AI & The Search Paradigm Shift

The current narrative around Google Search’s resilience in the AI era fundamentally misunderstands the transformation underway.

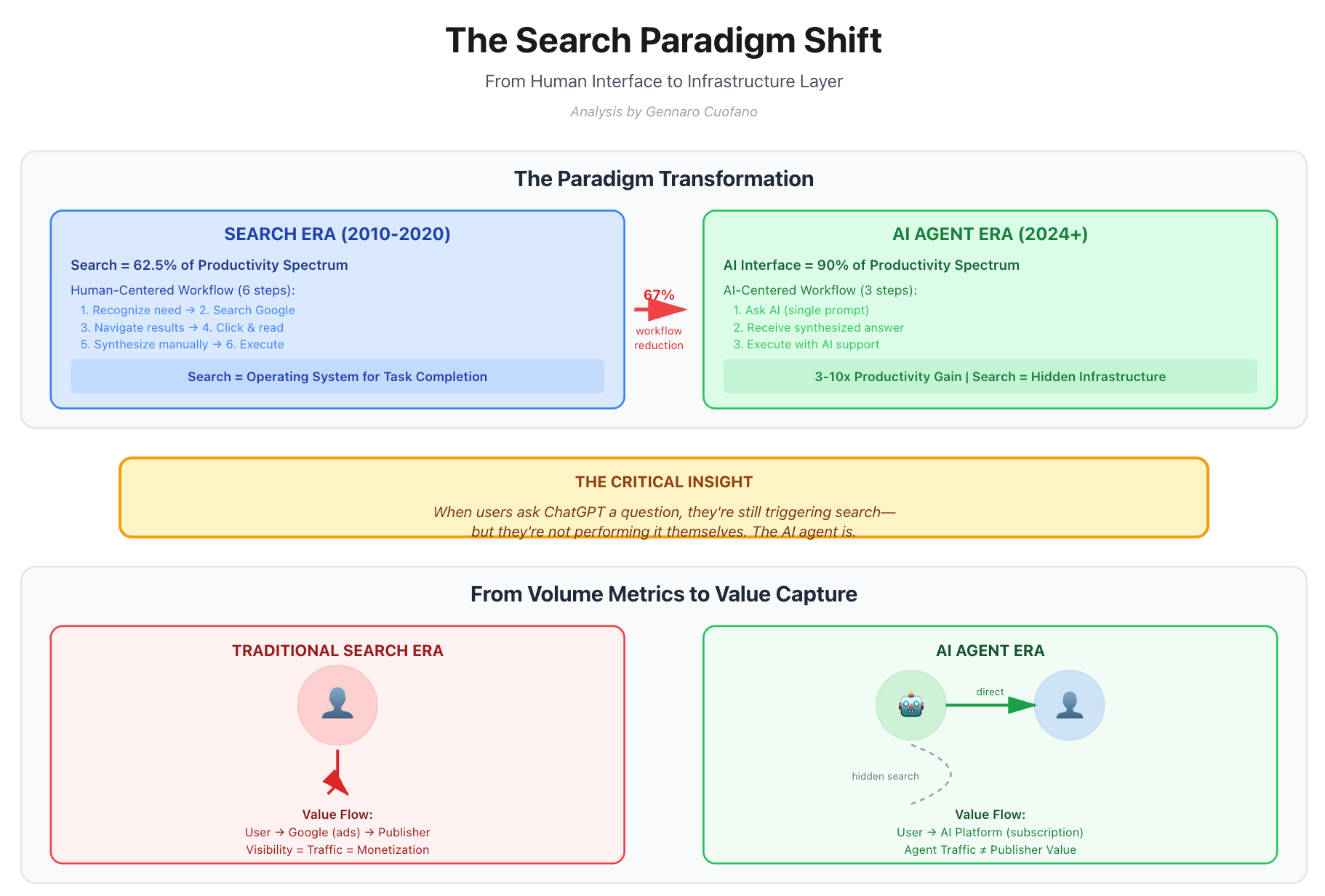

In fact, the graphic argues that since Google Search is seeing an increased usage, then nothing is changing, actually, traditional search might be having a sort of resurrection!

Yes, search volume is growing. Yes, AI tools are driving more queries to Google. But this growth obscures a profound architectural shift: search is transitioning from a human-facing productivity tool to an invisible retrieval layer for AI agents.

This isn’t about whether search survives, it will. This is about understanding where the search business survives and what that means for its economics.