consumption pricing.

Reprice skippers go from Surface to Substrate — they rebuild architecture before changing the price card. Common in technically-led companies that believe pricing follows architecture.

Direct Rebuilders never enter the path at all. They were built on the right substrate from the beginning.

And some companies reverse. A common reversal: a company moves into Reprice, fails to retain customers in the new model, and quietly retreats to Surface — keeping the API exposure but burying the consumption pricing. The mutation goes backward when financial pressure exceeds strategic conviction.

The diagnostic value of the typology is not just where a company is. It is the direction of movement.

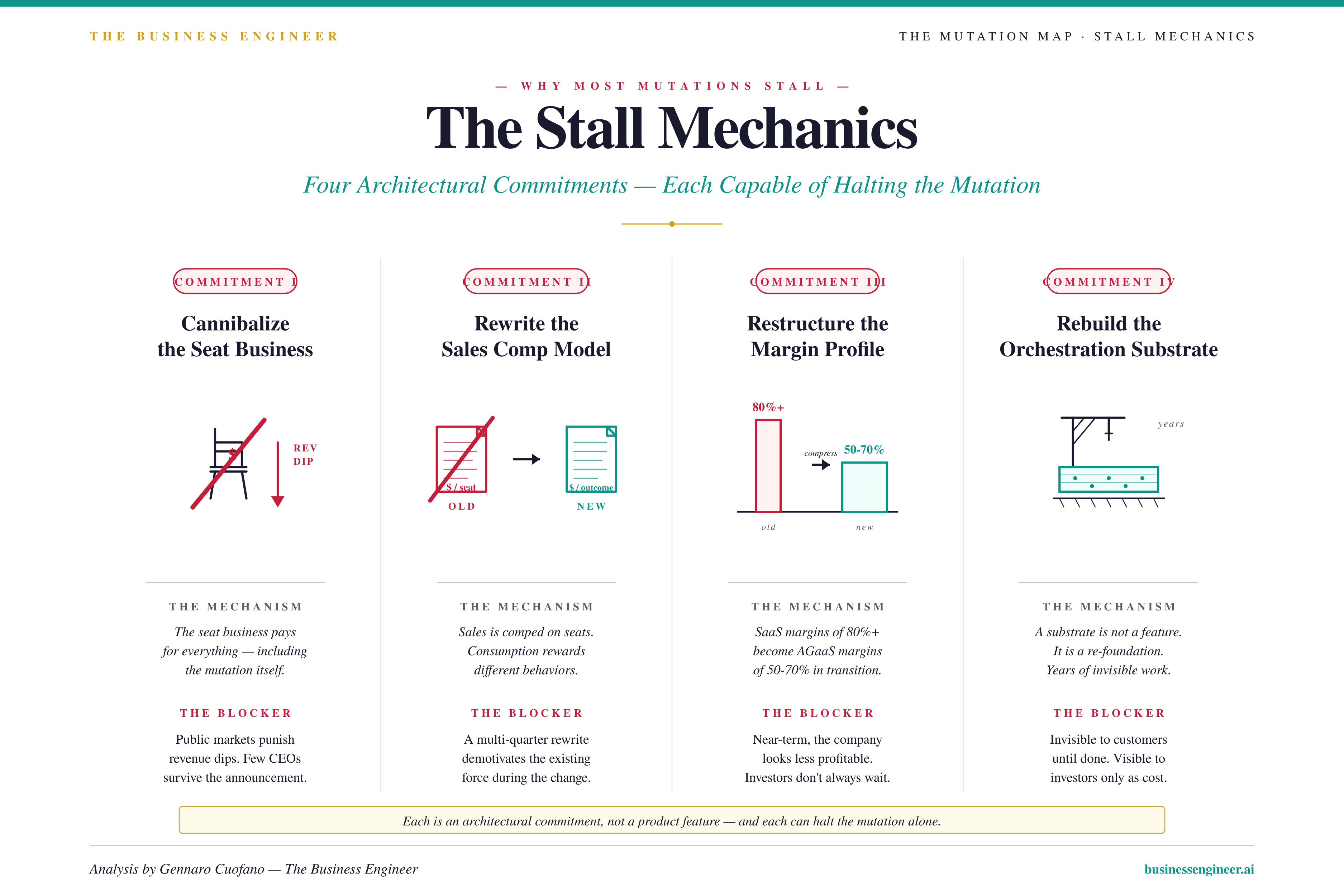

The Stall Mechanics

The mutation map reveals an uncomfortable distribution.

