AI & The Dynamo Doctrine

It’s easy to lose sight of where we are in the AI Supercycle.

The AI Supercycle

Back in 2022, I introduced my first analogy for what I believed would become the defining shape of the AI revolution.

In that regard, Jensen Huang’s ability to zoom out, connect the dots, and articulate the broader transformation underway is truly exceptional.

I highly recommend watching the talk below, along with the accompanying article it inspired.

The piece builds on Huang’s perspective while incorporating several frameworks and mental models I’ve been developing to better understand and navigate the AI Supercycle.

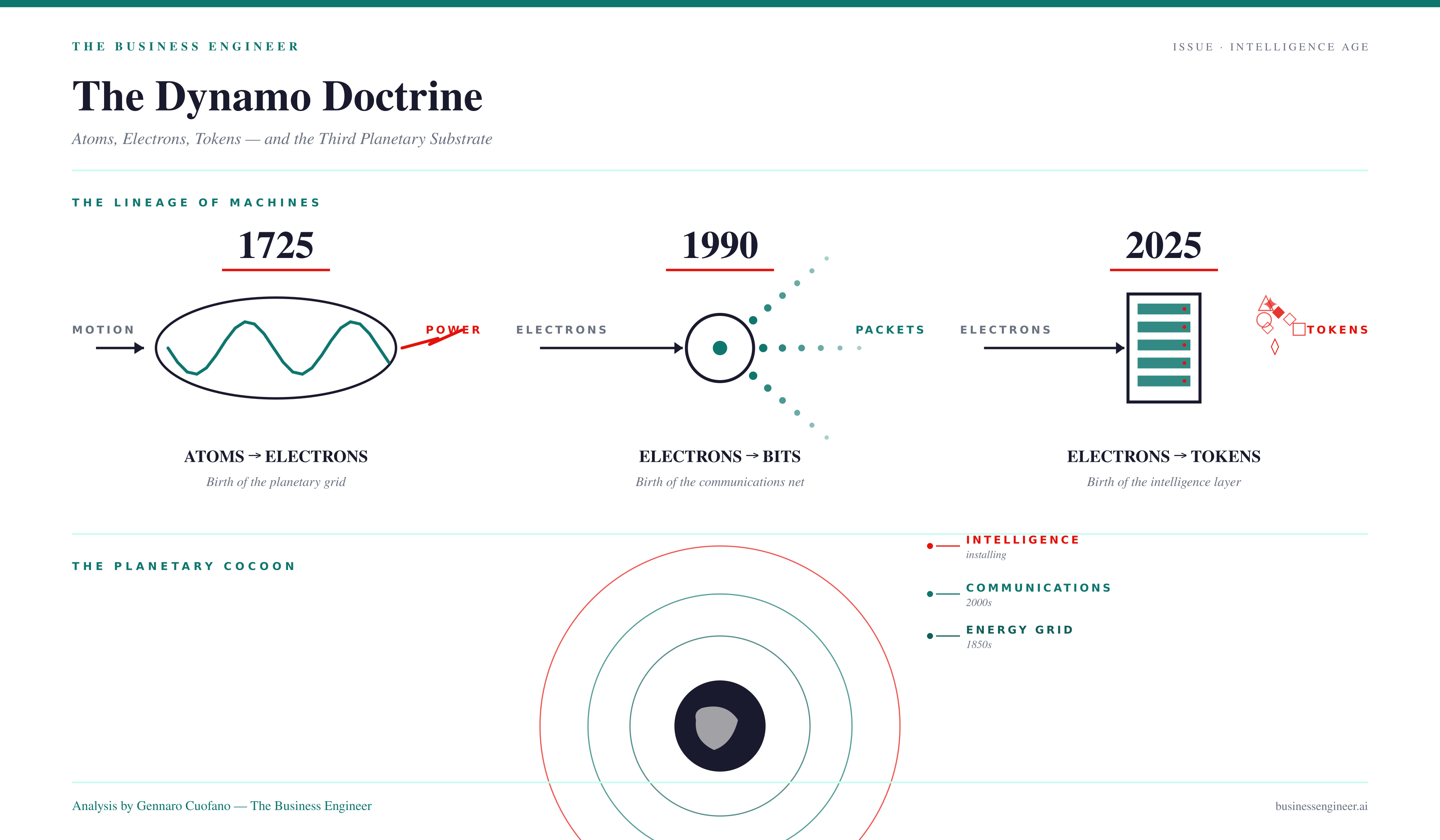

Every industrial age is defined by a machine that consumes one substrate and emits another. The substrate that gets emitted — not the machine that emits it — is what reshapes the economy. Three hundred years of industrial history compress into three of these conversions, and the third one is being installed in real time, in concrete and copper, on every continent simultaneously.

