The State of AI Compute

Premium Analysis

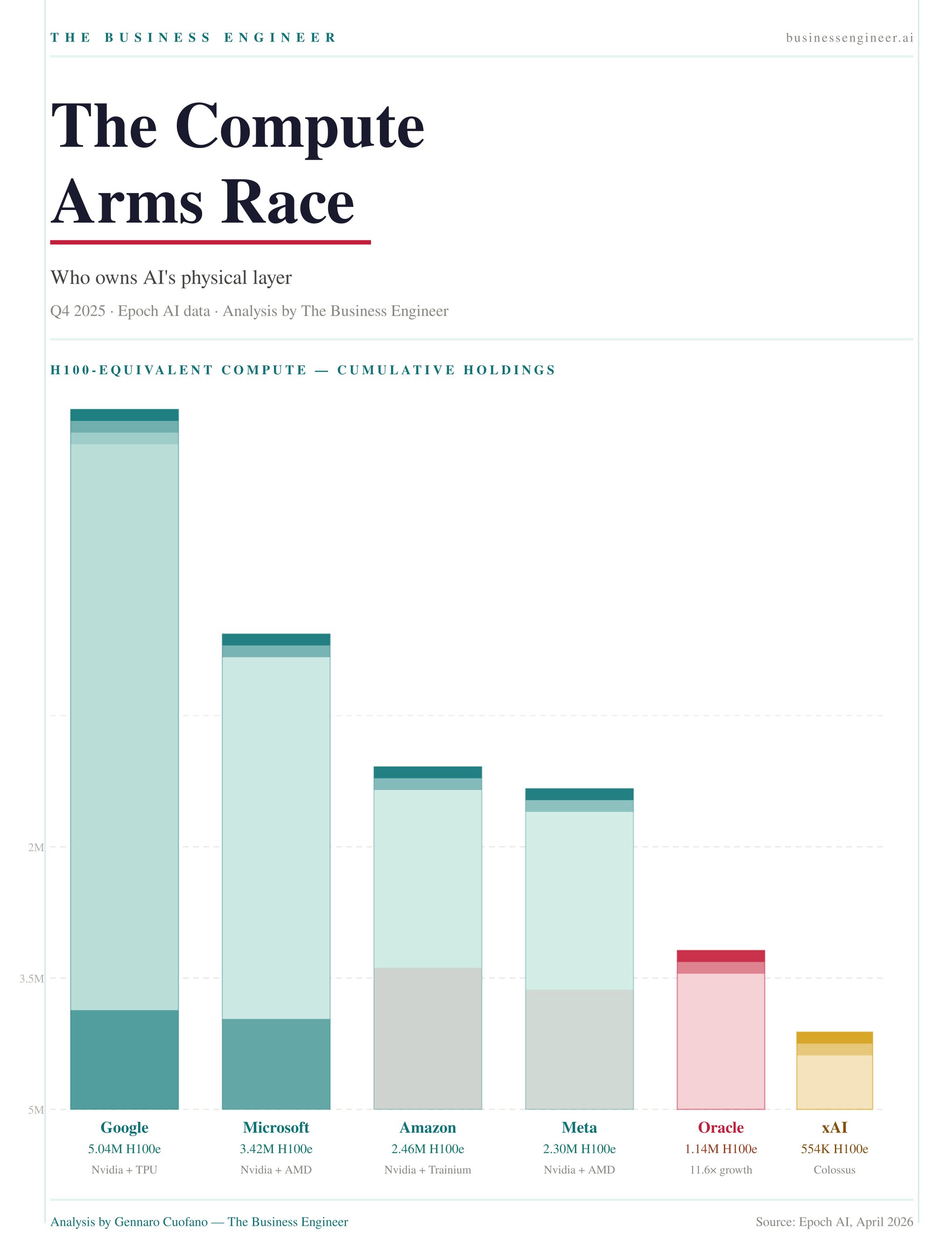

There is a number that keeps doubling, and nobody outside a handful of data centers fully appreciates what it means.

In Q1 2024, the total tracked AI compute capacity across the world’s major technology players stood at roughly 2.5 million H100-equivalent units. By Q4 2025 — eight quarters later — it had reached 21.3 million. An 8.5× expansion. Not 8.5% growth. Not 85%. Eight and a half times.

This is not a build. It is a structural transformation of who controls the physical substrate of the next economy. And the patterns visible in that data — who is building, at what pace, with whose chips, toward what architecture — reveal something deeper than a hardware procurement story. They reveal the strategic intentions of the five or six organizations that are quietly competing to own the AI infrastructure layer for the next decade.