The vast majority of enterprise software companies sit at Surface or Reprice. Below the Substrate threshold. Above the Veneer floor. These are companies that have started the mutation but not completed it. They look transformed in product marketing. They read as legacy SaaS in financial structure. They are mid-architecture — between paradigms — and the gap between what they say and what they earn keeps widening.

Most will not complete the mutation. Not because leadership does not want to — but because completing it requires:

Cannibalizing the seat business. The seat business is paying for everything else, including the mutation itself. Cannibalizing it means accepting a revenue dip in a public-market environment that punishes revenue dips. Few CEOs survive the announcement.

Rewriting the sales comp model. The sales force is comped on seats. Consumption and outcome models reward different behaviors — and require different people. Rewriting comp at scale is a multi-quarter project that demotivates the existing sales force during the rewrite.

Restructuring the margin profile. Software margins of 80%+ get replaced by AGaaS margins of 50–70%. The new margins compound differently, but in the near term the company looks less profitable. Public investors do not always wait for the compound.

Rebuilding the orchestration substrate. This is the multi-year engineering commitment. The substrate is not a feature; it is a re-foundation. The work is invisible to customers until it is done, and visible to investors as cost.

Each of these is an architectural commitment, not a product feature. The reason most mutations stall is that the cheap commitments have already been made — and the expensive ones are the ones that finish the mutation.

The market is beginning to price this. Companies that have moved through the archetypes in recent quarters are getting rerated upward. Companies that have held flat are getting punished. The gap between what a company says it is and what it earns is becoming the most important number in ther earning calls.