The machine is the dynamo. The substrate is intelligence. The cocoon is forming now.

The Substrate Doctrine — Atoms, Electrons, Tokens

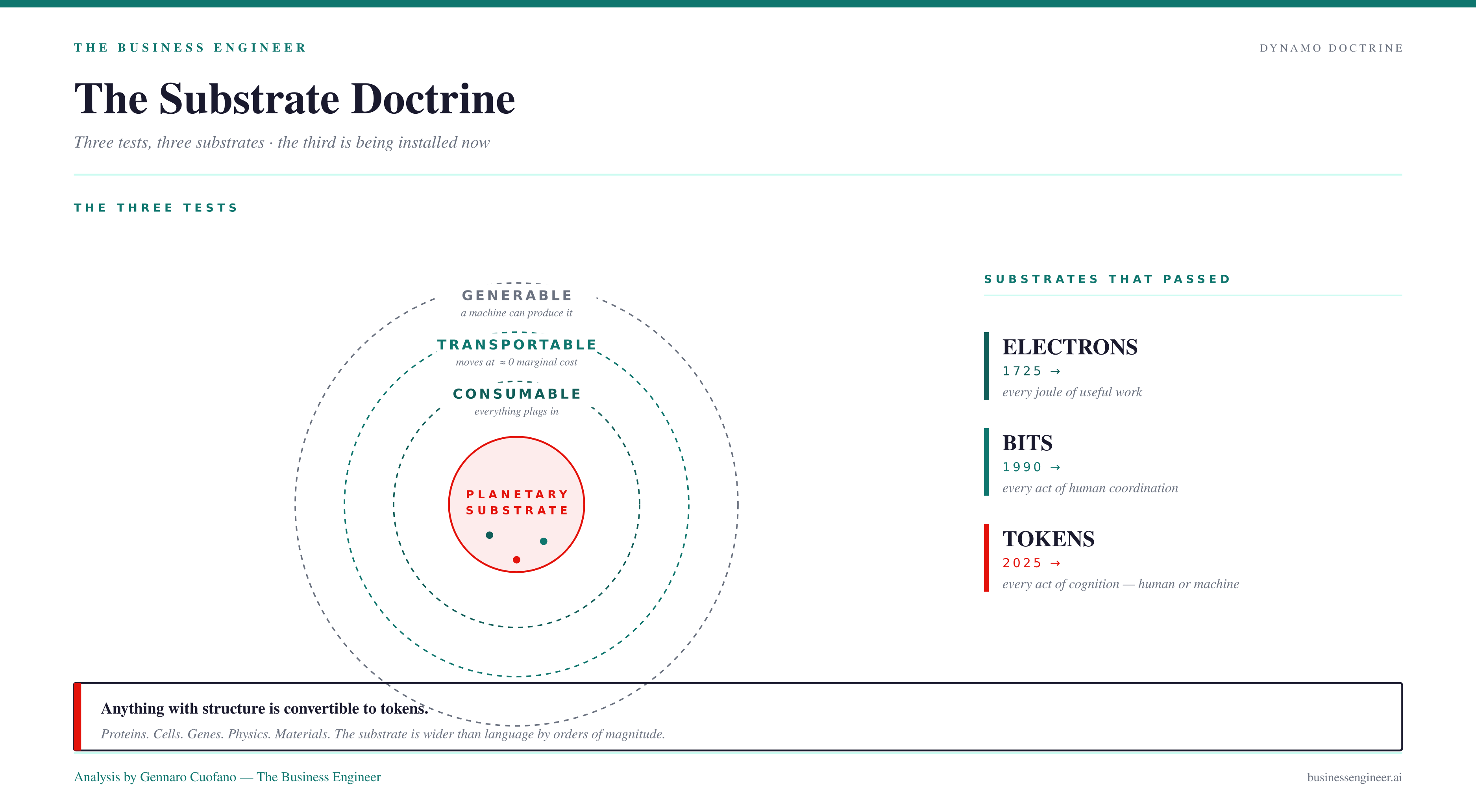

A substrate becomes infrastructure when three conditions hold. It must be generable on demand (a machine can produce it). It must be transportable at near-zero marginal cost (a wire, a fiber, a rack). It must be universally consumable (everything plugs in). Three substrates have ever passed all three tests at planetary scale.

