The New Geopolitical Architecture

This Week In Business AI [Week #10-2026]

To be clear from the outset, this is a geopolitical analysis. As such, it operates beyond personal sympathies or political preferences. The goal is to examine the structural dynamics beneath events. That is what analysis requires: stepping back from individual views to build a framework capable of interpreting what comes next.

Having described myself as an analyst for more than twenty years, I owe my audience a structural reading of what is unfolding. The objective is not commentary but to identify the forces and frameworks likely to shape the next decade.

Other geopolitical frameworks we shared in the past:

Most commentary frames what’s happening between Washington and Beijing as a trade negotiation, tariffs in, tariffs out, Boeing planes, soybeans, fentanyl. This is the wrong level of analysis.

What’s being negotiated is the operating system of the global economy for the next decade. Both sides know this. The Paris meeting (mid-March, Bessent + Greer + He Lifeng) and the planned April summit are the sixth round in a process that began in Geneva (May 2025) and continued through London, Stockholm, Madrid, and Kuala Lumpur.

Each meeting has functioned as a deliverable-setting session ahead of a higher-level event. Paris is pre-summit staging for the most consequential phase yet — with a freshly restructured legal baseline underneath it.

Surface narrative: Trade negotiation over tariffs and purchases.

Hidden driver: Both sides are managing their domestic vulnerabilities through the appearance of leverage over the other — and codifying the rules of a world that neither can dominate unilaterally.

The structural frame that emerges from prior rounds is a Three-Tier Architecture of global commerce:

Tier 1 — Strategic Denial: Hard wall, no negotiation. Blackwell/Rubin GPUs, quantum computing, EUV lithography, sub-3nm fabrication, frontier AI model weights. These remain within the allied perimeter regardless of what is agreed in Paris or April. China probes this tier in every negotiation; the answer is always no.

Tier 2 — Managed Commerce: Permissioned flows with leverage embedded. Previous-gen semiconductors, agricultural commodities, aircraft, energy, and green technology. This is the Paris agenda. The H200 deal is the prototype: US controls the tap, monetizes the flow, China gets the capability its domestic industry can’t yet match. The 25% government surcharge on Nvidia H200 sales to China is not a concession — it’s a revenue-sharing mechanism that makes the arrangement politically sustainable in Washington.

Tier 3 — Open Competition: Non-strategic goods at permanently elevated but negotiated rates. Consumer goods, industrial inputs, and general manufacturing. These flow at Section 122 (15%) + Section 301 (7.5–100%) + Section 232 (sector-specific) — the new structural cost of doing business, not a temporary disruption.

The Paris meeting operates almost entirely in Tiers 2 and 3 — the contested middle ground where both sides have genuine leverage and genuine commercial need.