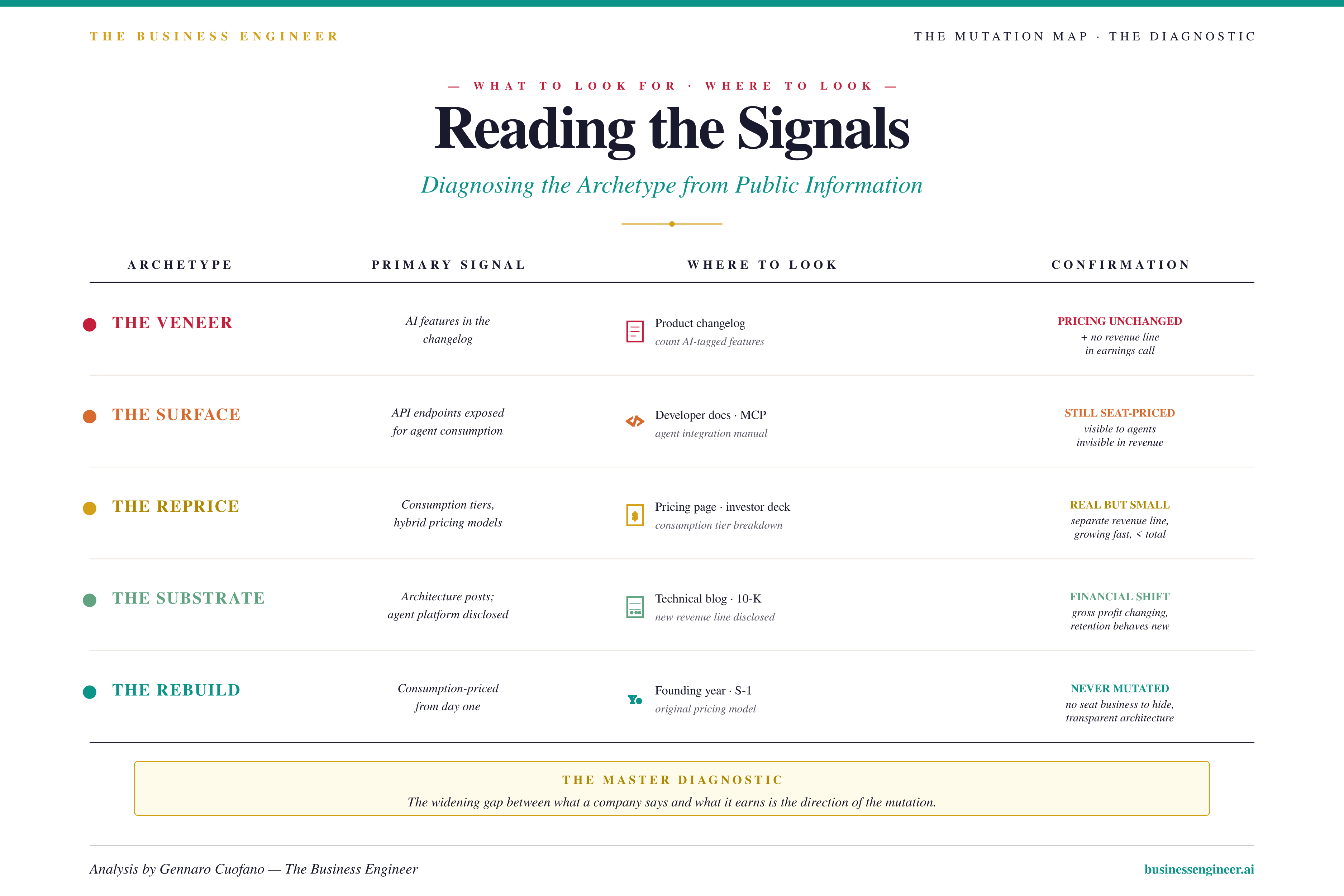

Reading The Signals

A typology is only useful if it can be applied. The archetypes can be diagnosed from public information — but the diagnostic requires looking in the right places.

For The Veneer, look in the product changelog. Count the AI-tagged features. Then check the pricing page: has anything changed? Check the earnings transcript: is AI mentioned only as a feature, not as a revenue line? If yes to changelog, no to pricing, no to revenue line — Veneer.

For The Surface, check the developer documentation. Are there API endpoints exposed for agent consumption? Is there an MCP server? Is there documentation for agent integration? Then check the pricing page: is access still seat-priced? Surface companies are visible to the agent ecosystem and invisible in the consumption metric.

For The Reprice, check the pricing page directly. Are there consumption tiers? Hybrid models? Outcome-based options? Then check the investor deck: how is consumption revenue reported? Is it a separate line, growing fast, but small? That is the Reprice signature: real new pricing, small total contribution.

For The Substrate, check the technical blog and architecture posts. Has the company published about its orchestration layer? Its agent platform? Its outcome measurement infrastructure? Check their earnings: is there a new revenue line large enough to disclose separately? Substrate companies are visibly rebuilding and visibly disclosing.

For The Rebuild, check the founding year and the original pricing model. Was the company consumption-priced from day one? Was the architecture machine-callable before “agent” was a marketing term? Rebuild companies are usually transparent about their architecture; they were never trying to hide a seat business that does not exist.

The most telling diagnostic is the gap between what a company says and what it earns. A company in Veneer or Surface that talks like Substrate is producing a widening gap. A company in Substrate that talks modestly is producing a narrowing gap. The direction of the gap is the direction of the mutation.