Electrons. A coil rotated through a magnetic field emits an invisible force. Within a century, that force cocoons every continent in a grid. Total addressable market: every joule of useful work humanity wants done.

Bits. Electrons routed through switches at near-luminal speed emit packets. Within three decades, those packets cocoon the planet in a network. Total addressable market: every act of human coordination.

Tokens. Electrons fed into massively parallel arithmetic emit numbers that encode meaning — text, code, images, video, protein structures, control signals, decisions. The substrate is intelligence. The economy is reorganizing for the third time. Total addressable market: every act of cognition humanity wants performed, plus the cognition of the machines themselves.

The implication of the lineage is not that AI is “like” electricity. The implication is that AI is on the same curve as electricity — same generational capital requirements, same regulatory eventualities, same commodity endpoint, same hundred-year reorganization of everything downstream. We are not in the chatbot phase. We are in the dynamo phase. The chatbot is one light bulb.

A second, deeper claim sits underneath the lineage: anything with structure is convertible to tokens. Proteins fold predictably. Cells behave predictably. Genes express predictably. Physics is predictable. Materials are predictable. The token is therefore not just a unit of language — it is the universal carrier of any learnable structure in the universe. The substrate is wider than language by orders of magnitude.

The Primitive Inversion — From Retrieval to Generation

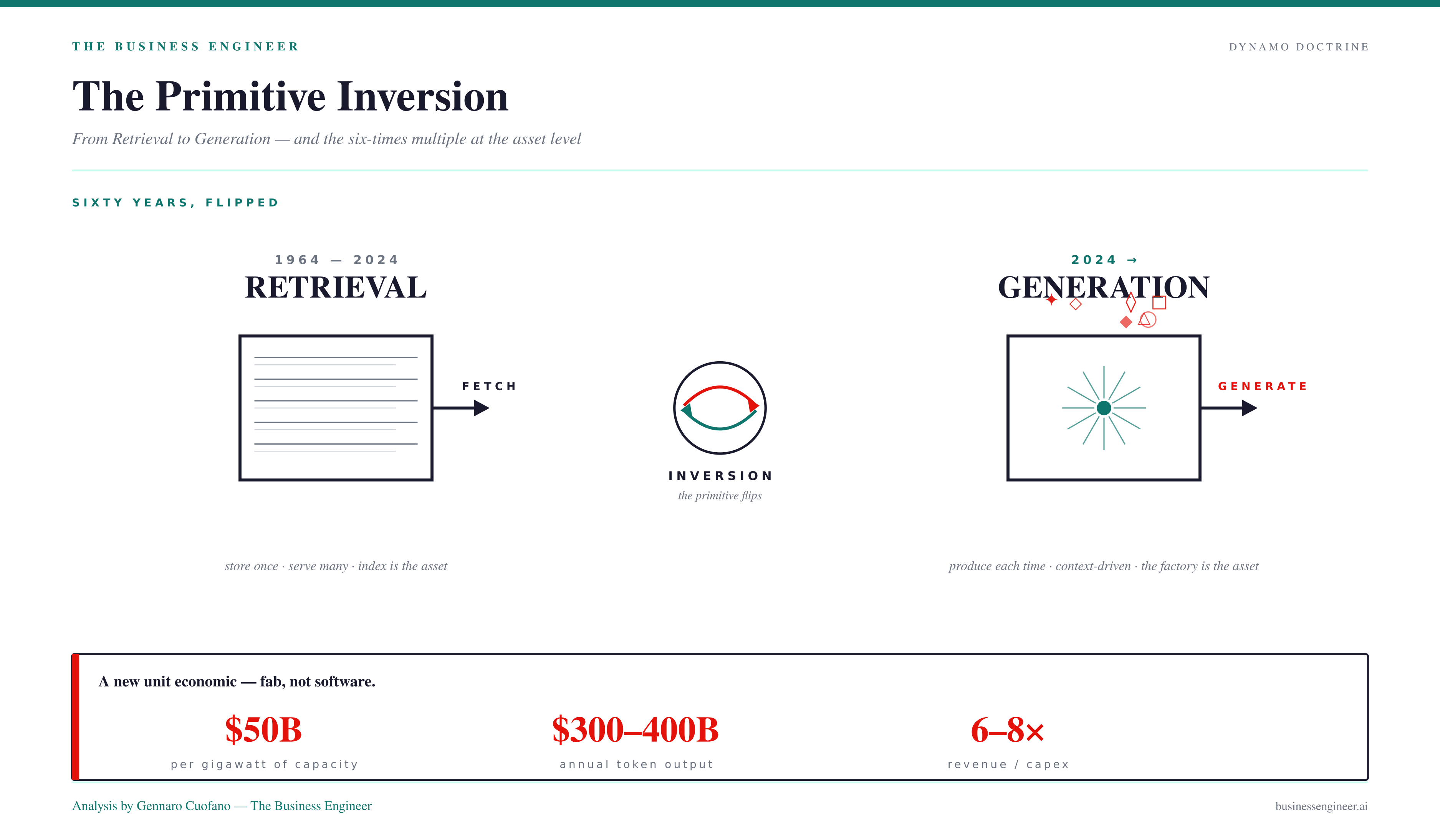

For sixty years, computing was a retrieval architecture. You wrote, you stored, you fetched. Every screen ever looked at served something pre-recorded by someone, somewhere, earlier. The most valuable real estate of the prior internet was the index — the catalog of what had already been made.