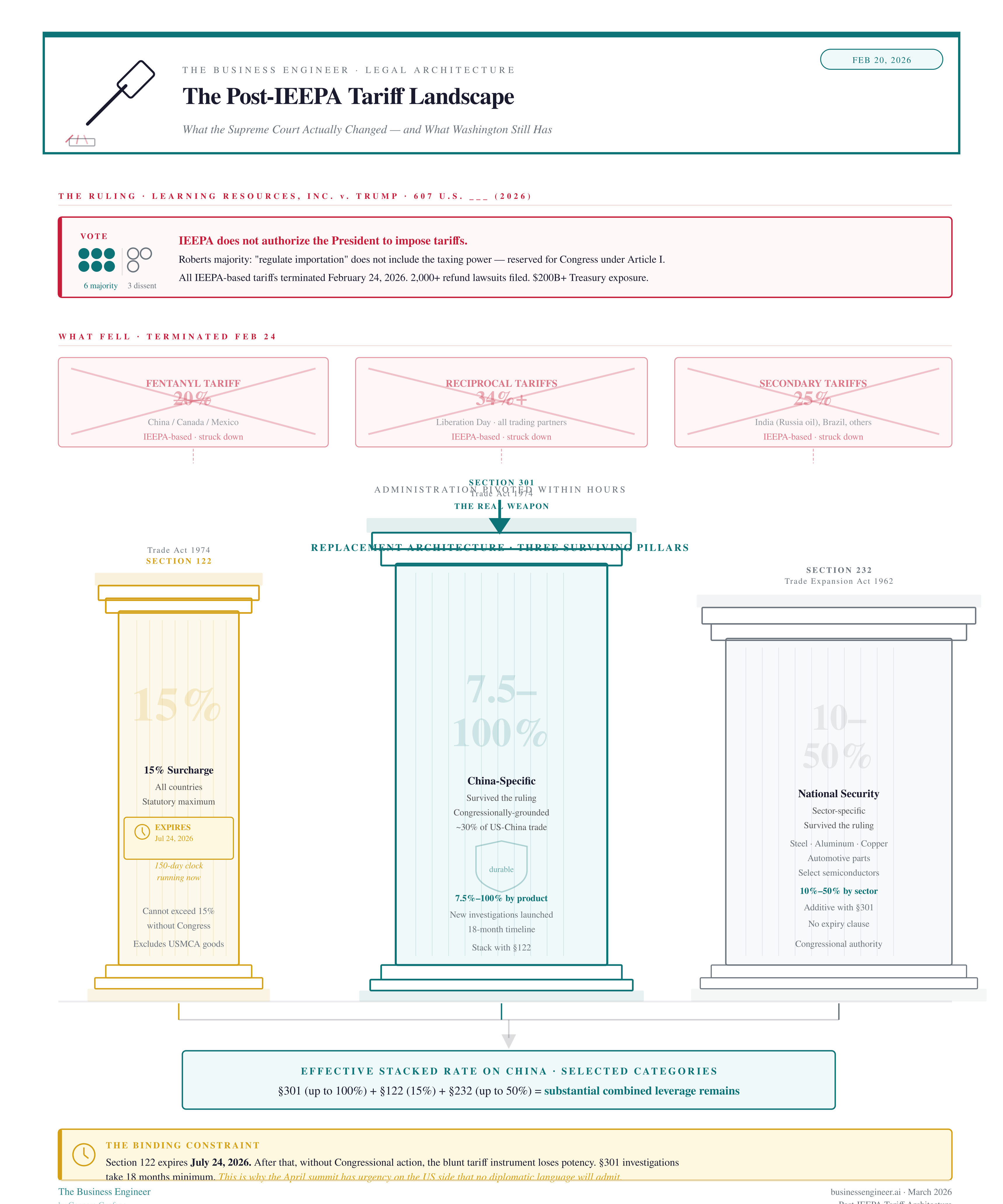

The Post-IEEPA Tariff Landscape: What the Supreme Court Actually Changed

On February 20, 2026, the Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that IEEPA does not authorize the president to impose tariffs. Chief Justice Roberts held that “regulate importation” in the 1977 statute does not include the taxing power, which belongs to Congress under Article I. The ruling invalidated the fentanyl tariffs, the reciprocal Liberation Day tariffs, and the broader IEEPA-based trade architecture — effective February 24.

The immediate effect on China: The 20% fentanyl tariff — gone. The 34%+ reciprocal tariff — gone. Over $200 billion in IEEPA tariffs paid by importers are now in legal jeopardy, with 2,000+ refund lawsuits filed. The effective tariff rate on Chinese goods collapsed significantly, giving Beijing a genuine opening ahead of the summit.

The Trump administration pivoted within hours. The replacement architecture rests on three surviving statutory pillars:

IEEPA Tariffs

34%+— struck down. Refund litigation ongoing. $200B+ Treasury exposure.Section 122 (Trade Act 1974): 15% temporary import surcharge on virtually all countries. Statutory maximum. Valid 150 days, expires July 24, 2026. Cannot be exceeded without Congressional action.

Section 301 (Trade Act 1974): China-specific. Survived ruling. Product-specific rates of 7.5–100% covering ~30% of US-China trade. New Section 301 investigations announced — 12–18 month timeline to new tariffs.

Section 232 (Trade Expansion Act 1962): National security basis. Sector-specific: steel, aluminum, copper, automotive parts, certain semiconductors. 10–50%. Survived ruling. Adds to 301 rates in covered categories.

The structural weakness this creates for Washington is precise: the Section 122 clock expires July 24, 2026. After that date, without new Congressional action or completed Section 301 investigations (an 18-month minimum), the blunt tariff instrument loses its potency. This is why the April summit has urgency on the US side that no diplomatic language will admit.

What’s happening next?

In the last few weeks, I’ve given you a view of where software is going next:

Read Also:

The weekly newsletter is in the spirit of what it means to be a Business Engineer:

We always want to ask three core questions:

What’s the shape of the underlying technology that connects the value prop to its product?

What’s the shape of the underlying business that connects the value prop to its distribution?

How does the business survive in the short term while adhering to its long-term vision through transitional business modeling and market dynamics?

These non-linear analyses aim to isolate the short-term buzz and noise, identify the signal, and ensure that the short-term and the long-term can be reconciled.