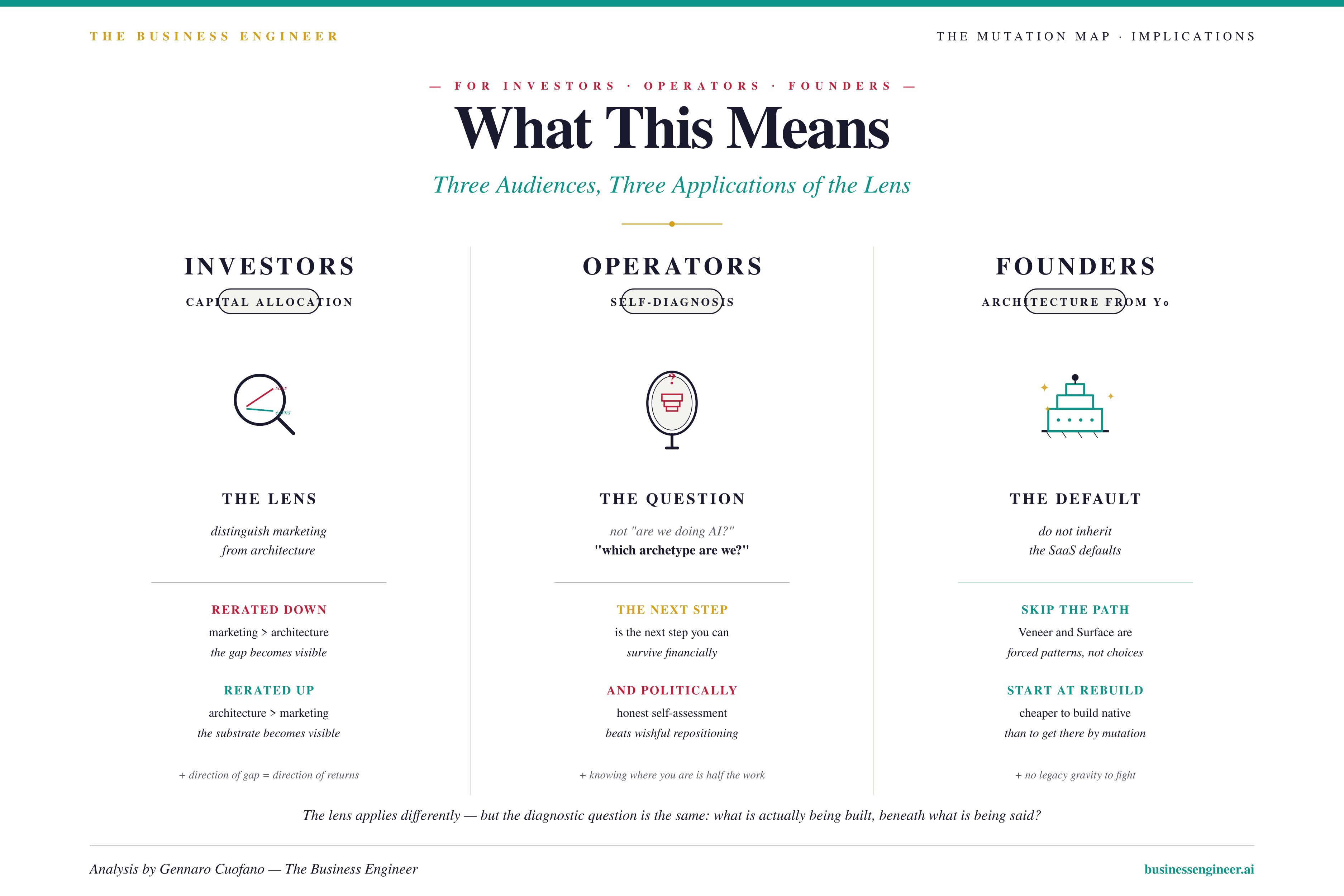

What This Means

For investors, the typology is a lens for distinguishing companies whose marketing has outrun their architecture from companies whose architecture has outrun their marketing. The first cluster will get rerated downward as the gap becomes visible. The second cluster will get rerated upward as the architecture becomes visible.

For operators, the typology is a diagnostic for honest self-assessment. The question is not “are we doing AI?” — every company is doing AI. The question is which archetype your company is actually in, and whether the next mutation step is one you can survive financially and politically.

For founders building new companies, the typology is a default to avoid. The Veneer and Surface archetypes are the patterns that legacy SaaS companies are forced into by their own architecture. A new company has no such constraint. Building toward Substrate or Rebuild from day one is structurally cheaper than getting there by mutation.

What’s Next

Mutation patterns are useful. They name what is happening.

But a typology is not a measurement. To know where a specific company actually sits — not just which archetype it resembles, but its exact position on the SaaS → AGaaS vector — requires a different lens. A scorecard. Six axes, each measured independently. A composite that distinguishes the company that marketed the mutation from the company that completed it.

That scorecard is called The Defensibility Map. It is the subject of the next piece in this series.

In the meantime: classify before you measure. Find the archetype before you find the score.