That primitive has inverted. Output is now produced originally, in real time, contextually, for one consumer, once. Every pixel, every word, every frame, every recommendation — generated, not retrieved. This is not a refinement of the old computing. It is a different machine emitting a different substrate. Hence the rename: data centers do not produce intelligence; AI factories do.

The unit economics of an AI factory are unlike anything in software history. One rack carries seventy-two accelerators, weighs two tons, costs around four million dollars, and contains roughly one and a half million parts. One gigawatt of factory capacity costs around fifty billion dollars to build and emits three hundred to four hundred billion dollars of token output per year — a revenue-to-capex multiple of six to eight times at the asset level. The total capital flowing into the stack in 2026 is on the order of one trillion dollars, against an implied steady-state ecosystem of roughly twenty trillion dollars per year. This is not a software business — it is a fab. This is the unit economic that breaks every capex-normalization forecast in the market. Forecasters are pricing buildings; operators are pricing production lines.

The second-order consequence is retrieval decay. Every business priced on retrieval economics — search advertising, content aggregation, social feeds, recommendation networks — is in slow runoff. Retrieval businesses paid pennies per query because they re-served stored content with marginal cost approaching zero. Generation businesses meter compute per query because each output is originally produced. The cost curve is different. The pricing model is different. The defensibility is different.

The third-order consequence is the agentic demand shock. Today, intelligence is consumed by roughly one billion humans through chat interfaces. In the agentic phase — already underway — intelligence will be consumed by roughly 100 billion agents running continuously, talking to each other, executing tasks, calling tools, and coordinating workflows. That is a hundredfold demand step change layered on top of the existing consumer demand. The factories under construction are not overbuilt. They are underbuilt relative to a demand curve that has not yet materialized.

