The Six AGaaS Moats

Every business model transition redefines what defensibility means. SaaS had its own moat vocabulary — seat lock-in, network effects, switching costs on stored data, ecosystem depth. Those moats worked because SaaS sold access to tools that humans operate, and defensibility grew around human usage patterns.

AGaaS breaks that vocabulary because AGaaS sells something structurally different. AGaaS — Agentic-as-a-Service — charges for the execution of outcomes by agents, not for access to tools operated by humans.

The AGaaS Race

Back in March, I introduced you to the concept of AGaaS. Now it’s time to understand what makes it so.

That single reframing is the disruption. It rewires what gets sold (outcomes, not access), who does the buying (business budgets, not IT budgets), where margin lives (substrate, not interface), and which metrics still predict the future (consumption, not seats). Every SaaS moat was built for a world where the seat was the atomic billing unit. In AGaaS, the seat is gone. The agent is the atomic unit, and the moats have to be rebuilt from scratch around it.

Three sequential inversions define the transition, and understanding them is prerequisite to understanding what defensibility looks like inside the shift:

The operator inversion. The agent, not the human, operates the workflow. The billing unit stops tracking headcount and starts tracking agent activity. Most enterprise software companies have completed this inversion architecturally by mid-2026, even if they have not repriced.

The buyer inversion. The person authorizing the purchase is the executive who owns the outcome (the CRO, the COO, the general counsel), not the IT function that owns the tool stack. Procurement, budget line-items, and the sales motion all rearrange. Most vendors are still mid-flight on this one.

The margin inversion. Gross margin structure shifts from “software plus support” (high fixed margin, low variable cost) to “consumption minus inference” (variable margin dominated by token cost). The P&L reshapes. This inversion is deferred at most incumbents through mechanisms like internal absorption (”Customer Zero”), buybacks, and reclassification, but it becomes visible once consumption revenue scales past a threshold.

The AGaaS transition is what these three inversions look like when they run through the enterprise software category. It has a canonical form, and its canonical form has been mapped in the prior work of this analytical arc:

Follow me on The AI Supercycle as well!

“From SaaS to AGaaS: The Full Cascade” (March 2026) mapped the underlying value-layer inversion — value migrating from the interface layer, where SaaS captured it, down to the substrate layer, where AGaaS captures it — and the five-layer cascade this inversion produces across the enterprise software stack. It also established the three canonical AGaaS pricing models: outcome-based, consumption-based, and hybrid.

“The Four Frictions of AGaaS” (April 2026) mapped the frictions that slow the transition — financial, operational, competitive, commercial — and why they multiply rather than add.

“The Tell: Salesforce Q1 FY27” (May 2026) used the largest pure enterprise-software incumbent as an instrument to locate where the transition actually sits. The verdict: architecturally migrating, mechanically still SaaS. Operator inverted, buyer not, margin deferred.

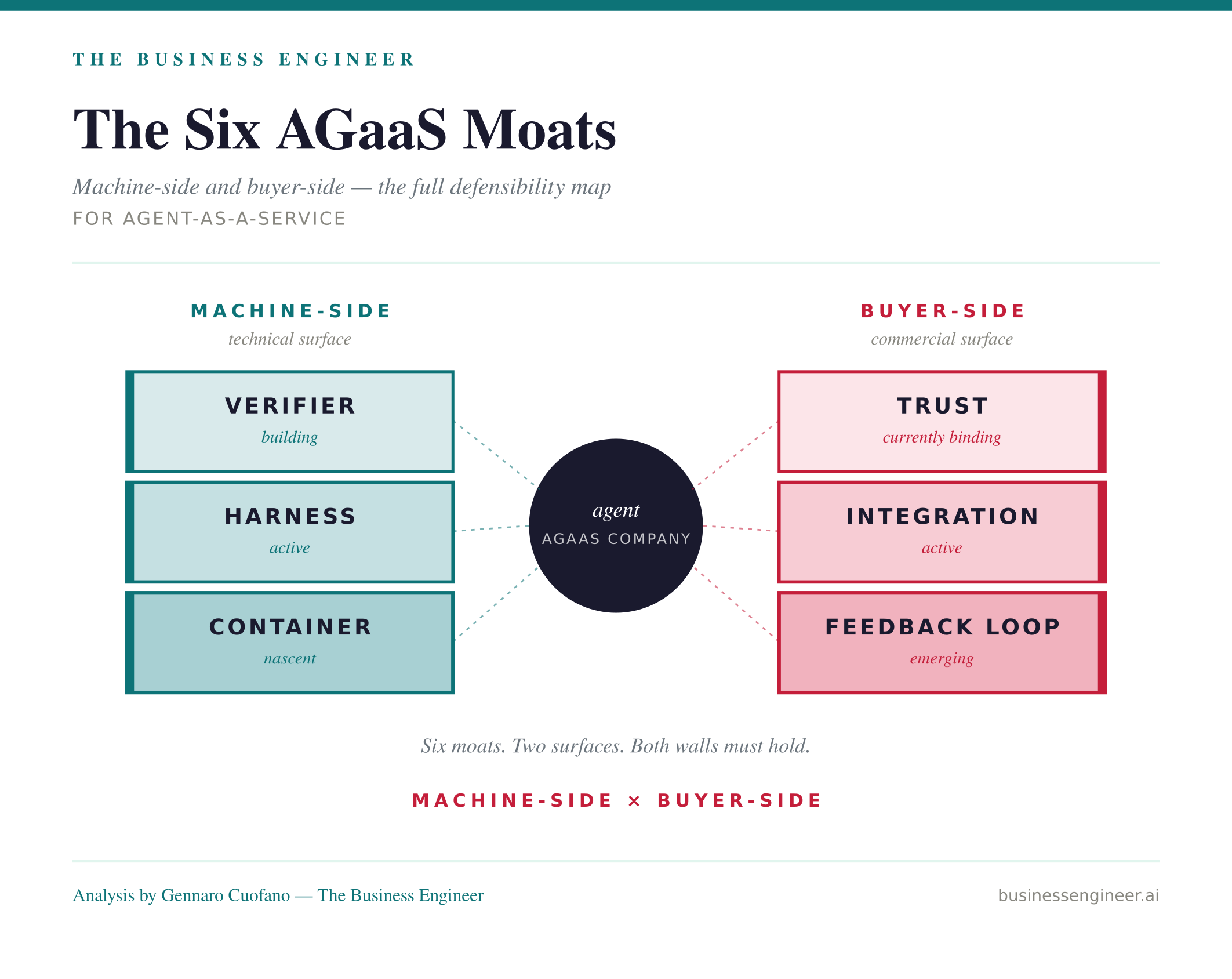

“The Four Intelligence Moats” (June 2026) — the direct parent to this piece — mapped how the entire AI stack builds defensibility across paradigms: corpus, verifier, harness, container. That piece established the machine-side moat map.

This piece completes the arc by mapping defensibility inside the transition itself. If old SaaS moats no longer apply and machine-side moats alone are not sufficient, what moats does an AGaaS company actually build? The answer is six — three inherited from the machine-side (verifier, harness, container), three new to the buyer relationship (trust, integration, feedback). Together they define what AGaaS defensibility looks like once the transition matures. They also determine, mechanically, which of the three AGaaS pricing models a company can actually charge — a link the closing section of this piece will make explicit.

The order in which the six moats are built matters more than the number of them. They are not parallel. They are serial. Each one unlocks the next. A company that tries to build them out of order finds itself with moats that do not compound — and, more consequentially, with pricing power that stalls at whichever inversion its missing moat was gating.