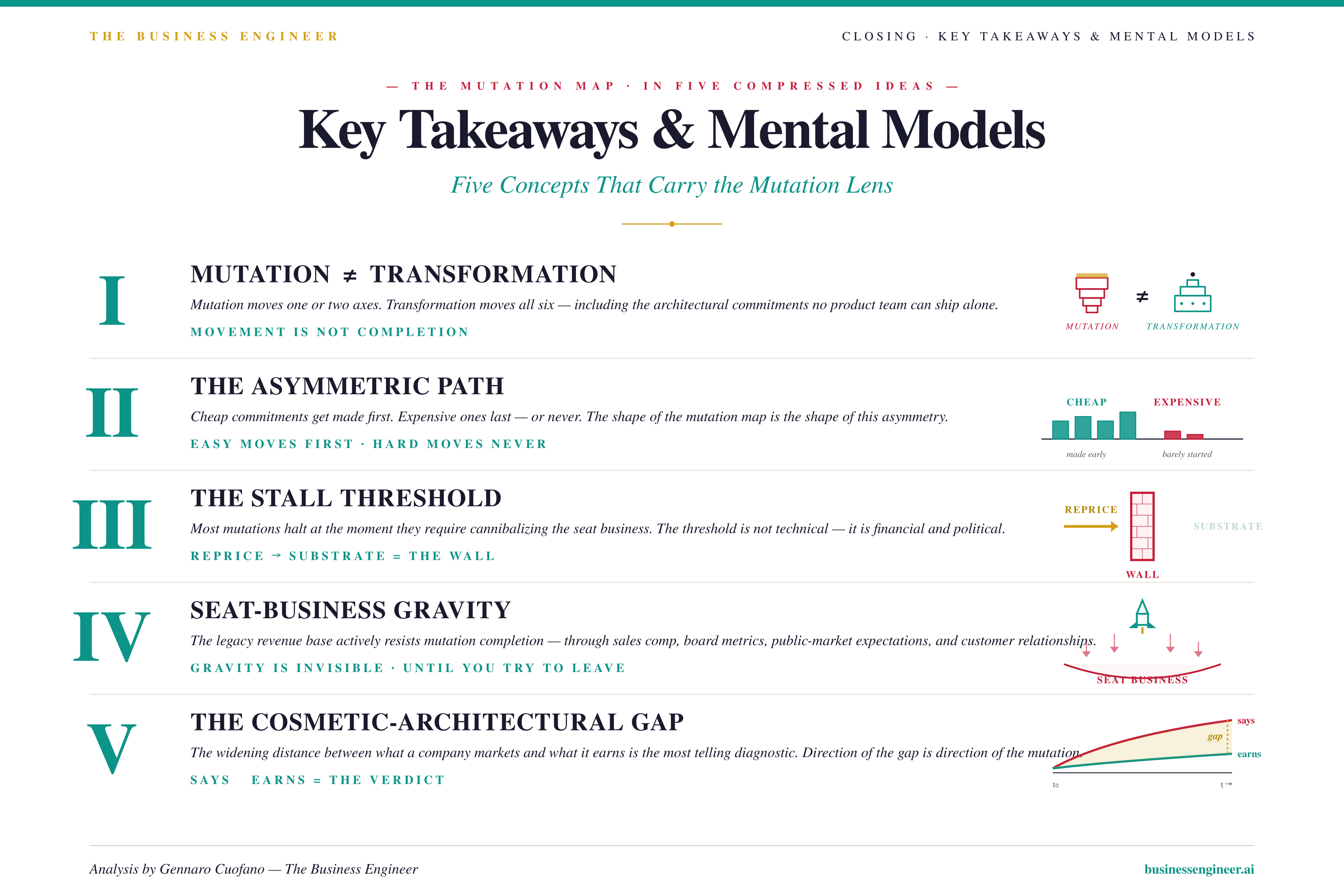

Key Mental Models

I — Mutation ≠ Transformation. Adding AI features, exposing APIs, and changing pricing are mutations on one or two axes. Transformation requires moving on all of them — including the architectural commitments that no product team can ship alone.

II — The Asymmetric Path. Cheap commitments (UI, API, marketing) get made first; expensive commitments (cannibalizing seat revenue, rebuilding the substrate) get made last or never. The shape of the mutation map is the shape of this asymmetry.