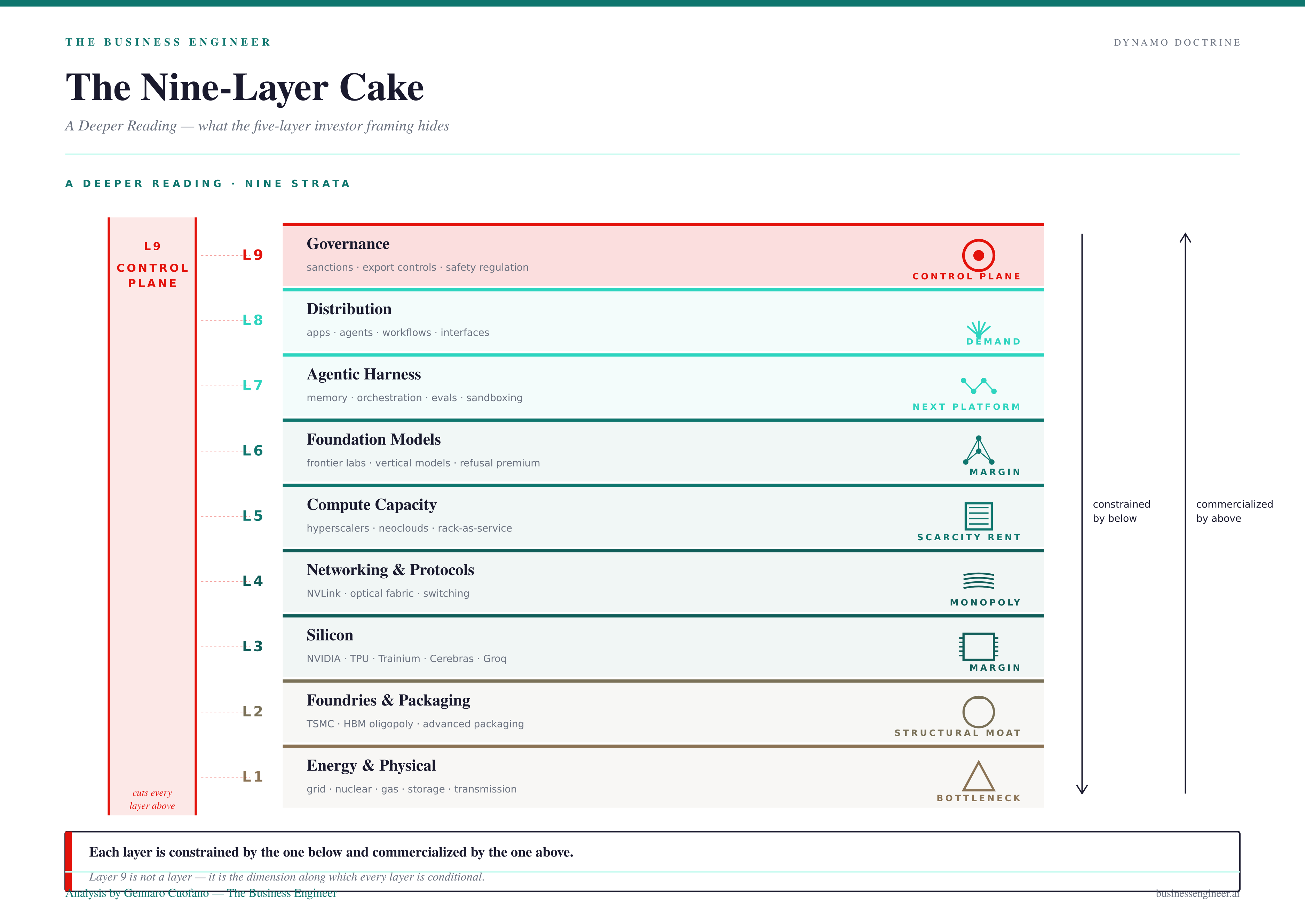

The Nine-Layer Cake — A Deeper Reading

The standard investor framing of the AI stack has five layers — energy, compute, infrastructure, models, applications. It is a useful public-facing compression, but it hides at least four separations that have become structurally consequential. A more accurate reading of the stack has nine layers.

The five-layer framing collapses what are now separate profit pools. Networking has separated from compute — rack-scale interconnects consume more than twenty percent of system cost and are growing roughly two hundred percent year-on-year, with one company holding monopoly economics on the interconnect.

Foundries have separated from silicon — allocation power at the leading-edge fab and the high-bandwidth memory oligopoly is now more consequential than chip design itself.

Governance has separated from generic policy and trust — it is now a priced variable in enterprise procurement and a binding constraint on cross-border deployment. Silicon itself has bifurcated into a generalist substrate, hyperscaler custom silicon, and merchant custom challengers. Each of these separations is its own market with its own incumbents, moat, and bottleneck.

Bottom-to-top, the nine layers are:

1 · Energy & Physical. Generation, transmission, water, cooling, land, permits. The first serious grid investment cycle in roughly a century. Power is the binding constraint for everything above it. Rare-earth supply, transformer steel, and grid-scale storage chemistry are the physical chokepoints that govern the pace of the entire stack. Capital intensity is extreme; margin is regulated; the moat is physical and political.

2 · Foundries & Packaging. The fab and the package — the physical conversion of designs into silicon. Allocation power at the leading-edge foundry and the HBM oligopoly is now a more consequential bottleneck than chip design. Advanced packaging (CoWoS and equivalents) is the binding constraint on supply for the next two generations of accelerators. Capital intensity is the highest in the entire economy. Margin is high at the frontier and structurally protected by twenty-plus-year capability gaps to the next-best competitor.

3 · Silicon. Chip design itself — generalist accelerators, hyperscaler custom silicon (custom TPUs, training accelerators, inference accelerators), and merchant custom challengers. The layer has bifurcated into three structurally different positions: the dominant generalist who sets the software stack, the captive customs who optimize for one workload, and the merchant customs who specialize on inference or specific architectures. Margin concentrates at the generalist; volume disperses to the customs.

