Snowflake's AI Bet & The Future of SaaS

Premium Analysis

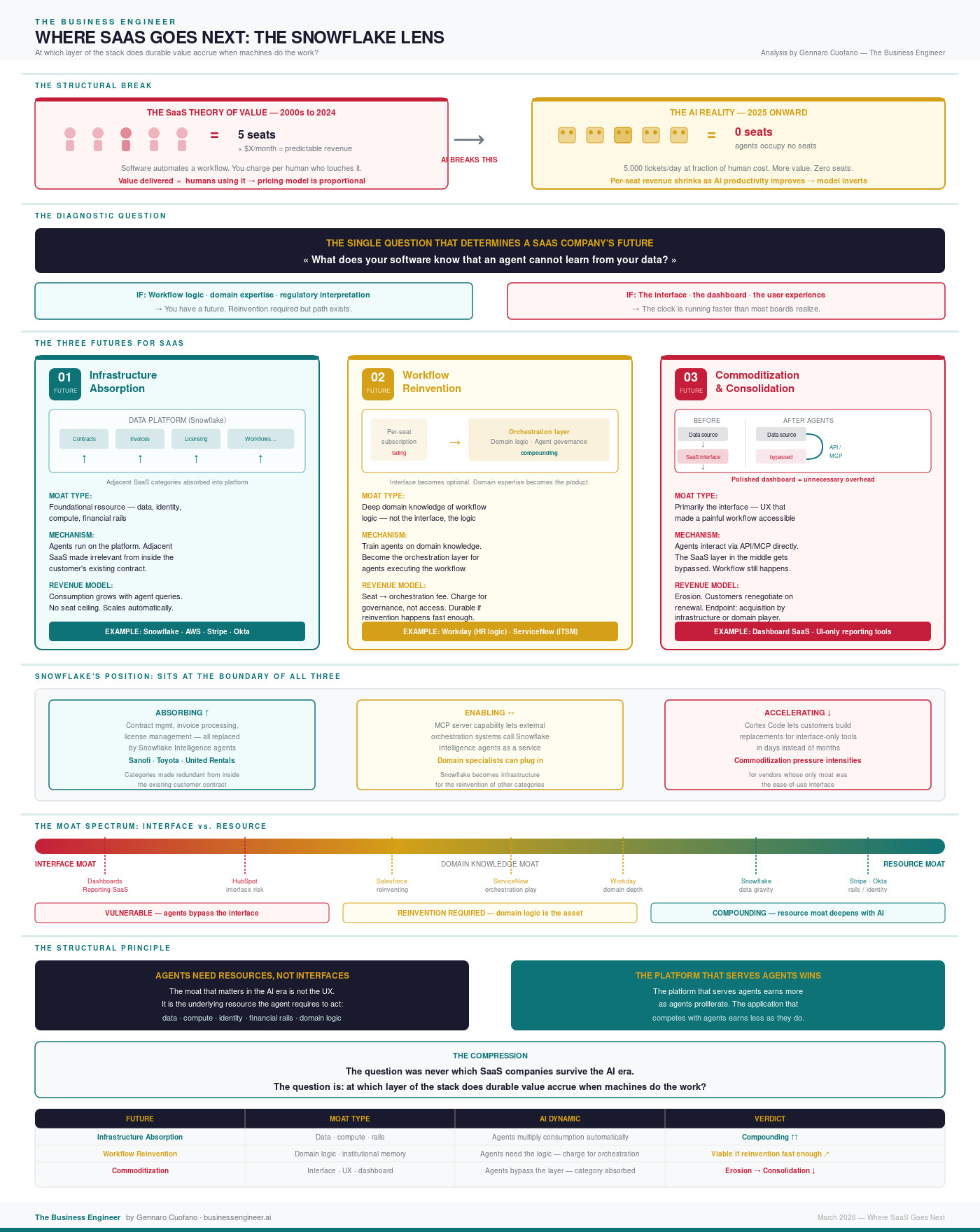

For the past two years, the enterprise software world has been asking: which AI company will win? The better question — the more structurally interesting one — is: which companies were accidentally built for the AI era before they knew it was coming?

In the last few days, I’ve given you a view of where this is going next, and it’s not just a passing change; it’s structural.

Snowflake is the clearest answer in enterprise infrastructure. Not because it out-competed anyone on AI. Not because it saw the agentic wave coming.

But because the mechanics of its business model — consumption pricing, data gravity, cross-cloud neutrality, governance-first architecture — happen to be exactly what the AI era requires.

The company built a platform that lets humans query data. It turns out the same platform scales to machines querying data at a thousand times the rate. That is not a strategy. That is structural luck meeting structural preparation. And in business, that combination is the rarest kind of moat.

The Q4 FY2026 earnings report — $1.23 billion in product revenue, 30% year-over-year growth, RPO accelerating to $9.77 billion at 42% growth — is not just a strong quarter. It is the first measurable signal that the transformation is real, not rhetorical.