III — The Stall Threshold. Most mutations halt at the moment they require cannibalizing the seat business. The threshold is not technical; it is financial and political. It is the line between Reprice and Substrate.

IV — Seat-Business Gravity. The legacy revenue base actively resists mutation completion — through sales comp, board metrics, public-market expectations, and customer relationship structure. Gravity is invisible until you try to leave the surface.

V — The Cosmetic-Architectural Gap. The widening distance between what a company markets and what it earns is the most telling diagnostic of where it actually sits. Direction of the gap is direction of the mutation.

Recap: In This Issue!

The dominant claim that “SaaS is dying” is too simplistic. The stronger thesis: SaaS is mutating, but mutation is not the same as true transformation.

Most enterprise software companies are adding AI, APIs, agents, or consumption pricing, but many remain structurally SaaS underneath.

The real diagnostic is not whether a company has AI. It is where the mutation stops.

Three forces are driving mutation:

inference economics

buyer budget reallocation

competitive obsolescence

The core asymmetry: companies make cheap commitments first, such as AI features, APIs, and marketing. They delay expensive commitments, such as cannibalizing seat revenue, rebuilding architecture, and accepting lower margins.

The Five Mutation Archetypes

1. The Veneer

Cosmetic AI.

Chatbot added to existing UI

AI features in the changelog

No pricing change

No architecture change

No operator-model change

Representative examples:

vertical SaaS adding AI assistants

Zoom

ADP

Key point:

The Veneer buys narrative time, not defensibility.

2. The Surface

Integration-level mutation.

APIs exposed

MCP endpoints added

Product becomes agent-callable

But pricing and workflows remain SaaS-like

Representative examples:

Workday

ServiceNow

Adobe

HubSpot before repricing

Key point:

The company looks AGaaS externally but still reads SaaS financially.

3. The Reprice

Pricing-level mutation.

Consumption tiers introduced

Hybrid pricing appears

Outcome/action-based pricing begins

But legacy seat revenue still dominates

Representative examples:

Microsoft

Alphabet

Salesforce

HubSpot post-reprice

Key point:

This is the holding pattern for most large enterprise software companies.

4. The Substrate

Architectural mutation.

Agents become first-class operators

Orchestration layer is rebuilt

Data substrate becomes machine-consumable

Outcomes become measurable and billable

Representative examples:

Palantir

CrowdStrike

Fortinet

Akamai

Twilio

Key point:

This is where mutation starts compounding.

5. The Rebuild

Native AGaaS.

Consumption-priced from day one

Agent-operated by design

Machine-callable architecture

Built for the new economics, not retrofitted into them

Representative examples:

AppLovin

Snowflake

Datadog

Cloudflare

MongoDB

Databricks

Key point:

These companies did not mutate. They were already architecturally aligned with the new paradigm.

Core Strategic Insight

The mutation path usually follows:

Veneer → Surface → Reprice → Substrate → Rebuild

But most companies stall before Substrate.

Why?

Because moving beyond Reprice requires:

cannibalizing seat revenue

rewriting sales compensation

accepting lower AGaaS margins

rebuilding the orchestration substrate

This is not a product challenge. It is a financial, political, and architectural challenge.

The Main Diagnostic

The most important signal is the gap between: what the company says it is and what the company earns from

A company talking like Substrate but earning like SaaS is still trapped in mutation theater.

Key Mental Models

Mutation ≠ Transformation

AI features and APIs are not enough. Transformation requires pricing, margin, operator, and architecture migration.The Asymmetric Path

Visible changes happen first. Structural changes happen last, or never.The Stall Threshold

Most companies stall when migration requires cannibalizing seat revenue.Seat-Business Gravity

Legacy ARR, sales comp, board metrics, and public-market expectations pull companies back toward SaaS.The Cosmetic-Architectural Gap

The wider the gap between AI narrative and financial structure, the weaker the mutation.

Bottom Line

SaaS is not dying in a clean, linear way. It is splitting into mutation archetypes.

The winners are not the companies that “add AI.”

They are the companies that move from surface-level mutation into architectural substrate transformation.

With massive ♥️ Gennaro Cuofano, The Business Engineer