4 · Networking & Protocols. Rack-scale interconnect, optical fabric, switching silicon, and the protocols stitching factories together. This layer carries monopoly economics on the leading edge — the interconnect is the most under-priced asset in the public market. Networking is now growing faster than compute itself because every additional accelerator demands a non-linear increase in interconnect bandwidth.

5 · Compute Capacity. The actual deployable rack-and-power-contract bundle — what hyperscalers and neoclouds sell. The difference between owning silicon and being able to deploy it at scale is now its own market. Capital intensity is extreme. Margin is high while scarcity holds and will normalize toward utility-like over a decade as the physical layer catches up.

6 · Foundation Models. The visible language models cover one slice. The industrial layer is everything else — protein, cell, genome, materials, physics, climate, robotics control, autonomous driving, code, design, audio. Anything with structure is learnable; anything learnable becomes a model; every model is a vertical market. The layer is shaped by three structural philosophies: maximalist capability frontiers (capability is the moat), trust and safety frontiers (refusal and reliability are the moat), and integrated platform frontiers (distribution into existing ecosystems is the moat). These are not interchangeable strategies — they produce structurally different products and command different multiples. The safety-positioned frontier in particular commands a refusal premium — enterprise buyers pay materially more for a model whose refusal behavior they can underwrite.

7 · Agentic Harness. The orchestration substrate that turns model output into operational output — tool calling, memory, planning, retries, evaluation, guardrails, sandboxing, multi-agent coordination. This is the layer that most application-layer companies confuse with their product. It is in fact a horizontal infrastructure layer in its own right, comparable to the cloud-native infrastructure layer of the prior decade. The companies that own the harness — and the persistent state that agents accumulate inside it — will become the next generation of infrastructure incumbents.

8 · Distribution. Applications, surfaces, and channels — the layer that touches the user. $100B of venture capital deployed in 2025 alone, the largest year in the history of the asset class. It is also the most fragmented layer and the one with the highest failure rate. Most application-layer companies built on a single model capability are absorbed by the next model release. The breakouts here own a workflow, not a feature, and reprice from per-seat to per-token or per-outcome.

9 · Governance. Policy, sanctions, export controls, deemed-export rules, AI safety regulation, model accountability, antitrust. This was treated for years as a soft layer — a horizontal constraint, not a market. It has now become a control plane perpendicular to the entire stack. A single jurisdictional directive can switch off a frontier model across every customer on the planet in seventy-two hours. Governance does not sit on top of the stack — it cuts through it. This is the most consequential reframe in the deeper reading: Layer 9 was never a layer. It is the dimension along which every other layer is conditional.

Two reading rules govern the stack. Each layer is constrained by the one below it — you cannot ship a model without compute, you cannot ship compute without silicon, you cannot ship silicon without foundries, you cannot ship foundries without energy. Each layer is commercialized by the one above it — silicon needs models to monetize, models need a harness, the harness needs distribution. Read top-down to see what gets priced. Read bottom-up to see what gets bottlenecked.

Where profit pools concentrate. Read the stack as a column to see one company’s full vertical posture — only a handful of operators in the world are deeply present across more than three layers, and those that are command the largest market capitalizations on Earth. Read the stack as a row to see who owns one layer in isolation. The diagonal between vertical integration and horizontal monopoly is where the supercycle’s profit pools live. Capex concentrates at L1–L5. Margin concentrates at L3 (silicon), L4 (networking), L6 (models), L7 (harness), and L8 (distribution). Demand concentrates at L8. Bottleneck concentrates at L1. Control concentrates at L9.

Any portfolio that touches only one layer carries dependency risk on all the others. The complete investment thesis specifies which layer is being financed, which adjacent layer the position depends on, and which jurisdictional governance regime the position assumes.

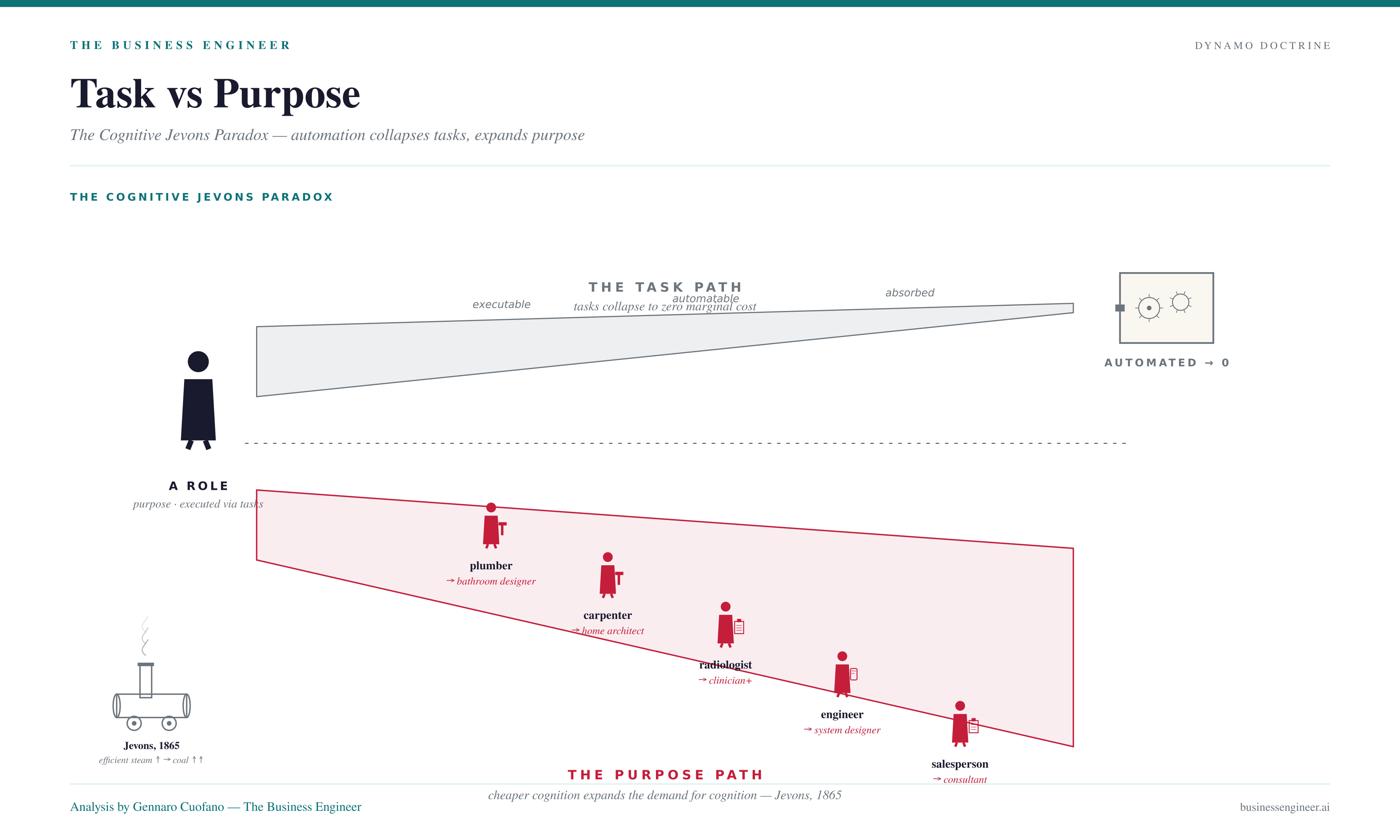

Task vs Purpose — The Cognitive Jevons Paradox

There is a single mechanism that controls how the labor market reorganizes in the intelligence age. It is the same mechanism that controlled the steam age, the electrification age, and the computerization age, and it has been misread every time. The mechanism is the distinction between task and purpose.

A task is the thing a person does in a given hour. A purpose is the reason the task exists. Automation collapses tasks. It does not collapse purposes. And when the underlying purpose is demand-unconstrained — when there is more of it wanted than is currently supplied — automating the task expands employment in the role, not contracts it.

Twelve years ago, a leading voice forecast the extinction of the radiology profession on the strength of superhuman computer vision. Computer vision did saturate radiology. Every reading is now augmented by it. And the number of radiologists is up, scan volume is up, departmental profitability is up. The mechanism: AI made each radiologist more productive, which lowered the cost per scan, which expanded the volume of patients who could be admitted, which increased departmental revenue, which justified hiring more radiologists. The same forecast made about software engineers in 2024 — “ninety percent of coding will be automated” — is being falsified in real time by record hiring at the foundation model labs.

This is a cognitive version of Jevons’ paradox: in 1865, William Stanley Jevons observed that more efficient steam engines did not reduce British coal consumption — they expanded it, because lower cost per unit of work expanded the universe of work being done. Cognitive labor sits in the same regime. Cheaper cognition expands the demand for cognition. The plumber becomes a bathroom designer. The carpenter becomes a home architect. The salesperson becomes an interior consultant. The accountant becomes a strategic advisor. The radiologist becomes a clinician with infinite scan capacity.

Three predictions follow directly. First, aggregate cognitive employment grows, not shrinks — the roles change shape, the headcount expands. Second, roles defined by task automate while roles defined by purpose elevate — a clear definition of purpose is now a labor market moat. Third, the geographic and educational concentration of cognitive work flattens — the prior dominant programming language was known by roughly two percent of humanity, the new programming language is human language known by roughly one hundred percent, and the population of programmers therefore becomes the population of humans. Returns to scale move from technical populations to user populations.

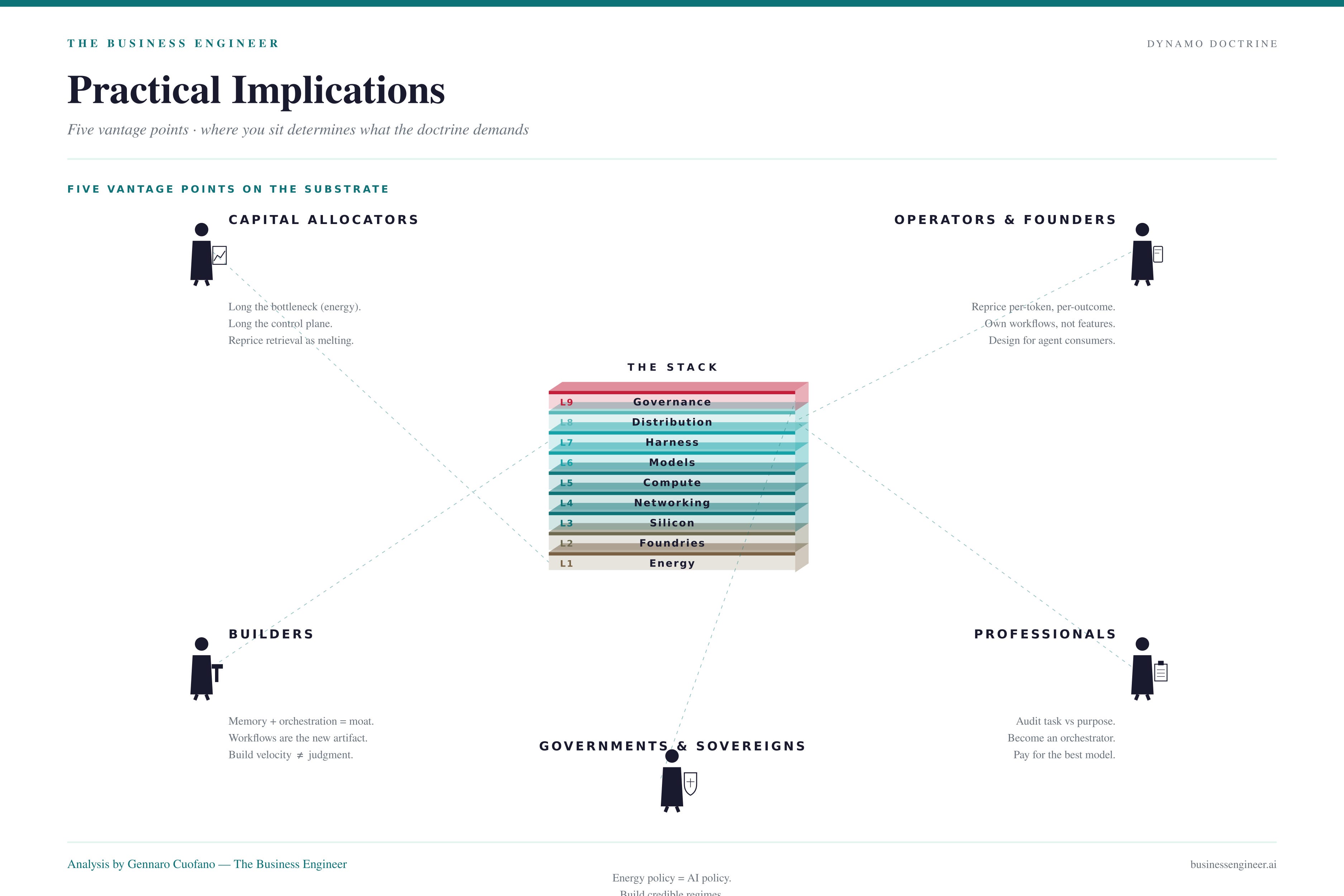

Practical Implications